diff --git a/src/posts/articles/Benefit-uprating-25.md b/src/posts/articles/Benefit-uprating-25.md

index 8afb9027f..d806b32bc 100644

--- a/src/posts/articles/Benefit-uprating-25.md

+++ b/src/posts/articles/Benefit-uprating-25.md

@@ -4,7 +4,7 @@

PolicyEngine estimates that the 1.7% benefits uprating for 2025/26:

-- increases government costs by [£2.5 billion](https://policyengine.org/uk/policy?focus=policyOutput.policyBreakdown&reform=1®ion=uk&timePeriod=2025&baseline=69807&mode=lite)

+- increases government costs by [£2.5 billion](https://legacy.policyengine.org/uk/policy?focus=policyOutput.policyBreakdown&reform=1®ion=uk&timePeriod=2025&baseline=69807&mode=lite)

- lowers poverty by 1.8%

- raises net income for 45.9% of people

diff --git a/src/posts/articles/american-family-act-2025.md b/src/posts/articles/american-family-act-2025.md

index b9a080364..85c82207b 100644

--- a/src/posts/articles/american-family-act-2025.md

+++ b/src/posts/articles/american-family-act-2025.md

@@ -12,7 +12,7 @@ Key results (static):

- Reduces the Gini index of income inequality by 2.4%

-_Use PolicyEngine to [view the full results](https://policyengine.org/us/policy?focus=policyOutput.policyBreakdown&reform=82820®ion=us&timePeriod=2025&baseline=2&dataset=enhanced_cps) or calculate the [effect on your household](https://policyengine.org/us/household?focus=intro&reform=82820®ion=us&timePeriod=2025&baseline=2&dataset=enhanced_cps)._

+_Use PolicyEngine to [view the full results](https://legacy.policyengine.org/us/policy?focus=policyOutput.policyBreakdown&reform=82820®ion=us&timePeriod=2025&baseline=2&dataset=enhanced_cps) or calculate the [effect on your household](https://legacy.policyengine.org/us/household?focus=intro&reform=82820®ion=us&timePeriod=2025&baseline=2&dataset=enhanced_cps)._

## History of Democrats’ Push to Expand the CTC

@@ -20,7 +20,7 @@ In the past decade, Democratic lawmakers have supported several proposals to exp

## The American Family Act’s Provisions

-The 2025 American Family Act makes several changes to the Child Tax Credit (CTC). While the 2025 AFA shares a structure with previous versions and [Harris’s CTC plan](https://policyengine.org/us/research/harris-ctc) and the [American Rescue Plan Act CTC](https://policyengine.org/us/research/restoration-of-the-american-rescue-plan-acts-expanded-child-tax-credit), it offers larger benefits than these other CTC proposals.

+The 2025 American Family Act makes several changes to the Child Tax Credit (CTC). While the 2025 AFA shares a structure with previous versions and [Harris’s CTC plan](https://legacy.policyengine.org/us/research/harris-ctc) and the [American Rescue Plan Act CTC](https://legacy.policyengine.org/us/research/restoration-of-the-american-rescue-plan-acts-expanded-child-tax-credit), it offers larger benefits than these other CTC proposals.

Under the 2025 AFA, children under the age of six are eligible for a maximum credit of $4,320 ($360 per month), while children aged 6 to 17 would receive $3,600 ($300 per month). The 2025 AFA also contains a baby bonus where parents of newborns can claim $2,400 for the first month instead of the standard $360 monthly credit for young children. This means families with newborn children would receive a total of $6,360 during the baby’s first year. Additionally, the 2025 AFA extends the $500 nonrefundable adult dependent credit beyond its scheduled 2026 expiration date, preserving a benefit that was originally enacted in the Tax Cuts and Jobs Act of 2017.

@@ -42,15 +42,15 @@ Table 1 summarizes the key parameters of the 2025 AFA compared against the previ

## Household Impacts

-Since the 2025 AFA makes the CTC fully refundable, households with no household earnings would now be eligible for the entire credit, raising their net income. For example, a single parent with a newborn and no income currently receives no CTC. However, with the fully refundable CTC and baby bonus component, their [net income would increase by $6,360](https://policyengine.org/us/household?focus=householdOutput.netIncome&reform=82820®ion=us&timePeriod=2028&baseline=2&dataset=enhanced_cps&household=53124), the highest gain of any household with one child.

+Since the 2025 AFA makes the CTC fully refundable, households with no household earnings would now be eligible for the entire credit, raising their net income. For example, a single parent with a newborn and no income currently receives no CTC. However, with the fully refundable CTC and baby bonus component, their [net income would increase by $6,360](https://legacy.policyengine.org/us/household?focus=householdOutput.netIncome&reform=82820®ion=us&timePeriod=2028&baseline=2&dataset=enhanced_cps&household=53124), the highest gain of any household with one child.

-Middle-income families with qualifying children will also see a boost to their net income. For example, a married couple with two children (ages 4 and 8) with $80,000 of annual earnings [would gain $3,920](https://policyengine.org/us/household?focus=householdOutput.netIncome&reform=82820®ion=us&timePeriod=2028&baseline=2&dataset=enhanced_cps&household=53129). Their new CTC allotment would reach $7,920, increasing from $4,000 today.

+Middle-income families with qualifying children will also see a boost to their net income. For example, a married couple with two children (ages 4 and 8) with $80,000 of annual earnings [would gain $3,920](https://legacy.policyengine.org/us/household?focus=householdOutput.netIncome&reform=82820®ion=us&timePeriod=2028&baseline=2&dataset=enhanced_cps&household=53129). Their new CTC allotment would reach $7,920, increasing from $4,000 today.

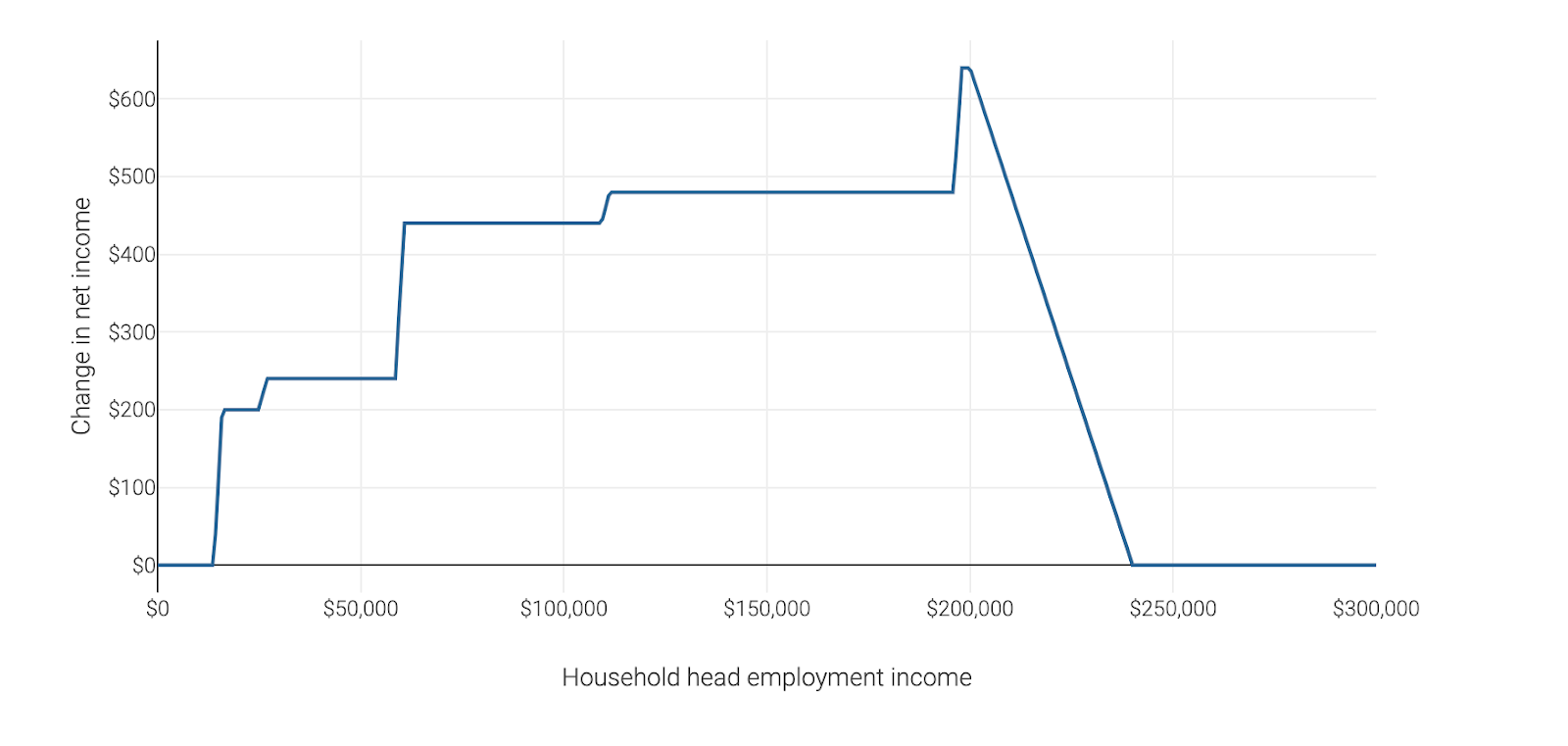

-As income rises, households will be subject to the initial phase-out. A single parent with one older child and $135,000 of earnings will receive $2,450 from the CTC, [resulting in a gain of $450 to their net income](https://policyengine.org/us/household?focus=householdOutput.netIncome&reform=82820®ion=us&timePeriod=2028&baseline=2&dataset=enhanced_cps&household=53141). As this household’s income exceeds the lower threshold of $112,500 for head of household filers, the CTC value is reduced, falling by $1,150 from its $3,600 maximum. If this family’s income fell between $150,000 and $300,000, they would receive $2,000 as the initial threshold cannot reduce the benefit lower than $2,000 per child.

+As income rises, households will be subject to the initial phase-out. A single parent with one older child and $135,000 of earnings will receive $2,450 from the CTC, [resulting in a gain of $450 to their net income](https://legacy.policyengine.org/us/household?focus=householdOutput.netIncome&reform=82820®ion=us&timePeriod=2028&baseline=2&dataset=enhanced_cps&household=53141). As this household’s income exceeds the lower threshold of $112,500 for head of household filers, the CTC value is reduced, falling by $1,150 from its $3,600 maximum. If this family’s income fell between $150,000 and $300,000, they would receive $2,000 as the initial threshold cannot reduce the benefit lower than $2,000 per child.

-However, because the current CTC begins to fully phase out at $200,000 for head of household filers, this household with $250,000 of annual earnings would see a [$2,000 increase to their net income](https://policyengine.org/us/household?focus=householdOutput.netIncome&reform=82820®ion=us&timePeriod=2028&baseline=2&dataset=enhanced_cps&household=53143) as the AFA raises the higher phaseout threshold to $300,000. Once household income reaches $340,000, the CTC fully phases out, and their change in net income falls back to $0.

+However, because the current CTC begins to fully phase out at $200,000 for head of household filers, this household with $250,000 of annual earnings would see a [$2,000 increase to their net income](https://legacy.policyengine.org/us/household?focus=householdOutput.netIncome&reform=82820®ion=us&timePeriod=2028&baseline=2&dataset=enhanced_cps&household=53143) as the AFA raises the higher phaseout threshold to $300,000. Once household income reaches $340,000, the CTC fully phases out, and their change in net income falls back to $0.

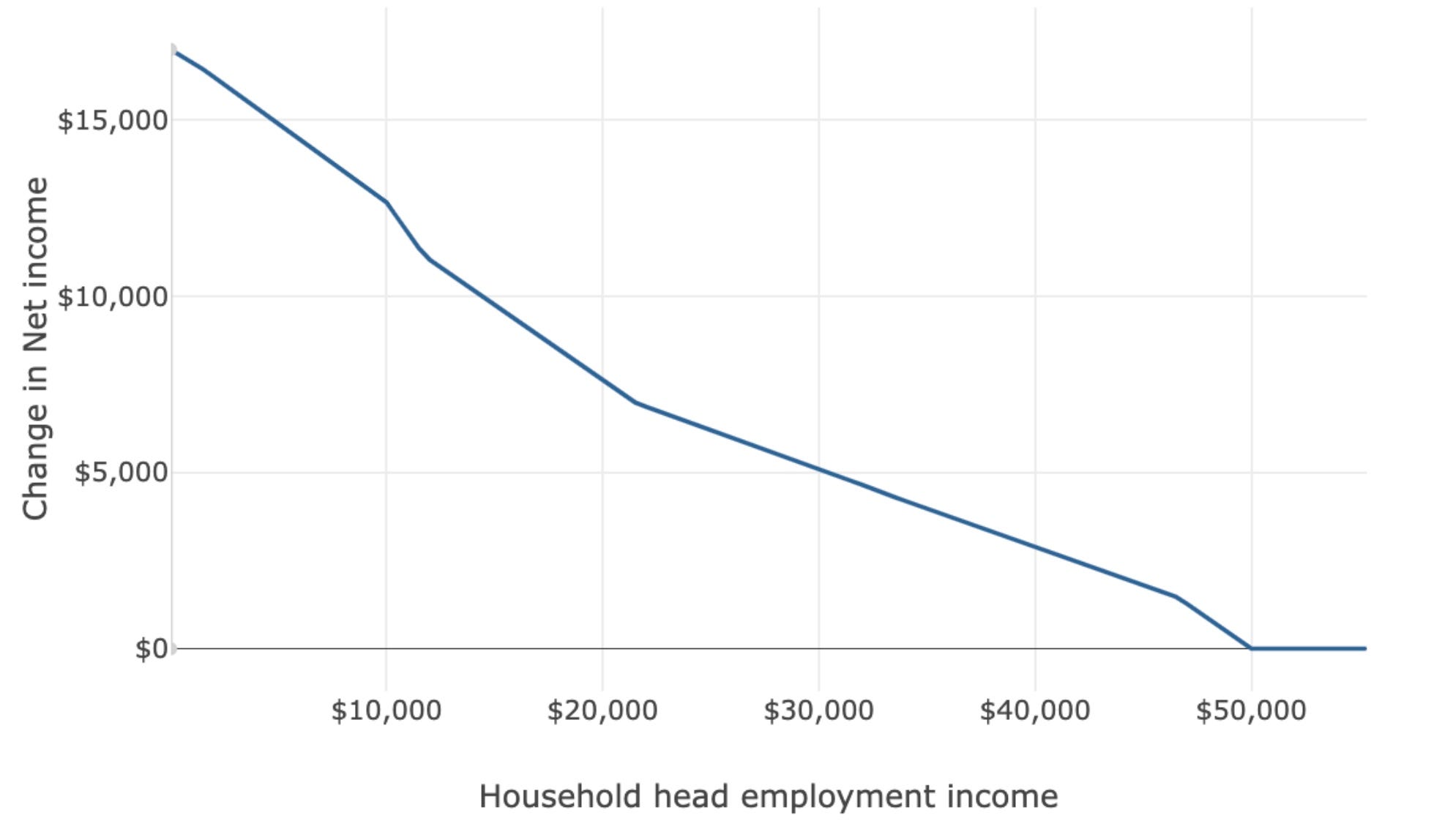

-The AFA leaves some married filers with both adult and child dependents worse off: consider a couple with earnings of $425,000, an adult dependent, and an 8-year-old child. As the AFA phases out — the adult dependent credit and CTC simultaneously — joint filers see a decrease in net income until the entirety of the CTC and adult dependent credit value phases out, as under current law. For this household, net income begins to fall at $400,000 before plateauing at [a $500 decrease](https://policyengine.org/us/household?focus=householdOutput.netIncome&reform=82820®ion=us&timePeriod=2028&baseline=2&dataset=enhanced_cps&household=54174). Once the current CTC is phased out at $440,000, net income begins to rise as the remaining $500 adult dependent credit begins to phase out. At $450,000, net income stabilizes at $0. The AFA’s increased head of household phase-out threshold prevents unmarried filers from paying higher tax.

+The AFA leaves some married filers with both adult and child dependents worse off: consider a couple with earnings of $425,000, an adult dependent, and an 8-year-old child. As the AFA phases out — the adult dependent credit and CTC simultaneously — joint filers see a decrease in net income until the entirety of the CTC and adult dependent credit value phases out, as under current law. For this household, net income begins to fall at $400,000 before plateauing at [a $500 decrease](https://legacy.policyengine.org/us/household?focus=householdOutput.netIncome&reform=82820®ion=us&timePeriod=2028&baseline=2&dataset=enhanced_cps&household=54174). Once the current CTC is phased out at $440,000, net income begins to rise as the remaining $500 adult dependent credit begins to phase out. At $450,000, net income stabilizes at $0. The AFA’s increased head of household phase-out threshold prevents unmarried filers from paying higher tax.

Figure 1 displays the value of the CTC under the AFA compared to current law, while Figure 2 shows the change in net income for a single parent with one older child as annual earnings vary.

@@ -78,7 +78,7 @@ Table 2 summarizes the change in net income for each household discussed above.

## Microsimulation Results

-Using PolicyEngine’s static microsimulation model, we project that the American Family Act will cost the federal government [$167.2 billion in 2025](https://policyengine.org/us/policy?focus=policyOutput.budgetaryImpact.overall&reform=82820®ion=us&timePeriod=2025&baseline=2&dataset=enhanced_cps). Over a ten-year period (2025–2034), the legislation will reduce federal tax revenues by $2.5 trillion.

+Using PolicyEngine’s static microsimulation model, we project that the American Family Act will cost the federal government [$167.2 billion in 2025](https://legacy.policyengine.org/us/policy?focus=policyOutput.budgetaryImpact.overall&reform=82820®ion=us&timePeriod=2025&baseline=2&dataset=enhanced_cps). Over a ten-year period (2025–2034), the legislation will reduce federal tax revenues by $2.5 trillion.

**Table 3: Annual Federal Budgetary Impact of the AFA**

@@ -98,25 +98,25 @@ Using PolicyEngine’s static microsimulation model, we project that the America

Because the TCJA’s CTC provisions expire for tax year 2026, the cost of the AFA increases as the CTC’s value is projected to fall to $1,000 compared to its current maximum of $2,000. In addition to the federal budgetary impact, the AFA will reduce state revenues by $35 billion over ten years due to interactions with the CTC provisions.

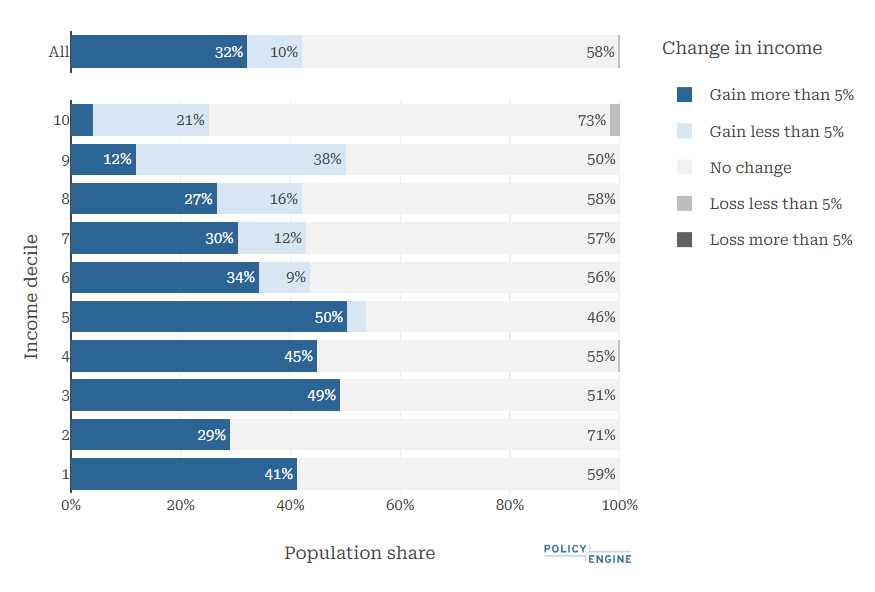

-The AFA will [raise the net income of 42.1% of American residents](https://policyengine.org/us/policy?focus=policyOutput.winnersAndLosers.incomeDecile&reform=82820®ion=us&timePeriod=2025&baseline=2&dataset=enhanced_cps) in 2025, including 25% of those in the top income decile and 54% of those in the fifth decile. Additionally, 1.7% of people in the top income decile would see their net incomes decline due to the adult dependent phasing out independently of the CTC rather than as one combined value. In 2026, when the TCJA expires, the AFA will increase the net income of [46.7%](https://policyengine.org/us/policy?focus=policyOutput.winnersAndLosers.incomeDecile&reform=82820®ion=us&timePeriod=2026&baseline=2&dataset=enhanced_cps) of people, while leaving no households worse off, since the adult dependent credit expires with the TCJA.

+The AFA will [raise the net income of 42.1% of American residents](https://legacy.policyengine.org/us/policy?focus=policyOutput.winnersAndLosers.incomeDecile&reform=82820®ion=us&timePeriod=2025&baseline=2&dataset=enhanced_cps) in 2025, including 25% of those in the top income decile and 54% of those in the fifth decile. Additionally, 1.7% of people in the top income decile would see their net incomes decline due to the adult dependent phasing out independently of the CTC rather than as one combined value. In 2026, when the TCJA expires, the AFA will increase the net income of [46.7%](https://legacy.policyengine.org/us/policy?focus=policyOutput.winnersAndLosers.incomeDecile&reform=82820®ion=us&timePeriod=2026&baseline=2&dataset=enhanced_cps) of people, while leaving no households worse off, since the adult dependent credit expires with the TCJA.

**Figure 2: Winners of the AFA (2025)**

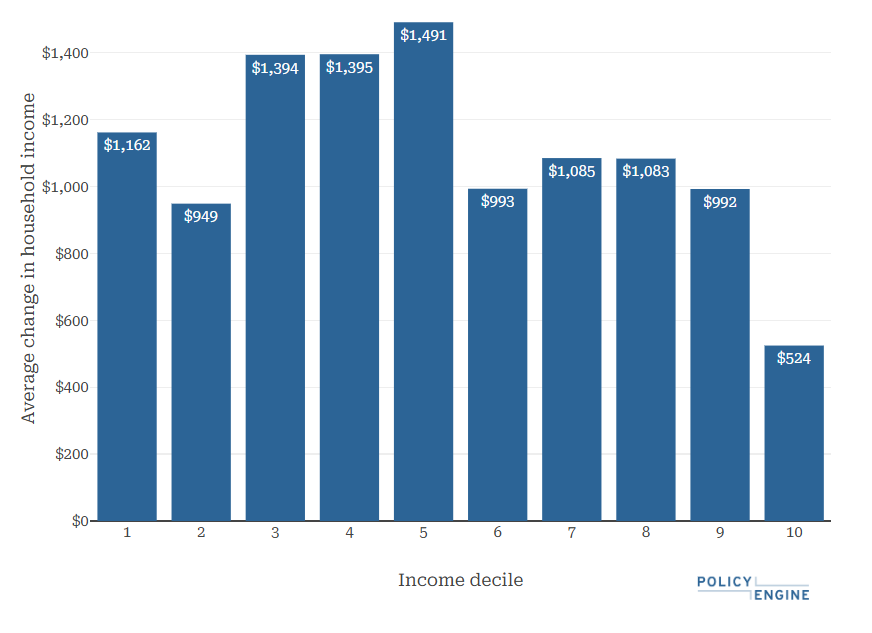

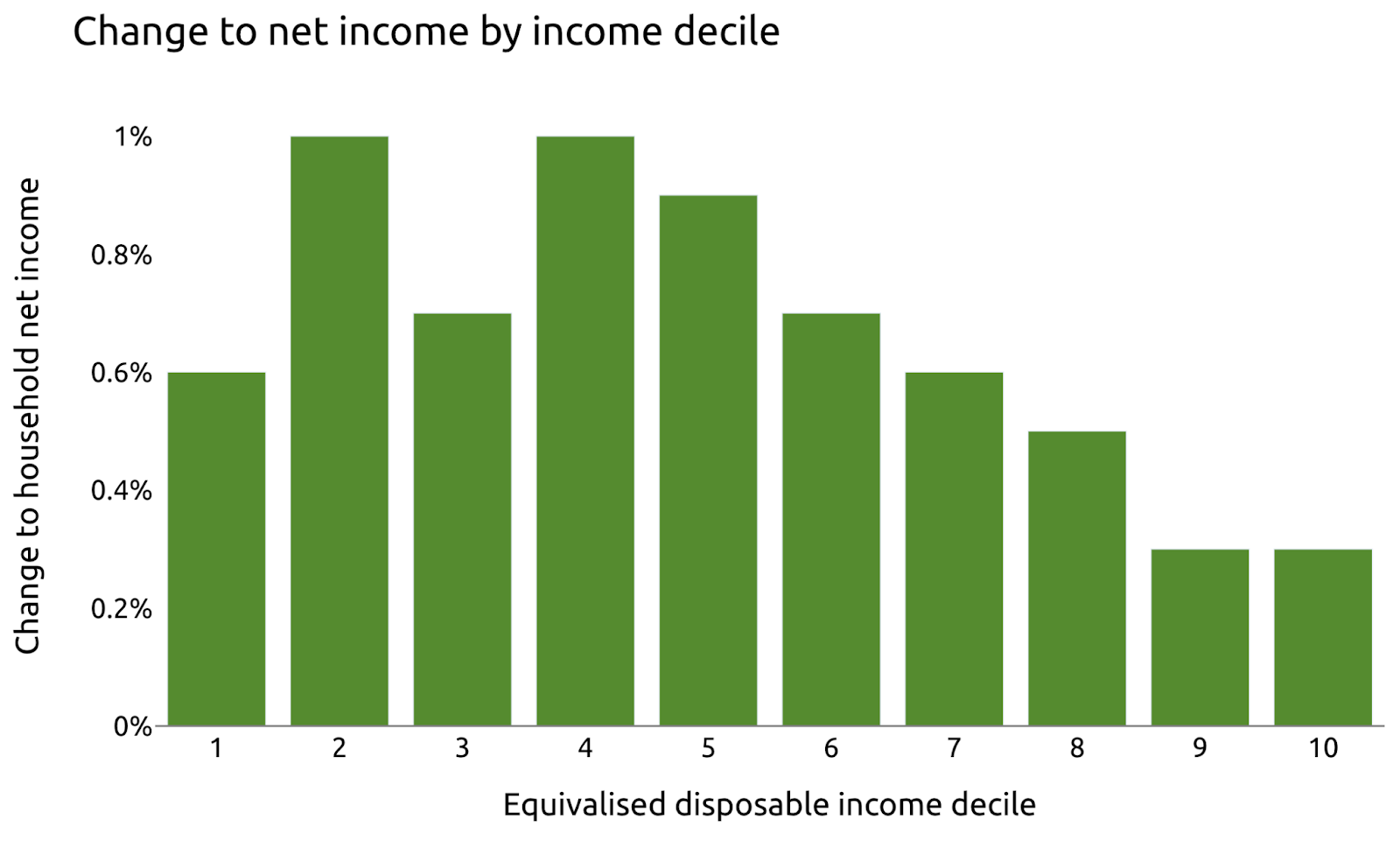

-The AFA is projected to provide an average benefit of [$1,115 per household](https://policyengine.org/us/policy?focus=policyOutput.distributionalImpact.incomeDecile.average&reform=82820®ion=us&timePeriod=2025&baseline=2&dataset=enhanced_cps). Families in the fifth decile would see the highest average benefit at $1,491, while the top decile would see the lowest gain of $524, due to the credit phaseouts. When examining average benefit by percent of net income, the [first decile receives the largest gain](https://policyengine.org/us/policy?focus=policyOutput.distributionalImpact.incomeDecile.relative&reform=82820®ion=us&timePeriod=2025&baseline=2&dataset=enhanced_cps), then decreases by each subsequent decile. In 2026, the average household benefit [increases to $1,540](https://policyengine.org/us/policy?focus=policyOutput.distributionalImpact.incomeDecile.average&reform=82820®ion=us&timePeriod=2026&baseline=2&dataset=enhanced_cps).

+The AFA is projected to provide an average benefit of [$1,115 per household](https://legacy.policyengine.org/us/policy?focus=policyOutput.distributionalImpact.incomeDecile.average&reform=82820®ion=us&timePeriod=2025&baseline=2&dataset=enhanced_cps). Families in the fifth decile would see the highest average benefit at $1,491, while the top decile would see the lowest gain of $524, due to the credit phaseouts. When examining average benefit by percent of net income, the [first decile receives the largest gain](https://legacy.policyengine.org/us/policy?focus=policyOutput.distributionalImpact.incomeDecile.relative&reform=82820®ion=us&timePeriod=2025&baseline=2&dataset=enhanced_cps), then decreases by each subsequent decile. In 2026, the average household benefit [increases to $1,540](https://legacy.policyengine.org/us/policy?focus=policyOutput.distributionalImpact.incomeDecile.average&reform=82820®ion=us&timePeriod=2026&baseline=2&dataset=enhanced_cps).

**Figure 3: Average Benefit of the AFA by Decile (2025 and 2026)**

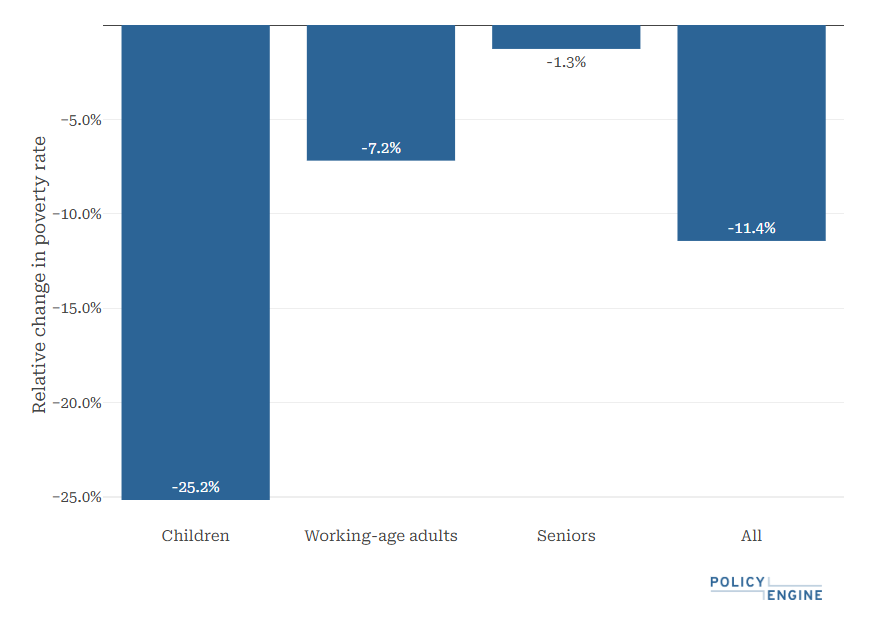

-The child tax credit expansion would [reduce poverty](https://policyengine.org/us/policy?focus=policyOutput.povertyImpact.regular.byAge&reform=82820®ion=us&timePeriod=2025&baseline=2&dataset=enhanced_cps) (as defined by the Supplemental Poverty Measure) by 11.4% and child poverty by 25.2% in 2025. Deep poverty and deep child poverty would [fall by 12.2% and 29.9%](https://policyengine.org/us/policy?focus=policyOutput.povertyImpact.deep.byAge&reform=82820®ion=us&timePeriod=2025&baseline=2&dataset=enhanced_cps), respectively. These poverty statistics vary by less than six percentage points across years in the 10-year budget window.

+The child tax credit expansion would [reduce poverty](https://legacy.policyengine.org/us/policy?focus=policyOutput.povertyImpact.regular.byAge&reform=82820®ion=us&timePeriod=2025&baseline=2&dataset=enhanced_cps) (as defined by the Supplemental Poverty Measure) by 11.4% and child poverty by 25.2% in 2025. Deep poverty and deep child poverty would [fall by 12.2% and 29.9%](https://legacy.policyengine.org/us/policy?focus=policyOutput.povertyImpact.deep.byAge&reform=82820®ion=us&timePeriod=2025&baseline=2&dataset=enhanced_cps), respectively. These poverty statistics vary by less than six percentage points across years in the 10-year budget window.

**Figure 4: Poverty Reduction Under the AFA (2025)**

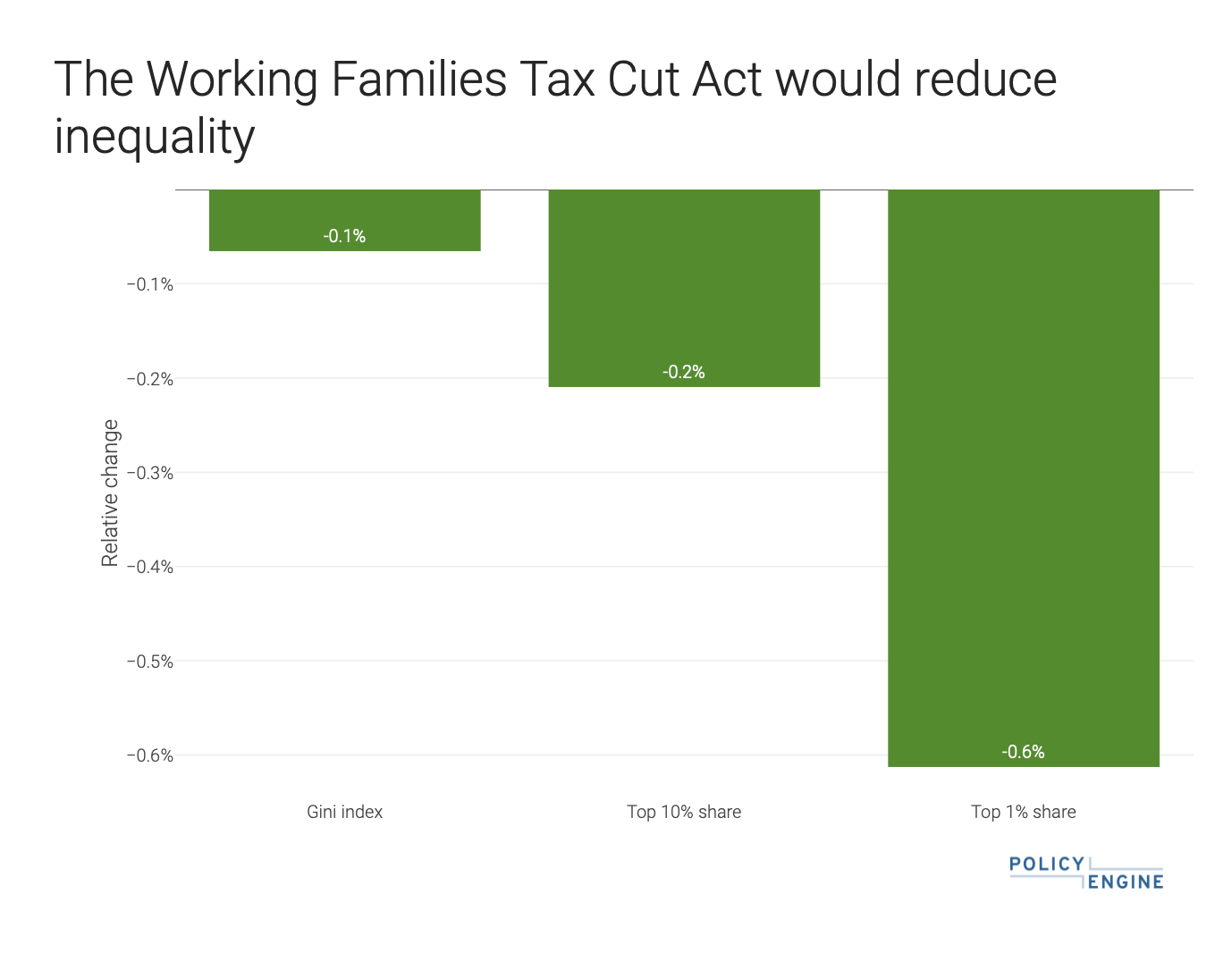

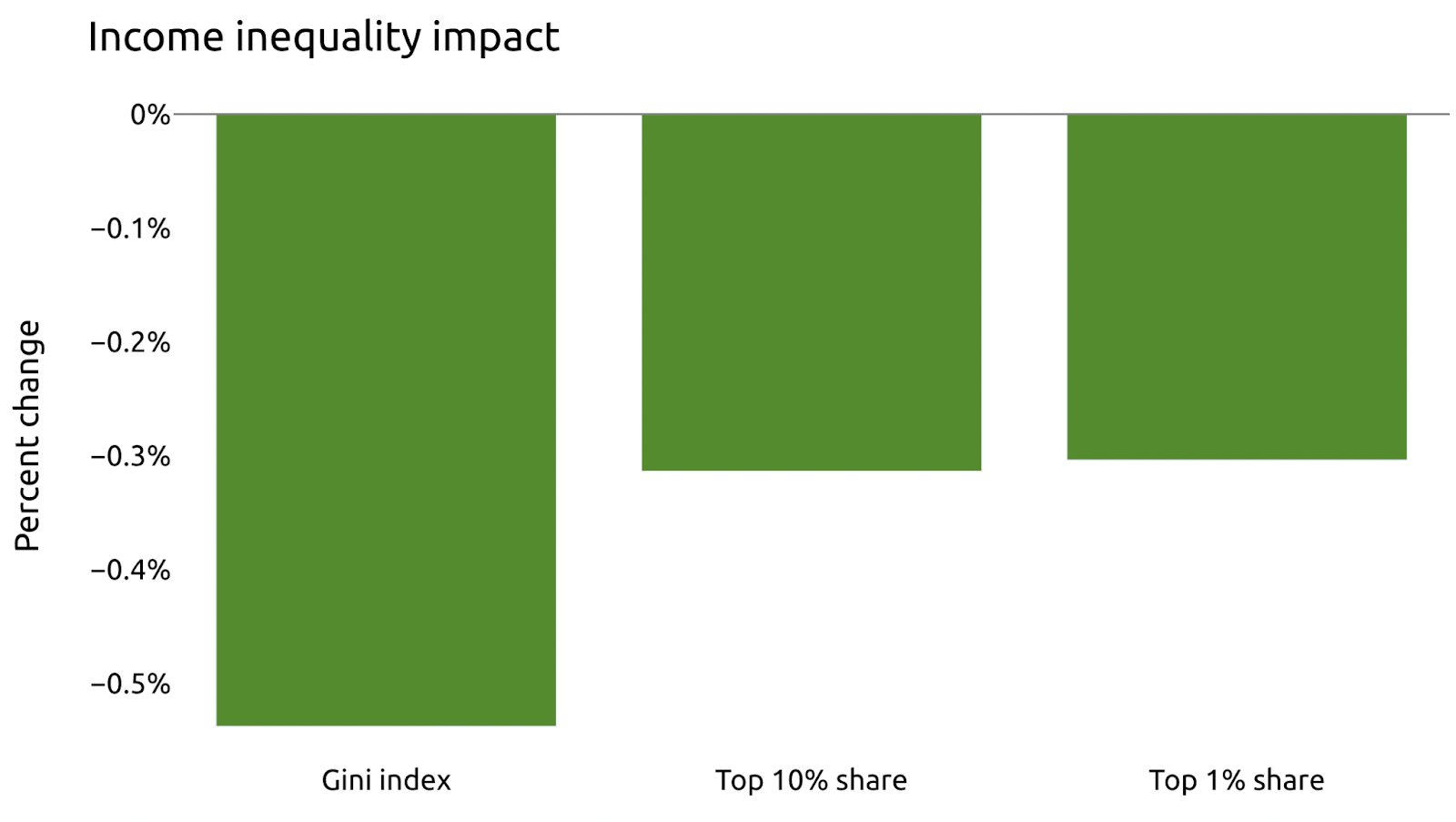

-Finally, the AFA will reduce the United States’ Gini index of inequality [by 2.4%](https://policyengine.org/us/policy?focus=policyOutput.inequalityImpact&reform=82820®ion=us&timePeriod=2025&baseline=2&dataset=enhanced_cps). The bill would also reduce the top 10% and 1%’s share of net income by 0.4% and 1.0%, respectively. In 2026, the Gini index is [projected to fall by 2.8%](https://policyengine.org/us/policy?focus=policyOutput.inequalityImpact&reform=82820®ion=us&timePeriod=2026&baseline=2&dataset=enhanced_cps).

+Finally, the AFA will reduce the United States’ Gini index of inequality [by 2.4%](https://legacy.policyengine.org/us/policy?focus=policyOutput.inequalityImpact&reform=82820®ion=us&timePeriod=2025&baseline=2&dataset=enhanced_cps). The bill would also reduce the top 10% and 1%’s share of net income by 0.4% and 1.0%, respectively. In 2026, the Gini index is [projected to fall by 2.8%](https://legacy.policyengine.org/us/policy?focus=policyOutput.inequalityImpact&reform=82820®ion=us&timePeriod=2026&baseline=2&dataset=enhanced_cps).

## Conclusion

@@ -124,4 +124,4 @@ The American Family Act will expand the Child Tax Credit by making the credit fu

As policymakers evaluate reforms such as these, analytical tools like PolicyEngine offer critical insights into the impacts on diverse household compositions and the broader economy.

-We invite you to explore our [additional analyses](https://policyengine.org/us/research) and use [PolicyEngine](https://policyengine.org/us) to calculate your own tax benefits or design custom policy reforms.

+We invite you to explore our [additional analyses](https://legacy.policyengine.org/us/research) and use [PolicyEngine](https://legacy.policyengine.org/us) to calculate your own tax benefits or design custom policy reforms.

diff --git a/src/posts/articles/american-worker-rebate-act.md b/src/posts/articles/american-worker-rebate-act.md

index 63655b639..4670f27cb 100644

--- a/src/posts/articles/american-worker-rebate-act.md

+++ b/src/posts/articles/american-worker-rebate-act.md

@@ -10,7 +10,7 @@ Our microsimulation model, assuming no changes to economic conditions, projects

- Expected to reduce the Gini index of inequality by 1.1%

-_Use PolicyEngine to [view the full results](https://policyengine.org/us/policy?focus=policyOutput.policyBreakdown®ion=us&timePeriod=2024&baseline=2&dataset=enhanced_cps&reform=89462) or calculate the [effect on your household](https://policyengine.org/us/household?focus=intro®ion=us&timePeriod=2024&baseline=2&dataset=enhanced_cps&reform=89462)._

+_Use PolicyEngine to [view the full results](https://legacy.policyengine.org/us/policy?focus=policyOutput.policyBreakdown®ion=us&timePeriod=2024&baseline=2&dataset=enhanced_cps&reform=89462) or calculate the [effect on your household](https://legacy.policyengine.org/us/household?focus=intro®ion=us&timePeriod=2024&baseline=2&dataset=enhanced_cps&reform=89462)._

## How the rebate works

@@ -22,9 +22,9 @@ Eligible households receive the full payment if their adjusted gross income (AGI

## Household impacts

-Let's examine how the AWRA's tariff rebates could affect a hypothetical U.S. family. A married couple in Florida with two children earning $100,000 would receive the [full $2,400 rebate](https://policyengine.org/us/household?focus=householdOutput.netIncome®ion=us&timePeriod=2024&baseline=2&dataset=enhanced_cps&reform=89462&household=55185) in 2026, assuming all family members have valid SSNs. However, if one parent does not meet the SSN requirement and does not qualify for the armed services exception, the entire household is ineligible and [receives no benefit](https://policyengine.org/us/household?focus=householdOutput.netIncome®ion=us&timePeriod=2024&baseline=2&dataset=enhanced_cps&reform=89462&household=55186). If one child lacks a valid SSN, the household still qualifies [for $1,800](https://policyengine.org/us/household?focus=householdOutput.netIncome®ion=us&timePeriod=2024&baseline=2&dataset=enhanced_cps&reform=89462&household=55197), the full amount minus $600 for the ineligible child.

+Let's examine how the AWRA's tariff rebates could affect a hypothetical U.S. family. A married couple in Florida with two children earning $100,000 would receive the [full $2,400 rebate](https://legacy.policyengine.org/us/household?focus=householdOutput.netIncome®ion=us&timePeriod=2024&baseline=2&dataset=enhanced_cps&reform=89462&household=55185) in 2026, assuming all family members have valid SSNs. However, if one parent does not meet the SSN requirement and does not qualify for the armed services exception, the entire household is ineligible and [receives no benefit](https://legacy.policyengine.org/us/household?focus=householdOutput.netIncome®ion=us&timePeriod=2024&baseline=2&dataset=enhanced_cps&reform=89462&household=55186). If one child lacks a valid SSN, the household still qualifies [for $1,800](https://legacy.policyengine.org/us/household?focus=householdOutput.netIncome®ion=us&timePeriod=2024&baseline=2&dataset=enhanced_cps&reform=89462&household=55197), the full amount minus $600 for the ineligible child.

-Additionally, if household earnings were to rise to $160,000, then the $2,400 benefit would [fall to $1,900](https://policyengine.org/us/household?focus=householdOutput.netIncome®ion=us&timePeriod=2024&baseline=2&dataset=enhanced_cps&reform=89462&household=55199) as the rebate phaseout would now apply. The entire benefit would phase out once the household's AGI [reaches $198,000](https://policyengine.org/us/household?focus=householdOutput.netIncome®ion=us&timePeriod=2024&baseline=2&dataset=enhanced_cps&reform=89462&household=55200).[^3] Table 1 summarizes the benefit amounts for each household scenario.

+Additionally, if household earnings were to rise to $160,000, then the $2,400 benefit would [fall to $1,900](https://legacy.policyengine.org/us/household?focus=householdOutput.netIncome®ion=us&timePeriod=2024&baseline=2&dataset=enhanced_cps&reform=89462&household=55199) as the rebate phaseout would now apply. The entire benefit would phase out once the household's AGI [reaches $198,000](https://legacy.policyengine.org/us/household?focus=householdOutput.netIncome®ion=us&timePeriod=2024&baseline=2&dataset=enhanced_cps&reform=89462&household=55200).[^3] Table 1 summarizes the benefit amounts for each household scenario.

**Table 1: Summary of Household Impacts for a Married Couple with Two Children**

@@ -50,27 +50,27 @@ Figure 2 shows how the AWRA alters the household's marginal tax rates. The house

## Microsimulation results

-Using data from tax year 2024, the American Worker Rebate Act of 2025 [would cost $141.3 billion](https://policyengine.org/us/policy?focus=policyOutput.budgetaryImpact.overall®ion=us&timePeriod=2024&baseline=2&dataset=enhanced_cps&reform=89462), according to PolicyEngine's static modeling. Due to interactions with state tax codes, the AWRA would also raise $58.9 million in state and local tax revenue.

+Using data from tax year 2024, the American Worker Rebate Act of 2025 [would cost $141.3 billion](https://legacy.policyengine.org/us/policy?focus=policyOutput.budgetaryImpact.overall®ion=us&timePeriod=2024&baseline=2&dataset=enhanced_cps&reform=89462), according to PolicyEngine's static modeling. Due to interactions with state tax codes, the AWRA would also raise $58.9 million in state and local tax revenue.

-The legislation would [raise the net income of 80.3%](https://policyengine.org/us/policy?focus=policyOutput.winnersAndLosers.incomeDecile®ion=us&timePeriod=2024&baseline=2&dataset=enhanced_cps&reform=89462) of residents in the U.S, though the degree to which they benefit varies by income decile. Overall, 30% of residents would experience a gain of more than 5% of their net income, including 93% of those in the lowest income decile. In the top income decile, 41% of residents would see a gain (all amounting to less than 5% in their net income).

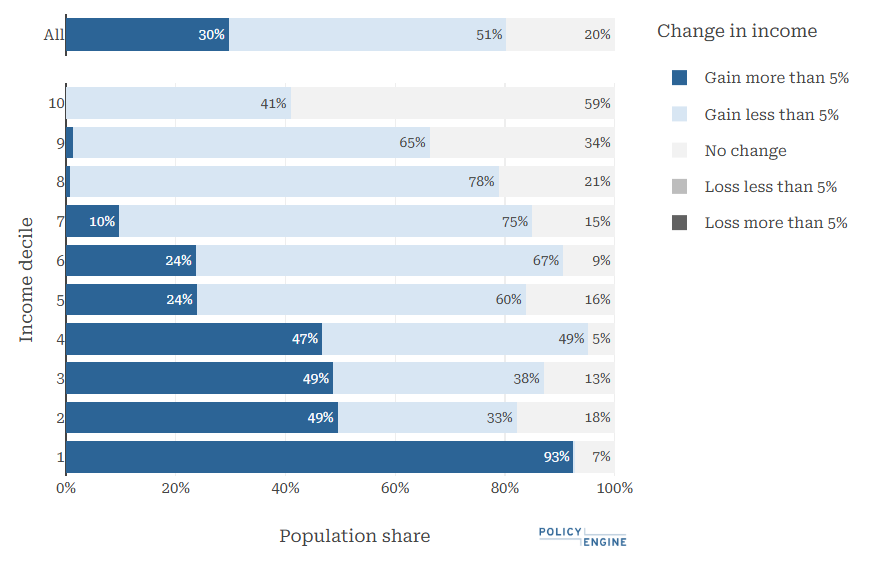

+The legislation would [raise the net income of 80.3%](https://legacy.policyengine.org/us/policy?focus=policyOutput.winnersAndLosers.incomeDecile®ion=us&timePeriod=2024&baseline=2&dataset=enhanced_cps&reform=89462) of residents in the U.S, though the degree to which they benefit varies by income decile. Overall, 30% of residents would experience a gain of more than 5% of their net income, including 93% of those in the lowest income decile. In the top income decile, 41% of residents would see a gain (all amounting to less than 5% in their net income).

**Figure 3: Winners of the AWRA's Tariff Rebates**

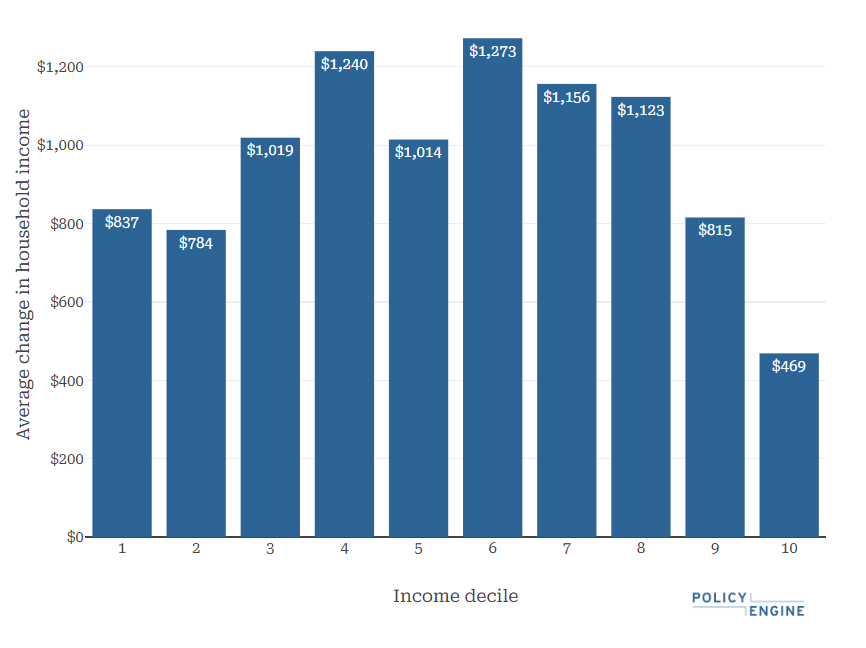

-The [average household benefit](https://policyengine.org/us/policy?focus=policyOutput.distributionalImpact.incomeDecile.average®ion=us&timePeriod=2024&baseline=2&dataset=enhanced_cps&reform=89462) of the AWRA would be $973. The decile experiencing the largest gain is the seventh ($1,273), while the tenth would benefit the least with an average benefit of $469. This is due to the phaseout of the rebates.

+The [average household benefit](https://legacy.policyengine.org/us/policy?focus=policyOutput.distributionalImpact.incomeDecile.average®ion=us&timePeriod=2024&baseline=2&dataset=enhanced_cps&reform=89462) of the AWRA would be $973. The decile experiencing the largest gain is the seventh ($1,273), while the tenth would benefit the least with an average benefit of $469. This is due to the phaseout of the rebates.

**Figure 4: Average Benefit of the AWRA's Tariff Rebates**

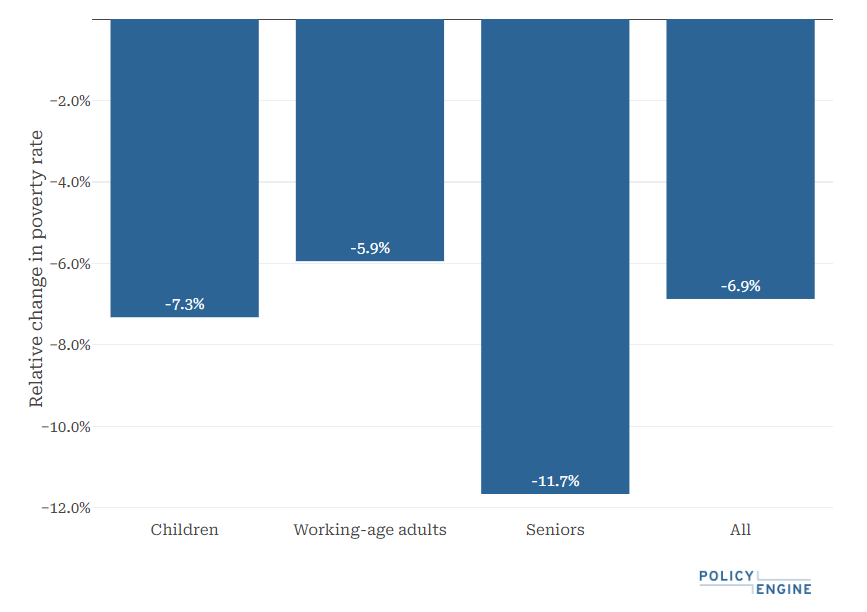

-We project the AWRA to [lower poverty](https://policyengine.org/us/policy?focus=policyOutput.povertyImpact.regular.byAge®ion=us&timePeriod=2024&baseline=2&dataset=enhanced_cps&reform=89462), as defined by the Supplemental Poverty Measure, by 6.9%, with seniors seeing the largest reduction at 11.7%. Deep poverty would [fall by 7.5%](https://policyengine.org/us/policy?focus=policyOutput.povertyImpact.deep.byAge®ion=us&timePeriod=2024&baseline=2&dataset=enhanced_cps&reform=89462), including a 15.2% reduction in deep child poverty.

+We project the AWRA to [lower poverty](https://legacy.policyengine.org/us/policy?focus=policyOutput.povertyImpact.regular.byAge®ion=us&timePeriod=2024&baseline=2&dataset=enhanced_cps&reform=89462), as defined by the Supplemental Poverty Measure, by 6.9%, with seniors seeing the largest reduction at 11.7%. Deep poverty would [fall by 7.5%](https://legacy.policyengine.org/us/policy?focus=policyOutput.povertyImpact.deep.byAge®ion=us&timePeriod=2024&baseline=2&dataset=enhanced_cps&reform=89462), including a 15.2% reduction in deep child poverty.

**Figure 5: Poverty Impact of the AWRA' Tariff Rebates**

-The proposed legislation would also [lower the Gini index of inequality](https://policyengine.org/us/policy?focus=policyOutput.inequalityImpact®ion=us&timePeriod=2024&baseline=2&dataset=enhanced_cps&reform=89462) by 1.07%, and lower the share of net income held by the top 10% and 1% households by 0.8% and 0.84%, respectively.

+The proposed legislation would also [lower the Gini index of inequality](https://legacy.policyengine.org/us/policy?focus=policyOutput.inequalityImpact®ion=us&timePeriod=2024&baseline=2&dataset=enhanced_cps&reform=89462) by 1.07%, and lower the share of net income held by the top 10% and 1% households by 0.8% and 0.84%, respectively.

## Conclusion

@@ -78,7 +78,7 @@ The American Worker Rebate Act of 2025 would send direct payments to qualifying

As policymakers evaluate reforms such as these, analytical tools like PolicyEngine offer critical insights into the impacts on diverse household compositions and the broader economy.

-We invite you to explore our [additional analyses](https://policyengine.org/us/research) and use [PolicyEngine](https://policyengine.org/us) to calculate your own tax benefits or design custom policy reforms.

+We invite you to explore our [additional analyses](https://legacy.policyengine.org/us/research) and use [PolicyEngine](https://legacy.policyengine.org/us) to calculate your own tax benefits or design custom policy reforms.

[^1]: Qualifying persons include the head and spouse of the household and any CTC-qualifying children. Adult dependents are not eligible for payments.

diff --git a/src/posts/articles/analysing-autumn-budget-universal-credit-reforms-with-policyengine.md b/src/posts/articles/analysing-autumn-budget-universal-credit-reforms-with-policyengine.md

index e15a91e1f..2454f4189 100644

--- a/src/posts/articles/analysing-autumn-budget-universal-credit-reforms-with-policyengine.md

+++ b/src/posts/articles/analysing-autumn-budget-universal-credit-reforms-with-policyengine.md

@@ -4,7 +4,7 @@ On Wednesday, the UK’s Chancellor of the Exchequer Rishi Sunak [published the

PolicyEngine estimates that this reform would cost £2.8bn per year, reduce poverty by 3.1%, and benefit 12% of the population. It will also reduce marginal tax rates by between 5.4pp and 63pp for people with income between the baseline work allowance and UC entitlement, while raising marginal tax rates by 37.4pp for people with income previously too high to receive UC.

-Read on for more details, or [jump to the reform in PolicyEngine](https://policyengine.org/uk/population-impact?UC_reduction_rate=55&UC_work_allowance_with_housing=335&UC_work_allowance_without_housing=557&policy_date=20211101) to see how the reform affects the UK population and your own household.

+Read on for more details, or [jump to the reform in PolicyEngine](https://legacy.policyengine.org/uk/population-impact?UC_reduction_rate=55&UC_work_allowance_with_housing=335&UC_work_allowance_without_housing=557&policy_date=20211101) to see how the reform affects the UK population and your own household.

## How Universal Credit works

@@ -28,7 +28,7 @@ The reforms announced in the budget reduce the taper rate by 8pp, from 63% to 55

### UK impact

-PolicyEngine estimates the total cost of introducing the reform to be £2.7bn per year. The reform benefits 12% of the population, and it reduces poverty by 3.1% (working-age poverty decreases by 3.0% and child poverty by 6.0%). For context, PolicyEngine estimates that [restoring Universal Credit’s pandemic-related Standard Allowance](https://policyengine.org/uk/population-impact?UC_couple_old=596.58&UC_couple_young=490.6&UC_single_old=411.51&UC_single_young=344) would cost £4.2bn, reduce poverty by 4.3%, and benefit 18% of the UK.

+PolicyEngine estimates the total cost of introducing the reform to be £2.7bn per year. The reform benefits 12% of the population, and it reduces poverty by 3.1% (working-age poverty decreases by 3.0% and child poverty by 6.0%). For context, PolicyEngine estimates that [restoring Universal Credit’s pandemic-related Standard Allowance](https://legacy.policyengine.org/uk/population-impact?UC_couple_old=596.58&UC_couple_young=490.6&UC_single_old=411.51&UC_single_young=344) would cost £4.2bn, reduce poverty by 4.3%, and benefit 18% of the UK.

Broadly, the reform is progressive; however, individuals in the first decile gain less than those in the second, third and fourth deciles, due to their lower likelihood to earn above the Work Allowance.

@@ -60,7 +60,7 @@ The reform lowers marginal tax rates more than it raises them, but its effect is

We’re pleased to share this first interactive analysis of the Autumn Budget UC reform, and the first to provide personalised household impacts. Our findings broadly resemble those from the [IFS](https://ifs.org.uk/uploads/Autumn-Budget-2021-Living-Standards-by-Xiaowei-Xu.pdf) and the [Resolution Foundation](https://www.resolutionfoundation.org/publications/the-boris-budget/), who also estimate the cost at around £3bn and identify similar distributional impacts.

-For more timely analysis of tax and benefit reforms, follow us here and on social media, and to create your own policy, try PolicyEngine at [policyengine.org.](https://policyengine.org/)

+For more timely analysis of tax and benefit reforms, follow us here and on social media, and to create your own policy, try PolicyEngine at [policyengine.org.](https://legacy.policyengine.org/)

_2021–11–04 update: This now reflects PolicyEngine 1.1.0, which incorporates Universal Credit’s minimum income floor for self-employed people._

diff --git a/src/posts/articles/analysis-of-guaranteed-income-for-the-21st-century.md b/src/posts/articles/analysis-of-guaranteed-income-for-the-21st-century.md

index c14d49fb3..d72b563dc 100644

--- a/src/posts/articles/analysis-of-guaranteed-income-for-the-21st-century.md

+++ b/src/posts/articles/analysis-of-guaranteed-income-for-the-21st-century.md

@@ -4,19 +4,19 @@ In this report, we depict the impact on a sample household, as well as on US-wid

Overall, we find that the reform would, in 2023:

-- [Cost $1.26 trillion](https://policyengine.org/us/policy?focus=policyOutput.netIncome&reform=1006®ion=us&timePeriod=2023&baseline=2)

+- [Cost $1.26 trillion](https://legacy.policyengine.org/us/policy?focus=policyOutput.netIncome&reform=1006®ion=us&timePeriod=2023&baseline=2)

-- [Benefit three in five Americans](https://policyengine.org/us/policy?focus=policyOutput.intraDecileImpact&reform=1006®ion=us&timePeriod=2023&baseline=2)

+- [Benefit three in five Americans](https://legacy.policyengine.org/us/policy?focus=policyOutput.intraDecileImpact&reform=1006®ion=us&timePeriod=2023&baseline=2)

-- [Cut poverty 94%](https://policyengine.org/us/policy?focus=policyOutput.povertyImpact&reform=1006®ion=us&timePeriod=2023&baseline=2)

+- [Cut poverty 94%](https://legacy.policyengine.org/us/policy?focus=policyOutput.povertyImpact&reform=1006®ion=us&timePeriod=2023&baseline=2)

-- [Lower the Gini index of income inequality 19%](https://policyengine.org/us/policy?focus=policyOutput.inequalityImpact&reform=1006®ion=us&timePeriod=2023&baseline=2)

+- [Lower the Gini index of income inequality 19%](https://legacy.policyengine.org/us/policy?focus=policyOutput.inequalityImpact&reform=1006®ion=us&timePeriod=2023&baseline=2)

-- [Increase the prevalence and severity of cliffs by 466% and 100%, respectively](https://policyengine.org/us/policy?focus=policyOutput.cliffImpact&reform=1006®ion=us&timePeriod=2023&baseline=2)

+- [Increase the prevalence and severity of cliffs by 466% and 100%, respectively](https://legacy.policyengine.org/us/policy?focus=policyOutput.cliffImpact&reform=1006®ion=us&timePeriod=2023&baseline=2)

This report describes and compares the New School’s proposal and analysis; calculates the impact for a sample household; and goes into these US-wide results in greater depth.

-[See how Guaranteed Income for the 21st Century would affect your household.](https://policyengine.org/us/household?focus=intro&reform=1006®ion=us&timePeriod=2023&baseline=2)

+[See how Guaranteed Income for the 21st Century would affect your household.](https://legacy.policyengine.org/us/household?focus=intro&reform=1006®ion=us&timePeriod=2023&baseline=2)

## The Guaranteed Income for the 21st Century proposal

@@ -26,7 +26,7 @@ _Guaranteed Income for the 21st Century_, or _21GI_ as the New School abbreviate

## Sample household

-Consider a [single parent of one child in New York City](https://policyengine.org/us/household?focus=householdOutput.earnings&reform=1006®ion=us&timePeriod=2023&baseline=2&household=31338). As they earn more, the net benefit of the 21GI falls, due to the shape of the EITC (in this case, federal, state, and local EITCs, since NYS and NYC based their EITCs on the federal), and the phase-out of the new payment itself.

+Consider a [single parent of one child in New York City](https://legacy.policyengine.org/us/household?focus=householdOutput.earnings&reform=1006®ion=us&timePeriod=2023&baseline=2&household=31338). As they earn more, the net benefit of the 21GI falls, due to the shape of the EITC (in this case, federal, state, and local EITCs, since NYS and NYC based their EITCs on the federal), and the phase-out of the new payment itself.

@@ -48,7 +48,7 @@ Our static microsimulation model, which applies 2023 tax and benefit rules to th

### Budgetary impact

-We project that 21GI would cost [$1.26 trillion](https://policyengine.org/us/policy?focus=policyOutput.netIncome&reform=1006®ion=us&timePeriod=2023&baseline=2), including the main benefit and the EITC elimination.

+We project that 21GI would cost [$1.26 trillion](https://legacy.policyengine.org/us/policy?focus=policyOutput.netIncome&reform=1006®ion=us&timePeriod=2023&baseline=2), including the main benefit and the EITC elimination.

This estimate exceeds the New School’s estimate of $876 billion by 43%. This discrepancy could result from multiple factors, including importantly the source dataset and tax filing unit assumption.

@@ -60,19 +60,19 @@ As an example, suppose a 22-year-old, who earns $30,000, lives with their parent

### Impact by income decile

-The reform would [add 11.7% to net incomes](https://policyengine.org/us/policy?focus=policyOutput.decileRelativeImpact&reform=1006®ion=us&timePeriod=2023&baseline=2) overall, and this percentage decreases with income, from 110% at the bottom decile to 0.7% at the top.

+The reform would [add 11.7% to net incomes](https://legacy.policyengine.org/us/policy?focus=policyOutput.decileRelativeImpact&reform=1006®ion=us&timePeriod=2023&baseline=2) overall, and this percentage decreases with income, from 110% at the bottom decile to 0.7% at the top.

### Distributional impacts

-21GI would [benefit 60% of the population](https://policyengine.org/us/policy?focus=policyOutput.intraDecileImpact&reform=1006®ion=us&timePeriod=2023&baseline=2), of whom 97% would gain at least 5% of net income. Over 99% of the bottom fifth would gain, as would 23% of those in the top decile (due to households that comprise multiple filing units).

+21GI would [benefit 60% of the population](https://legacy.policyengine.org/us/policy?focus=policyOutput.intraDecileImpact&reform=1006®ion=us&timePeriod=2023&baseline=2), of whom 97% would gain at least 5% of net income. Over 99% of the bottom fifth would gain, as would 23% of those in the top decile (due to households that comprise multiple filing units).

### Poverty

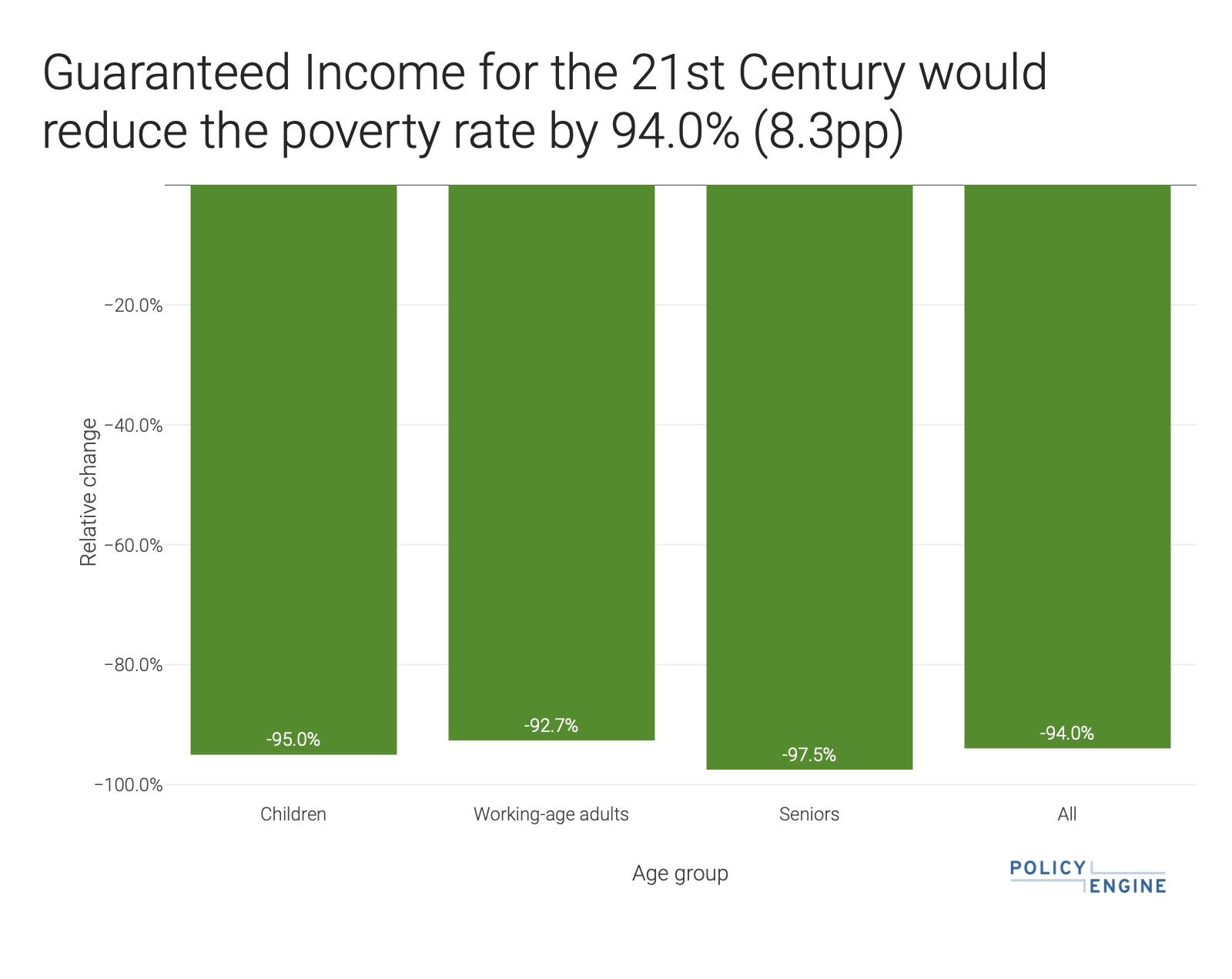

-Under 21GI, poverty would fall by [94% overall](https://policyengine.org/us/policy?focus=policyOutput.povertyImpact&reform=1006®ion=us&timePeriod=2023&baseline=2), and by at least 90% for most subgroups. [Deep poverty would also fall 99%](https://policyengine.org/us/policy?focus=policyOutput.deepPovertyImpact&reform=1006®ion=us&timePeriod=2023&baseline=2).

+Under 21GI, poverty would fall by [94% overall](https://legacy.policyengine.org/us/policy?focus=policyOutput.povertyImpact&reform=1006®ion=us&timePeriod=2023&baseline=2), and by at least 90% for most subgroups. [Deep poverty would also fall 99%](https://legacy.policyengine.org/us/policy?focus=policyOutput.deepPovertyImpact&reform=1006®ion=us&timePeriod=2023&baseline=2).

@@ -86,6 +86,6 @@ Under 21GI, poverty would fall by [94% overall](https://policyengine.org/us/poli

Currently, PolicyEngine estimates that 0.6% of households face a cliff, by which an additional $2,000 of earnings per adult would make the household financially worse off. We expect that this underestimates the prevalence of cliffs, since we have not yet modeled all tax and benefit programs that would increase marginal tax rates or introduce explicit cliffs.

-As a result of 21GI’s additional marginal tax rates, that rate of [cliffs would rise 466% to 3.3%](https://policyengine.org/us/policy?focus=policyOutput.cliffImpact&reform=1006®ion=us&timePeriod=2023&baseline=2) (one in 30 households). The total lost income from those facing cliffs would also double from $6 billion to $12 billion.

+As a result of 21GI’s additional marginal tax rates, that rate of [cliffs would rise 466% to 3.3%](https://legacy.policyengine.org/us/policy?focus=policyOutput.cliffImpact&reform=1006®ion=us&timePeriod=2023&baseline=2) (one in 30 households). The total lost income from those facing cliffs would also double from $6 billion to $12 billion.

diff --git a/src/posts/articles/analysis-of-the-spring-budget-2023.md b/src/posts/articles/analysis-of-the-spring-budget-2023.md

index 3379e0453..d65bbbbb4 100644

--- a/src/posts/articles/analysis-of-the-spring-budget-2023.md

+++ b/src/posts/articles/analysis-of-the-spring-budget-2023.md

@@ -1,4 +1,4 @@

-[See the full impact on PolicyEngine here.](https://policyengine.org/uk/policy?focus=policyOutput.inequalityImpact&reform=5847®ion=uk&timePeriod=2023&baseline=1544)

+[See the full impact on PolicyEngine here.](https://legacy.policyengine.org/uk/policy?focus=policyOutput.inequalityImpact&reform=5847®ion=uk&timePeriod=2023&baseline=1544)

Today saw the announcement of the 2023 Spring Budget for 2023, with significant changes to energy subsidies in particular. In this report, we analyse the budgetary, distributional, poverty, and inequality aspects of two of the largest reforms using data from the PolicyEngine UK microsimulation model.

diff --git a/src/posts/articles/automate-policy-analysis-with-policy-engines-new-chatgpt-integration.md b/src/posts/articles/automate-policy-analysis-with-policy-engines-new-chatgpt-integration.md

index ae55d9805..5d3a54cca 100644

--- a/src/posts/articles/automate-policy-analysis-with-policy-engines-new-chatgpt-integration.md

+++ b/src/posts/articles/automate-policy-analysis-with-policy-engines-new-chatgpt-integration.md

@@ -20,7 +20,7 @@ PolicyEngine provides style guidance (replaceable with your own), which includes

_Screenshot of the analysis prompt generator._

-The screenshot demonstrates an example policy reform prompt ([restoring the American Rescue Plan Act’s Earned Income Tax Credit expansion](http://policyengine.org/us/policy?focus=policyOutput.prompt&reform=6524®ion=us&timePeriod=2023&baseline=2)). ChatGPT’s unmodified analysis is provided at the end of the post.

+The screenshot demonstrates an example policy reform prompt ([restoring the American Rescue Plan Act’s Earned Income Tax Credit expansion](http://legacy.policyengine.org/us/policy?focus=policyOutput.prompt&reform=6524®ion=us&timePeriod=2023&baseline=2)). ChatGPT’s unmodified analysis is provided at the end of the post.

Utilizing GPT-4’s capabilities, we hope this integration streamlines policy analysis for researchers, allowing faster iteration. Both GPT-4 (available through [ChatGPT Plus](https://openai.com/blog/chatgpt-plus)) and GPT-3.5 (available on the [free ChatGPT tier](http://chat.openai.com/)) provide clear summaries. We’ve found that GPT-4 offers more clear and accurate results compared to GPT-3.5, although both deliver good outcomes. An example of GPT-3.5’s summary is available below for comparison.

diff --git a/src/posts/articles/autumn-budget-2024-employer-nic-pension-contributions.md b/src/posts/articles/autumn-budget-2024-employer-nic-pension-contributions.md

index 4bf3c9879..9cad6c5db 100644

--- a/src/posts/articles/autumn-budget-2024-employer-nic-pension-contributions.md

+++ b/src/posts/articles/autumn-budget-2024-employer-nic-pension-contributions.md

@@ -33,27 +33,27 @@ Under the ‘fixed employment cost’ assumption, the government receives £552

We apply this logic to all of the roughly 100,000 households in our representative microdata, aggregating the changes in tax liabilities and benefit entitlements. Under the static model, we estimate that revenues rise by around £18 billion per year, raising £90 billion over five years.

-| Year | Revenue impact (employer NICs) | Revenue impact (other) | Revenue impact | Wages |

-| :---------- | :----------------------------- | :--------------------- | :------------------------------------------------------------------------------------------------------------------------------ | :---- |

-| 2025 | 17.2 | 0 | [17.2](https://policyengine.org/uk/policy?focus=policyOutput.policyBreakdown&reform=69356®ion=uk&timePeriod=2025&baseline=1) | 0 |

-| 2026 | 17.7 | 0 | [17.7](https://policyengine.org/uk/policy?focus=policyOutput.policyBreakdown&reform=69356®ion=uk&timePeriod=2026&baseline=1) | 0 |

-| 2027 | 18.1 | 0 | [18.1](https://policyengine.org/uk/policy?focus=policyOutput.policyBreakdown&reform=69356®ion=uk&timePeriod=2027&baseline=1) | 0 |

-| 2028 | 18.4 | 0 | [18.4](https://policyengine.org/uk/policy?focus=policyOutput.policyBreakdown&reform=69356®ion=uk&timePeriod=2028&baseline=1) | 0 |

-| 2029 | 18.9 | 0 | [18.9](https://policyengine.org/uk/policy?focus=policyOutput.policyBreakdown&reform=69356®ion=uk&timePeriod=2029&baseline=1) | 0 |

-| **2025-29** | **90.3** | **0** | **90.3** | **0** |

+| Year | Revenue impact (employer NICs) | Revenue impact (other) | Revenue impact | Wages |

+| :---------- | :----------------------------- | :--------------------- | :------------------------------------------------------------------------------------------------------------------------------------- | :---- |

+| 2025 | 17.2 | 0 | [17.2](https://legacy.policyengine.org/uk/policy?focus=policyOutput.policyBreakdown&reform=69356®ion=uk&timePeriod=2025&baseline=1) | 0 |

+| 2026 | 17.7 | 0 | [17.7](https://legacy.policyengine.org/uk/policy?focus=policyOutput.policyBreakdown&reform=69356®ion=uk&timePeriod=2026&baseline=1) | 0 |

+| 2027 | 18.1 | 0 | [18.1](https://legacy.policyengine.org/uk/policy?focus=policyOutput.policyBreakdown&reform=69356®ion=uk&timePeriod=2027&baseline=1) | 0 |

+| 2028 | 18.4 | 0 | [18.4](https://legacy.policyengine.org/uk/policy?focus=policyOutput.policyBreakdown&reform=69356®ion=uk&timePeriod=2028&baseline=1) | 0 |

+| 2029 | 18.9 | 0 | [18.9](https://legacy.policyengine.org/uk/policy?focus=policyOutput.policyBreakdown&reform=69356®ion=uk&timePeriod=2029&baseline=1) | 0 |

+| **2025-29** | **90.3** | **0** | **90.3** | **0** |

If employers pass on NICs in the form of reduced wages, we estimate that employer NIC revenues rise by around £15 billion per year, but are offset by on average £5 billion per year in personal tax liabilities and benefit entitlements as a result of the (average) £15 billion in wage reductions.

Overall, this raises £9.6 billion in 2025, totalling £50 billion over five years.

-| Year | Revenue impact (Employer NICs) | Revenue impact (other) | Revenue impact | Wages |

-| :---------- | :----------------------------- | :--------------------- | :------------------------------------------------------------------------------------------------------------------------------ | :--------- |

-| 2025 | 15.1 | \-5.5 | [9.6](https://policyengine.org/uk/policy?focus=policyOutput.policyBreakdown&reform=69355®ion=uk&timePeriod=2025&baseline=1) | \-15.2 |

-| 2026 | 15.6 | \-5.8 | [9.8](https://policyengine.org/uk/policy?focus=policyOutput.policyBreakdown&reform=69355®ion=uk&timePeriod=2026&baseline=1) | \-15.7 |

-| 2027 | 15.9 | \-6.0 | [9.9](https://policyengine.org/uk/policy?focus=policyOutput.policyBreakdown&reform=69355®ion=uk&timePeriod=2027&baseline=1) | \-16.0 |

-| 2028 | 16.2 | \-6.1 | [10.1](https://policyengine.org/uk/policy?focus=policyOutput.policyBreakdown&reform=69355®ion=uk&timePeriod=2028&baseline=1) | \-16.3 |

-| 2029 | 16.6 | \-6.3 | [10.3](https://policyengine.org/uk/policy?focus=policyOutput.policyBreakdown&reform=69355®ion=uk&timePeriod=2029&baseline=1) | \-16.7 |

-| **2025-29** | **79.4** | **\-29.7** | **49.7** | **\-79.9** |

+| Year | Revenue impact (Employer NICs) | Revenue impact (other) | Revenue impact | Wages |

+| :---------- | :----------------------------- | :--------------------- | :------------------------------------------------------------------------------------------------------------------------------------- | :--------- |

+| 2025 | 15.1 | \-5.5 | [9.6](https://legacy.policyengine.org/uk/policy?focus=policyOutput.policyBreakdown&reform=69355®ion=uk&timePeriod=2025&baseline=1) | \-15.2 |

+| 2026 | 15.6 | \-5.8 | [9.8](https://legacy.policyengine.org/uk/policy?focus=policyOutput.policyBreakdown&reform=69355®ion=uk&timePeriod=2026&baseline=1) | \-15.7 |

+| 2027 | 15.9 | \-6.0 | [9.9](https://legacy.policyengine.org/uk/policy?focus=policyOutput.policyBreakdown&reform=69355®ion=uk&timePeriod=2027&baseline=1) | \-16.0 |

+| 2028 | 16.2 | \-6.1 | [10.1](https://legacy.policyengine.org/uk/policy?focus=policyOutput.policyBreakdown&reform=69355®ion=uk&timePeriod=2028&baseline=1) | \-16.3 |

+| 2029 | 16.6 | \-6.3 | [10.3](https://legacy.policyengine.org/uk/policy?focus=policyOutput.policyBreakdown&reform=69355®ion=uk&timePeriod=2029&baseline=1) | \-16.7 |

+| **2025-29** | **79.4** | **\-29.7** | **49.7** | **\-79.9** |

## Employee pass-through sensitivity

diff --git a/src/posts/articles/autumn-budget-2024-policy-choices.ipynb b/src/posts/articles/autumn-budget-2024-policy-choices.ipynb

index 312058bfa..e20293154 100644

--- a/src/posts/articles/autumn-budget-2024-policy-choices.ipynb

+++ b/src/posts/articles/autumn-budget-2024-policy-choices.ipynb

@@ -6,7 +6,7 @@

"source": [

"*Image credit: The Labour Party*\n",

"\n",

- "*See the full impact estimate for 2025 [here](https://policyengine.org/uk/policy?reform=68829&focus=policyOutput.policyBreakdown®ion=uk&timePeriod=2025&baseline=1).*\n",

+ "*See the full impact estimate for 2025 [here](https://legacy.policyengine.org/uk/policy?reform=68829&focus=policyOutput.policyBreakdown®ion=uk&timePeriod=2025&baseline=1).*\n",

"\n",

"\n",

"## Key findings\n",

@@ -32,7 +32,7 @@

"\n",

"### Private school VAT\n",

"\n",

- "In their manifesto, Labour also committed to levying VAT (as well as business rates) on private school fees from FY2025. We estimate this raises around £1.5 billion per year, assuming no behavioural responses, mostly from higher-income deciles. Read more detail about the policy in our recently-published report [here](https://policyengine.org/uk/research/school-vat).\n",

+ "In their manifesto, Labour also committed to levying VAT (as well as business rates) on private school fees from FY2025. We estimate this raises around £1.5 billion per year, assuming no behavioural responses, mostly from higher-income deciles. Read more detail about the policy in our recently-published report [here](https://legacy.policyengine.org/uk/research/school-vat).\n",

"\n",

"\n",

"### Employer NICs\n",

@@ -52,7 +52,7 @@

"\n",

"## Economic impacts\n",

"\n",

- "PolicyEngine [estimates](https://policyengine.org/uk/policy?reform=68829&focus=policyOutput.policyBreakdown®ion=uk&timePeriod=2025&baseline=1) that these reforms combined would raise £25 billion per year over five years, with over half of the revenue impact from the employer NICs reform. The table below summarises these reforms’ impacts over the budget window (with the behavioural responses as stated previously).\n",

+ "PolicyEngine [estimates](https://legacy.policyengine.org/uk/policy?reform=68829&focus=policyOutput.policyBreakdown®ion=uk&timePeriod=2025&baseline=1) that these reforms combined would raise £25 billion per year over five years, with over half of the revenue impact from the employer NICs reform. The table below summarises these reforms’ impacts over the budget window (with the behavioural responses as stated previously).\n",

"\n",

"\n",

"| Year | 2025 | 2026 | 2027 | 2028 | 2029 | 2025-29 |\n",

@@ -61,7 +61,7 @@

"| Levy private school VAT | 1.5 | 1.5 | 1.5 | 1.6 | 1.6 | 7.7 |\n",

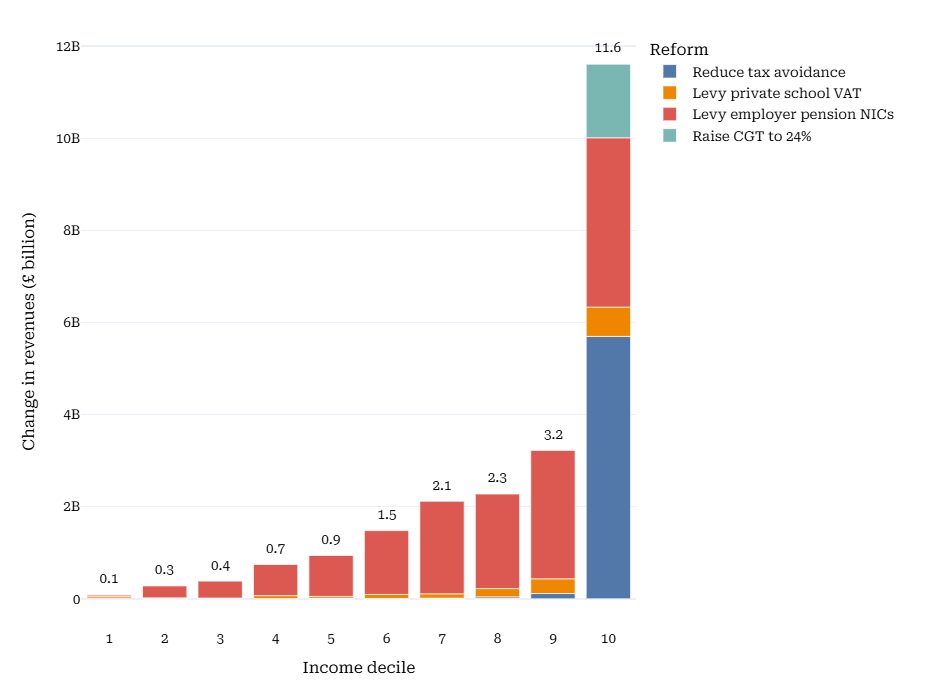

"| Raise CGT to 24% | 1.6 | 1.9 | 2.0 | 2.3 | 2.3 | 10.1 |\n",

"| Reduce tax avoidance | 5.9 | 5.9 | 5.9 | 5.9 | 5.9 | 29.5 |\n",

- "| **Total** | **[23.1](https://policyengine.org/uk/policy?reform=69049&focus=policyOutput.distributionalImpact.incomeDecile.relative®ion=uk&timePeriod=2025&baseline=1)** | **23.1** | **22.6** | **22.4** | **22.7** | **113.9** |"

+ "| **Total** | **[23.1](https://legacy.policyengine.org/uk/policy?reform=69049&focus=policyOutput.distributionalImpact.incomeDecile.relative®ion=uk&timePeriod=2025&baseline=1)** | **23.1** | **22.6** | **22.4** | **22.7** | **113.9** |"

]

},

{

diff --git a/src/posts/articles/autumn-budget-24-employer-ni.md b/src/posts/articles/autumn-budget-24-employer-ni.md

index f24599bbb..ea6463c02 100644

--- a/src/posts/articles/autumn-budget-24-employer-ni.md

+++ b/src/posts/articles/autumn-budget-24-employer-ni.md

@@ -1,6 +1,6 @@

_Credit: World Economic Forum/Walter Duerst_

-[See the full impact on PolicyEngine here.](https://policyengine.org/uk/policy?reform=69728&focus=policyOutput.policyBreakdown®ion=uk&timePeriod=2025&baseline=1)

+[See the full impact on PolicyEngine here.](https://legacy.policyengine.org/uk/policy?reform=69728&focus=policyOutput.policyBreakdown®ion=uk&timePeriod=2025&baseline=1)

The Chancellor Rachel Reeves has announced reforms to employer National Insurance (NI) contributions, marking the most substantial revenue-raising measure in the Autumn Budget 2024. The changes include raising the main rate from 13.8% to 15.0% while simultaneously lowering the Secondary Threshold at which employers begin contributing from £9,100 to £5,000 per year. Additionally, Reeves has raised the [Employment Allowance](https://www.gov.uk/claim-employment-allowance) from £5,000 to £10,000 and eliminated its cap. This analysis focuses on the rate rise and threshold reduction.

diff --git a/src/posts/articles/autumn-budget-24-fuel-duty.md b/src/posts/articles/autumn-budget-24-fuel-duty.md

index a76a726d6..f04ed4f46 100644

--- a/src/posts/articles/autumn-budget-24-fuel-duty.md

+++ b/src/posts/articles/autumn-budget-24-fuel-duty.md

@@ -1,4 +1,4 @@

-_[See the full impact on PolicyEngine here.](https://policyengine.org/uk/policy?focus=policyOutput.policyBreakdown&reform=69734®ion=uk&timePeriod=2025&baseline=1)_

+_[See the full impact on PolicyEngine here.](https://legacy.policyengine.org/uk/policy?focus=policyOutput.policyBreakdown&reform=69734®ion=uk&timePeriod=2025&baseline=1)_

Chancellor Rachel Reeves today confirmed that duty will remain frozen at £0.5295 per litre for FY 2025, before rising with retail price inflation in future years, continuing a policy approach that has been maintained for several years.

diff --git a/src/posts/articles/autumn-statement-2023.md b/src/posts/articles/autumn-statement-2023.md

index d546e2151..a2ebccc15 100644

--- a/src/posts/articles/autumn-statement-2023.md

+++ b/src/posts/articles/autumn-statement-2023.md

@@ -1,4 +1,4 @@

-_See the Autumn Statement 2023 on PolicyEngine [here](https://policyengine.org/uk/policy?focus=policyOutput.netIncome&reform=37636®ion=uk&timePeriod=2024&baseline=1)._

+_See the Autumn Statement 2023 on PolicyEngine [here](https://legacy.policyengine.org/uk/policy?focus=policyOutput.netIncome&reform=37636®ion=uk&timePeriod=2024&baseline=1)._

Today, the Chancellor of the Exchequer Jeremy Hunt delivered the annual [Autumn Statement](https://assets.publishing.service.gov.uk/media/655d0a83544aea000dfb321d/Autumn_Statement_2023_Policy_Costings_-_Final.pdf), in which he announced several tax and benefit reforms, including two to National Insurance Contributions (NICs):

@@ -8,7 +8,7 @@ Today, the Chancellor of the Exchequer Jeremy Hunt delivered the annual [Autumn

In this post, we'll use PolicyEngine to estimate the budgetary, distributional and poverty impacts of these reforms.

-_See how the combined reforms would affect your own household using our [personalised calculator](https://policyengine.org/uk/household?focus=intro&reform=37636®ion=uk&timePeriod=2023&baseline=1)_

+_See how the combined reforms would affect your own household using our [personalised calculator](https://legacy.policyengine.org/uk/household?focus=intro&reform=37636®ion=uk&timePeriod=2023&baseline=1)_

## Autumn Budget 2023 reforms

@@ -36,7 +36,7 @@ Non-State Pension benefits will rise by 6.7%, the inflation rate as measured by

In its [Autumn Statement 2023 Policy Costings document](https://assets.publishing.service.gov.uk/media/655d0a83544aea000dfb321d/Autumn_Statement_2023_Policy_Costings_-_Final.pdf#page=64), HM Treasury defines its _Default indexation assumed in the baseline_ as above. Since HM Treasury treats these announcements as following defaults rather than reforms, we follow suit and have only updated the baseline.

-Compared to a counterfactual where benefits are not uprated at all, we estimate that this set of upratings will [cost £5.9 billion in 2024](https://policyengine.org/uk/policy?focus=policyOutput.netIncome&timePeriod=2024®ion=uk&reform=1&baseline=37721).

+Compared to a counterfactual where benefits are not uprated at all, we estimate that this set of upratings will [cost £5.9 billion in 2024](https://legacy.policyengine.org/uk/policy?focus=policyOutput.netIncome&timePeriod=2024®ion=uk&reform=1&baseline=37721).

### Other reforms

@@ -46,7 +46,7 @@ He notably did _not_ announce reforms that outlets had previously reported he wa

## Household impacts of NIC cuts

-For a [single person with only employment income](https://policyengine.org/uk/household?focus=householdOutput.earnings&reform=37636®ion=uk&timePeriod=2023&baseline=1&household=32608), this reform produces a benefit if they earn at least £12,570. It would produce the maximum benefit of £377 if they earn at least £50,500.

+For a [single person with only employment income](https://legacy.policyengine.org/uk/household?focus=householdOutput.earnings&reform=37636®ion=uk&timePeriod=2023&baseline=1&household=32608), this reform produces a benefit if they earn at least £12,570. It would produce the maximum benefit of £377 if they earn at least £50,500.

@@ -54,7 +54,7 @@ These reforms lower marginal tax rates for individuals earning within that regio

-_See how the National Insurance cuts would affect your own household using our [personalised calculator](https://policyengine.org/uk/household?focus=intro&reform=37636®ion=uk&timePeriod=2023&baseline=1)._

+_See how the National Insurance cuts would affect your own household using our [personalised calculator](https://legacy.policyengine.org/uk/household?focus=intro&reform=37636®ion=uk&timePeriod=2023&baseline=1)._

## Societal impact of NIC cuts

@@ -62,29 +62,29 @@ Applying the PolicyEngine microsimulation model, we can estimate the impact of t

### Budgetary impacts

-Our microsimulation model projects that this NI cut will [cost £10.5 billion](https://policyengine.org/uk/policy?focus=policyOutput.netIncome&reform=37636®ion=uk&timePeriod=2024&baseline=1) in 2024.

+Our microsimulation model projects that this NI cut will [cost £10.5 billion](https://legacy.policyengine.org/uk/policy?focus=policyOutput.netIncome&reform=37636®ion=uk&timePeriod=2024&baseline=1) in 2024.

Our estimates exceed those from HM Treasury by about 12%, disproportionately due to Class 4 NICs. This largely results from our static model, compared to HM Treasury's behavioural responses, which assume that earnings will rise in response to lower tax rates. However, unlike HM Treasury, we also model the impact on benefits, which lowers our cost estimate: as benefits are calculated on post-tax income, tax cuts reduce benefits payments.

-| Reform | HM Treasury | PolicyEngine | Relative difference | PolicyEngine link |

-| ---------------------------------- | ----------- | ------------ | ------------------- | --------------------------------------------------------------------------------------------------------------------------- |

-| Lower Class 1 NICs from 12% to 10% | 8.72 | 9.69 | 11.2% | [#28973](https://policyengine.org/uk/policy?focus=policyOutput.netIncome&reform=28973®ion=uk&timePeriod=2024&baseline=1) |

-| Lower Class 4 NICs from 9% to 8% | 0.35 | 0.44 | 26.9% | [#37642](https://policyengine.org/uk/policy?focus=policyOutput.netIncome&reform=37642®ion=uk&timePeriod=2024&baseline=1) |

-| Abolish Class 2 NICs | 0.38 | 0.41 | 8.8% | [#37665](https://policyengine.org/uk/policy?focus=policyOutput.netIncome&reform=37665®ion=uk&timePeriod=2024&baseline=1) |

-| Total | 9.44 | 10.54 | 11.7% | [#37636](https://policyengine.org/uk/policy?focus=policyOutput.netIncome&reform=37636®ion=uk&timePeriod=2024&baseline=1) |

+| Reform | HM Treasury | PolicyEngine | Relative difference | PolicyEngine link |

+| ---------------------------------- | ----------- | ------------ | ------------------- | ---------------------------------------------------------------------------------------------------------------------------------- |

+| Lower Class 1 NICs from 12% to 10% | 8.72 | 9.69 | 11.2% | [#28973](https://legacy.policyengine.org/uk/policy?focus=policyOutput.netIncome&reform=28973®ion=uk&timePeriod=2024&baseline=1) |

+| Lower Class 4 NICs from 9% to 8% | 0.35 | 0.44 | 26.9% | [#37642](https://legacy.policyengine.org/uk/policy?focus=policyOutput.netIncome&reform=37642®ion=uk&timePeriod=2024&baseline=1) |

+| Abolish Class 2 NICs | 0.38 | 0.41 | 8.8% | [#37665](https://legacy.policyengine.org/uk/policy?focus=policyOutput.netIncome&reform=37665®ion=uk&timePeriod=2024&baseline=1) |

+| Total | 9.44 | 10.54 | 11.7% | [#37636](https://legacy.policyengine.org/uk/policy?focus=policyOutput.netIncome&reform=37636®ion=uk&timePeriod=2024&baseline=1) |

### Distributional impacts

-Households in the bottom income decile would [gain an average of £12](https://policyengine.org/uk/policy?focus=policyOutput.decileAverageImpact&reform=37636®ion=uk&timePeriod=2024&baseline=1), while those in the top decile would gain an average of £1,067.

+Households in the bottom income decile would [gain an average of £12](https://legacy.policyengine.org/uk/policy?focus=policyOutput.decileAverageImpact&reform=37636®ion=uk&timePeriod=2024&baseline=1), while those in the top decile would gain an average of £1,067.

-As a result of the reform, [66% of the population](https://policyengine.org/uk/policy?focus=policyOutput.intraDecileImpact&reform=37636®ion=uk&timePeriod=2024&baseline=1) would see their household net income rise, disproportionately those in higher-income households: around 90% of the top three deciles benefit, compared to around 25% of the bottom three.

+As a result of the reform, [66% of the population](https://legacy.policyengine.org/uk/policy?focus=policyOutput.intraDecileImpact&reform=37636®ion=uk&timePeriod=2024&baseline=1) would see their household net income rise, disproportionately those in higher-income households: around 90% of the top three deciles benefit, compared to around 25% of the bottom three.

-The reform has a [small, ambiguous effect on income inequality](https://policyengine.org/uk/policy?focus=policyOutput.inequalityImpact&reform=37636®ion=uk&timePeriod=2024&baseline=1): while the Gini index rises by 0.4%, the top 1% share of income falls by 0.4%. It [does not affect cliffs](https://policyengine.org/uk/policy?focus=policyOutput.cliffImpact&reform=37636®ion=uk&timePeriod=2024&baseline=1). Absolute, before-housing-costs [poverty falls by 0.5%](https://policyengine.org/uk/policy?focus=policyOutput.povertyImpact&reform=37636®ion=uk&timePeriod=2024&baseline=1), or around 60,000 individuals.

+The reform has a [small, ambiguous effect on income inequality](https://legacy.policyengine.org/uk/policy?focus=policyOutput.inequalityImpact&reform=37636®ion=uk&timePeriod=2024&baseline=1): while the Gini index rises by 0.4%, the top 1% share of income falls by 0.4%. It [does not affect cliffs](https://legacy.policyengine.org/uk/policy?focus=policyOutput.cliffImpact&reform=37636®ion=uk&timePeriod=2024&baseline=1). Absolute, before-housing-costs [poverty falls by 0.5%](https://legacy.policyengine.org/uk/policy?focus=policyOutput.povertyImpact&reform=37636®ion=uk&timePeriod=2024&baseline=1), or around 60,000 individuals.

## Conclusion

-In summary, PolicyEngine estimates the Autumn Budget 2023's National Insurance reforms will cost £10.5 billion in 2024, and will benefit two in three Britons, disproportionately those in higher-income households. We project a small, ambiguous effect on income inequality, and a 0.5% poverty reduction. We invite readers to use our [personalised calculator](https://policyengine.org/uk/household?focus=intro&reform=37636®ion=uk&timePeriod=2023&baseline=1) to estimate the impact on their own household, and to follow our work for more analyses of current tax and benefit policies.

+In summary, PolicyEngine estimates the Autumn Budget 2023's National Insurance reforms will cost £10.5 billion in 2024, and will benefit two in three Britons, disproportionately those in higher-income households. We project a small, ambiguous effect on income inequality, and a 0.5% poverty reduction. We invite readers to use our [personalised calculator](https://legacy.policyengine.org/uk/household?focus=intro&reform=37636®ion=uk&timePeriod=2023&baseline=1) to estimate the impact on their own household, and to follow our work for more analyses of current tax and benefit policies.

diff --git a/src/posts/articles/behavioural-responses.md b/src/posts/articles/behavioural-responses.md

index 1a9c551b0..4f21d3a0c 100644

--- a/src/posts/articles/behavioural-responses.md

+++ b/src/posts/articles/behavioural-responses.md

@@ -24,7 +24,7 @@ Unlike the [OBR](https://obr.uk/docs/dlm_uploads/NICS-Cut-Impact-on-Labour-Suppl

### An illustrative example

-To understand how these elasticities work, consider a worker earning £30,000 per year. This worker currently faces a marginal tax rate of [28%](https://policyengine.org/uk/household?focus=householdOutput.netIncome&household=49381) (combining income tax and National Insurance) and takes home [£24,961](https://policyengine.org/uk/household?focus=householdOutput.netIncome&household=49381) after taxes and transfers. At the current tax rates, this worker's net-of-tax wage rate is 72% of her gross wage. Now imagine a new policy that increases basic income tax by 1p (from 20% to 21%). In this case, PolicyEngine calculates that this new policy decreases her net income by [£175](https://policyengine.org/uk/household?focus=householdOutput.netIncome&reform=53461®ion=uk&timePeriod=2025&baseline=1&household=49381).

+To understand how these elasticities work, consider a worker earning £30,000 per year. This worker currently faces a marginal tax rate of [28%](https://legacy.policyengine.org/uk/household?focus=householdOutput.netIncome&household=49381) (combining income tax and National Insurance) and takes home [£24,961](https://legacy.policyengine.org/uk/household?focus=householdOutput.netIncome&household=49381) after taxes and transfers. At the current tax rates, this worker's net-of-tax wage rate is 72% of her gross wage. Now imagine a new policy that increases basic income tax by 1p (from 20% to 21%). In this case, PolicyEngine calculates that this new policy decreases her net income by [£175](https://legacy.policyengine.org/uk/household?focus=householdOutput.netIncome&reform=53461®ion=uk&timePeriod=2025&baseline=1&household=49381).

For this worker earning £14.42 per hour (£30,000/2,080 hours), the take-home pay per extra hour drops from £10.38 to £10.21 under the new policy – a 1.6% decrease. Using PolicyEngine's central estimates, we calculate two effects:

@@ -46,7 +46,7 @@ By default, the PolicyEngine web app assumes no behavioural responses. When user

## Comparing static and dynamic analysis

-Here we demonstrate how incorporating behavioural responses affects policy analysis by examining a tax reform proposed by the UK government in October 2024: change to Capital Gains Tax. For a detailed analysis of this and other reforms proposed in the Autumn Budget, see [PolicyEngine's reform impact analysis](https://policyengine.org/uk/research/autumn-budget-2024-policy-choices).

+Here we demonstrate how incorporating behavioural responses affects policy analysis by examining a tax reform proposed by the UK government in October 2024: change to Capital Gains Tax. For a detailed analysis of this and other reforms proposed in the Autumn Budget, see [PolicyEngine's reform impact analysis](https://legacy.policyengine.org/uk/research/autumn-budget-2024-policy-choices).

In estimating the impacts of this reform, we model how individuals with capital gains respond to changes in their marginal tax rate. The table below compares the five-year revenue impacts under both static and dynamic scenarios.

@@ -62,7 +62,7 @@ In this report, we present how PolicyEngine models three behavioural responses:

2. **Substitution effect for labour supply: 0.25 elasticity** (a 10% increase to the net marginal wage increases work hours by 2.5%)

3. **Capital gains response: \-0.7 elasticity** (a 10% increase in the marginal tax rate with respect to capital gains reduces capital gains by 7%)

-While this report focuses on these three core elasticities, PolicyEngine is expanding its behavioural modelling capabilities. For instance, we developed responses to [employer National Insurance contributions](https://policyengine.org/uk/research/autumn-budget-24-employer-ni), indicating the extent to which employers pass on the burden to lower wages. Using the CGT reform as an example demonstrates the importance of these behavioural responses. PolicyEngine's flexibility allows users to adjust behavioural response assumptions such as labour elasticities and capital gains elasticity to analyse the impact of public policies.

+While this report focuses on these three core elasticities, PolicyEngine is expanding its behavioural modelling capabilities. For instance, we developed responses to [employer National Insurance contributions](https://legacy.policyengine.org/uk/research/autumn-budget-24-employer-ni), indicating the extent to which employers pass on the burden to lower wages. Using the CGT reform as an example demonstrates the importance of these behavioural responses. PolicyEngine's flexibility allows users to adjust behavioural response assumptions such as labour elasticities and capital gains elasticity to analyse the impact of public policies.

[^1]: Chetty, R., Guren, A., Manoli, D., & Weber, A. (2011). Are Micro and Macro Labor Supply Elasticities Consistent? A Review of Evidence on the Intensive and Extensive Margins. American Economic Review, 101(3), 471–475.

diff --git a/src/posts/articles/biden-budget-2025.md b/src/posts/articles/biden-budget-2025.md

index ad247ec29..4951c8a6b 100644

--- a/src/posts/articles/biden-budget-2025.md

+++ b/src/posts/articles/biden-budget-2025.md

@@ -10,7 +10,7 @@ President Biden introduced his [2025 Budget](https://www.whitehouse.gov/briefing

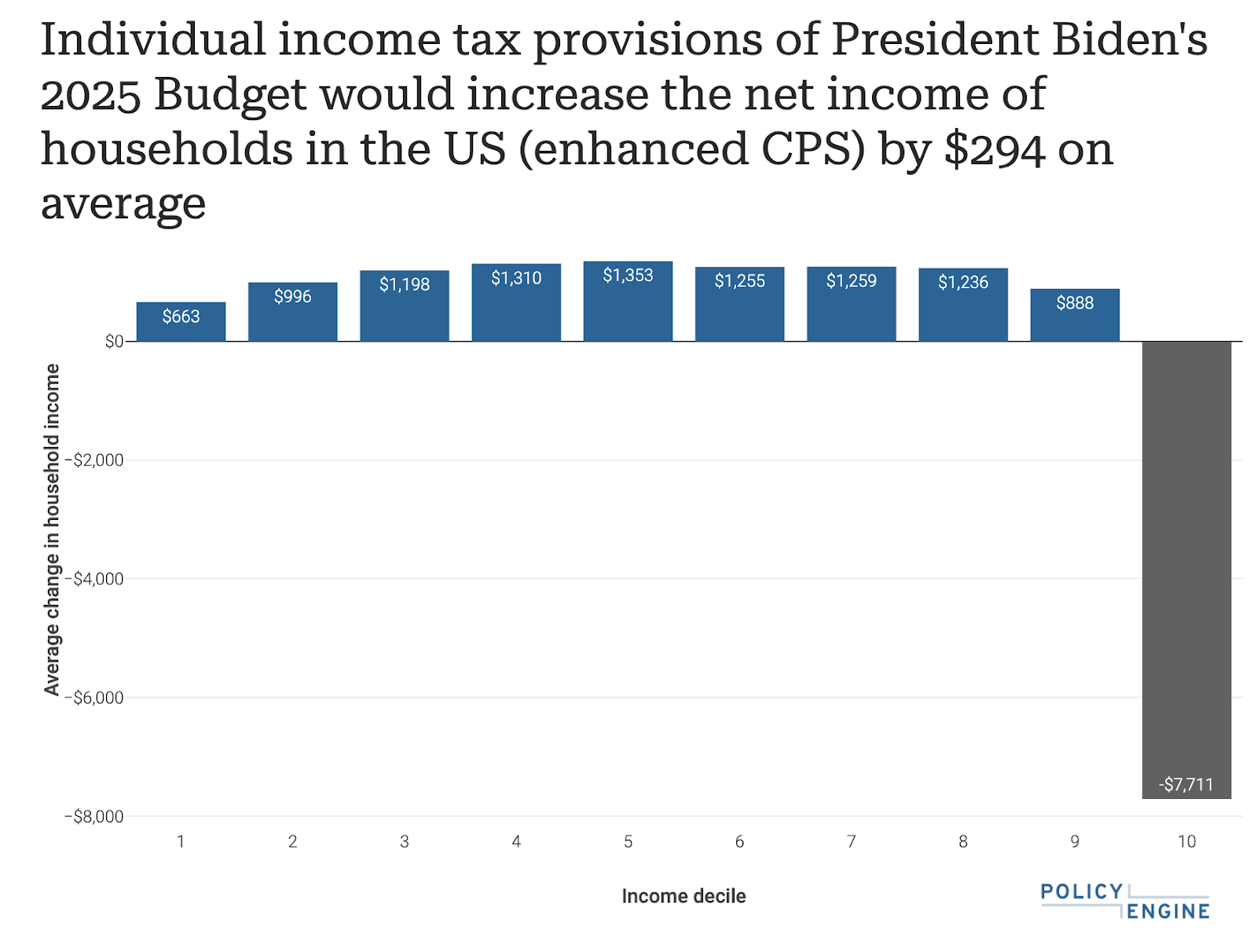

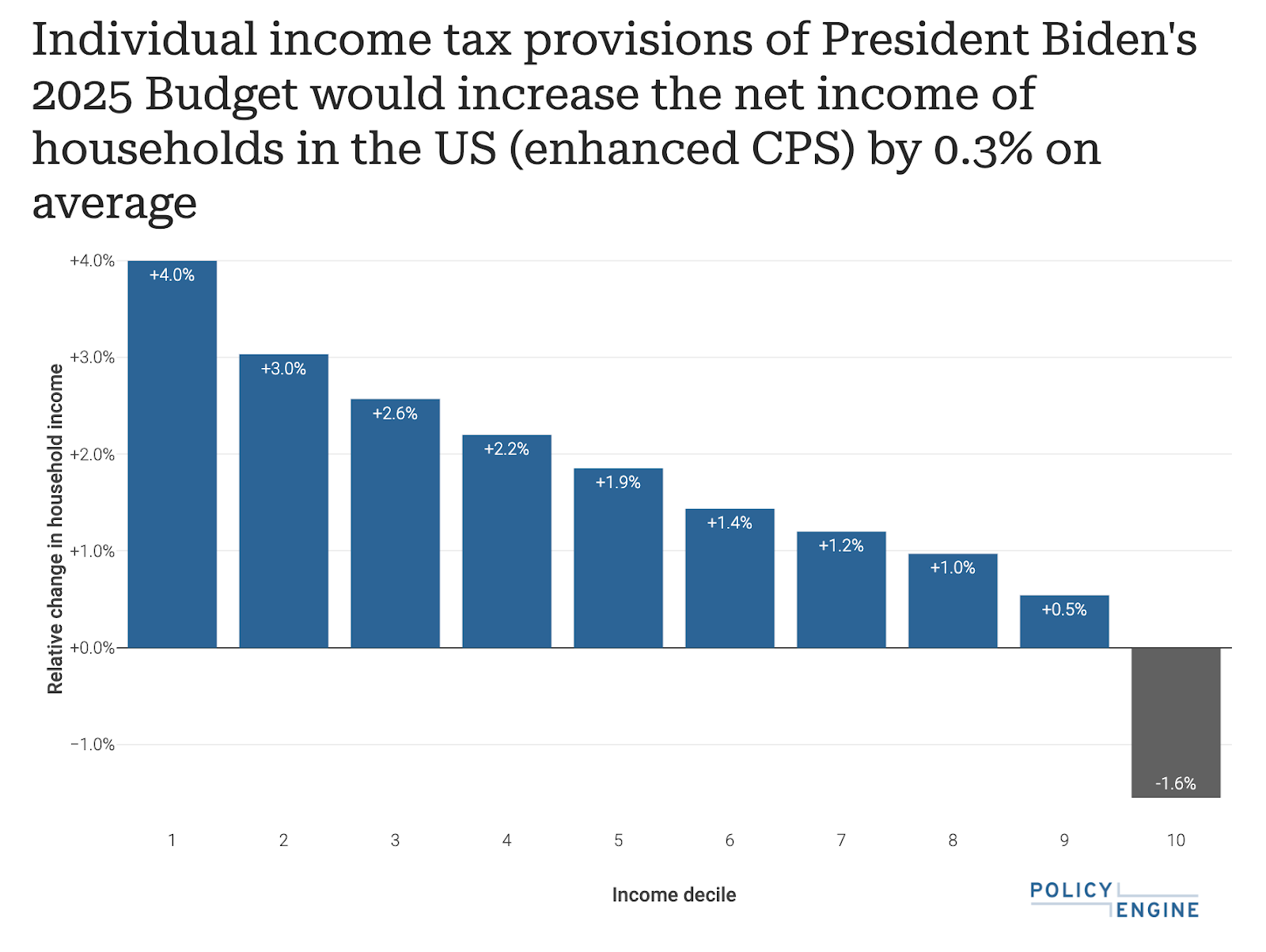

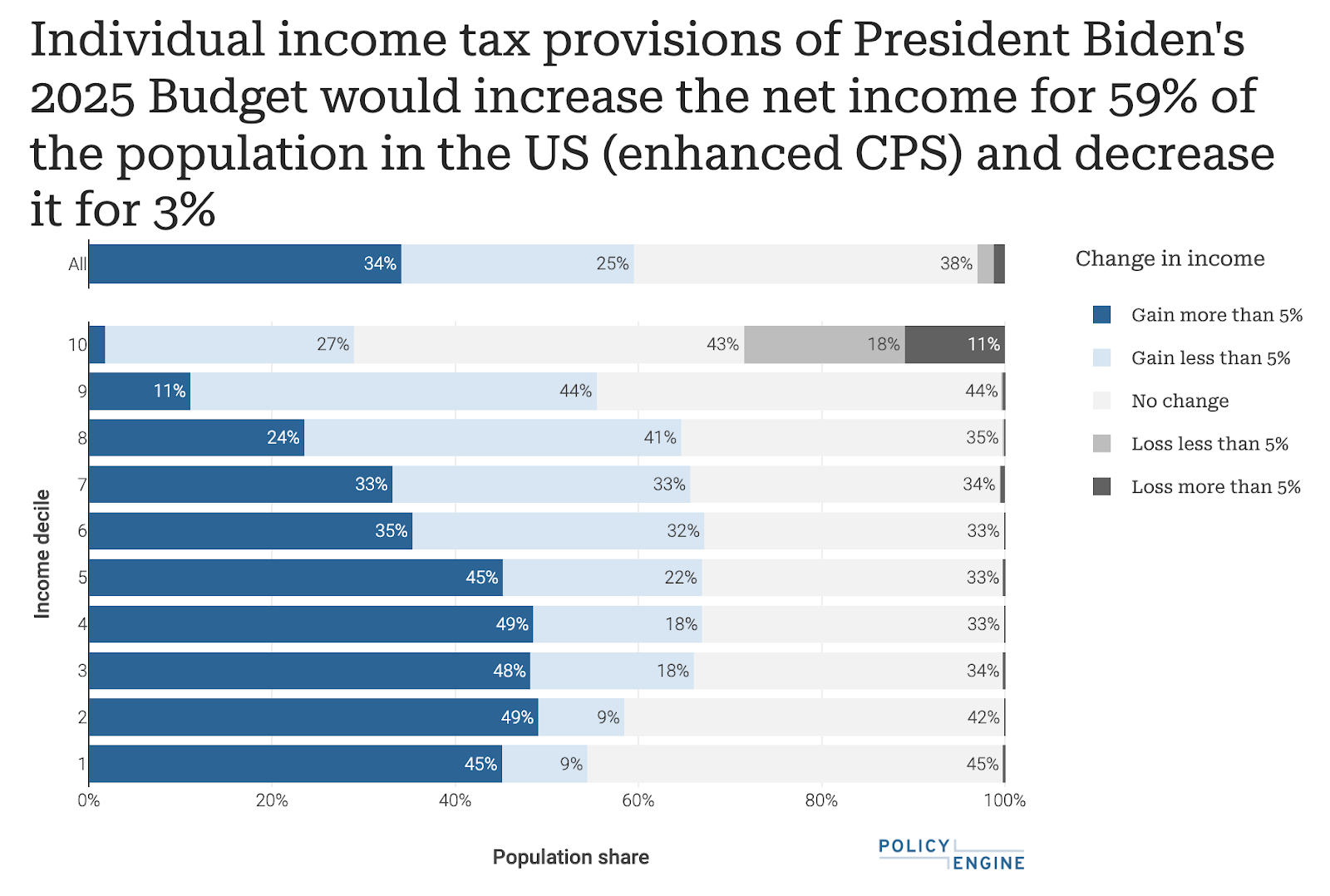

We estimate that, in 2024 and assuming no behavioral responses, these reforms would cost $40.5 billion, lower poverty 12%, and lower income inequality. 59% of Americans would see a higher net income, while 3% would see a lower net income. This report describes these impacts in more detail, and examines effects on individual households.

-**See how President Biden’s 2025 Budget affects your household with our [personalized calculator.](https://policyengine.org/us/household?reform=50893&focus=intro®ion=enhanced_us&timePeriod=2024&baseline=2)**

+**See how President Biden’s 2025 Budget affects your household with our [personalized calculator.](https://legacy.policyengine.org/us/household?reform=50893&focus=intro®ion=enhanced_us&timePeriod=2024&baseline=2)**

## The reforms

@@ -20,11 +20,11 @@ Here we summarize the four provisions of Biden’s 2025 Budget that PolicyEngine

Biden’s budget restores the expansion to the Child Tax Credit (CTC) enacted in the American Rescue Plan Act (ARPA). It would make the CTC fully refundable beginning in 2024, and for 2024 and 2025 increase the age limit from 16 to 17. Additionally, it increases the maximum credit per child to $3,600 for children under 6, and $3,000 for older children, phasing out at 5% of income in excess of a threshold dependent on filing status: $150,000 (married joint), $112,500 (head of household), and $75,000 (other). These amounts are not inflation-adjusted.

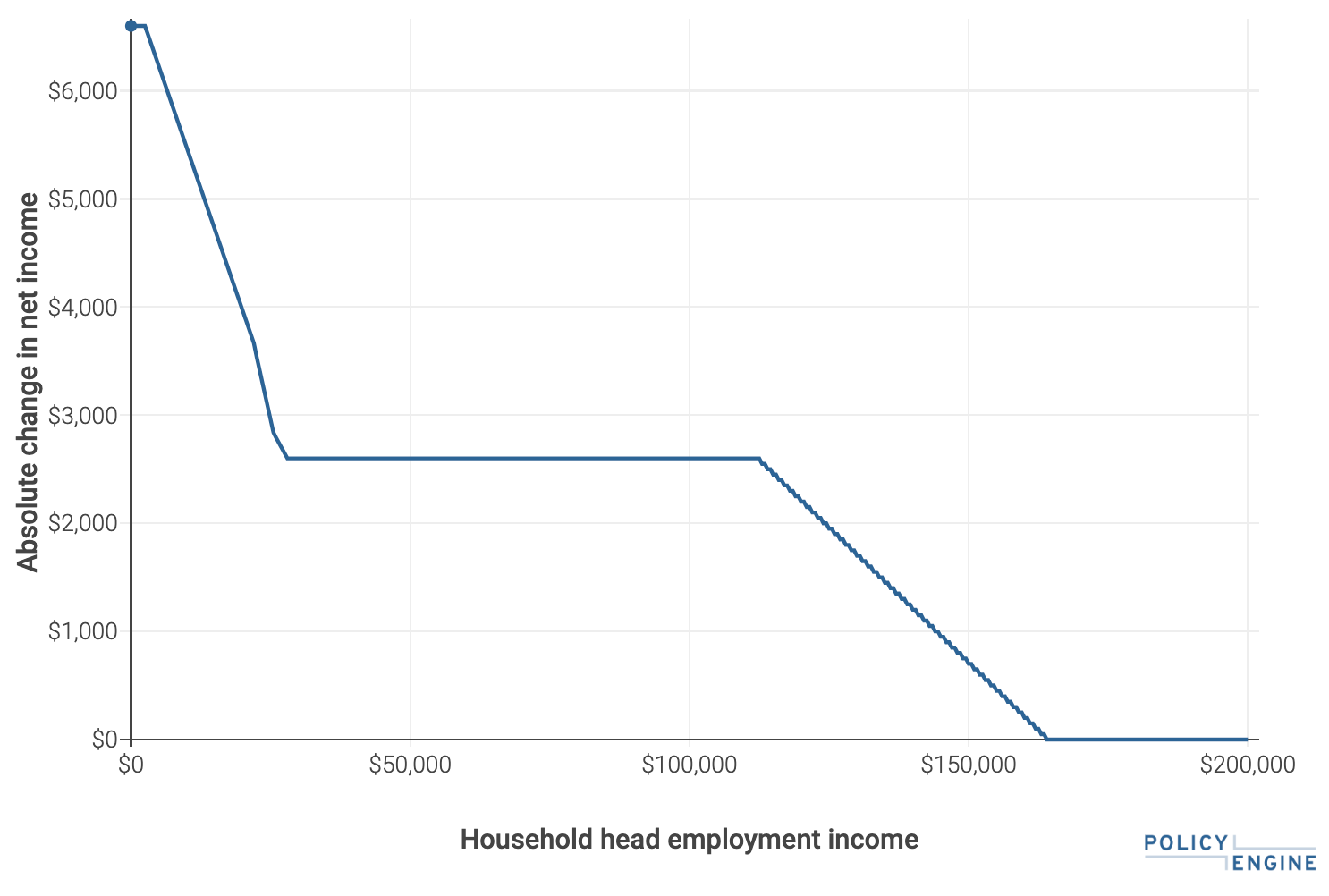

-For example, this reform would provide an additional $3,600 to a single parent of two children, with one below six, if their income is below $6,600. The net benefit would phase out until their earnings reach $164,000, as shown [here](https://policyengine.org/us/household?focus=householdOutput.earnings&reform=3826®ion=us&timePeriod=2024&baseline=2&household=43046).

+For example, this reform would provide an additional $3,600 to a single parent of two children, with one below six, if their income is below $6,600. The net benefit would phase out until their earnings reach $164,000, as shown [here](https://legacy.policyengine.org/us/household?focus=householdOutput.earnings&reform=3826®ion=us&timePeriod=2024&baseline=2&household=43046).

-To learn more, read our [**2023 report on restoring the ARPA CTC.**](https://policyengine.org/us/research/restoration-of-the-american-rescue-plan-acts-expanded-child-tax-credit)

+To learn more, read our [**2023 report on restoring the ARPA CTC.**](https://legacy.policyengine.org/us/research/restoration-of-the-american-rescue-plan-acts-expanded-child-tax-credit)

### Restoring the 2021 Earned Income Tax Credit expansion for filers without qualifying children

@@ -38,7 +38,7 @@ Biden similarly proposed restoring ARPA’s expansion of the Earned Income Tax C

- Raise the maximum credit from $632 to $1,749 (adjusted for inflation from 2021)

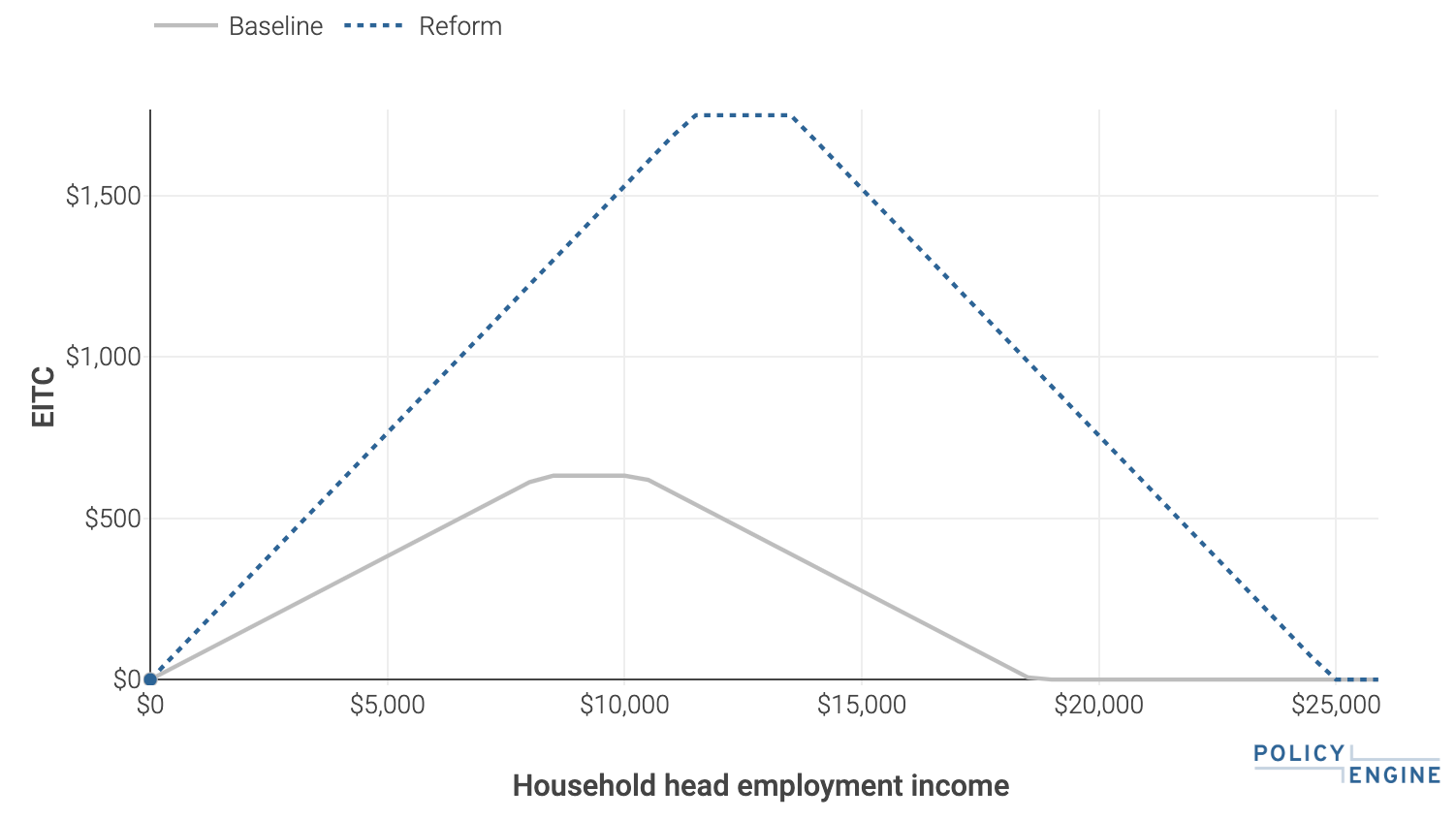

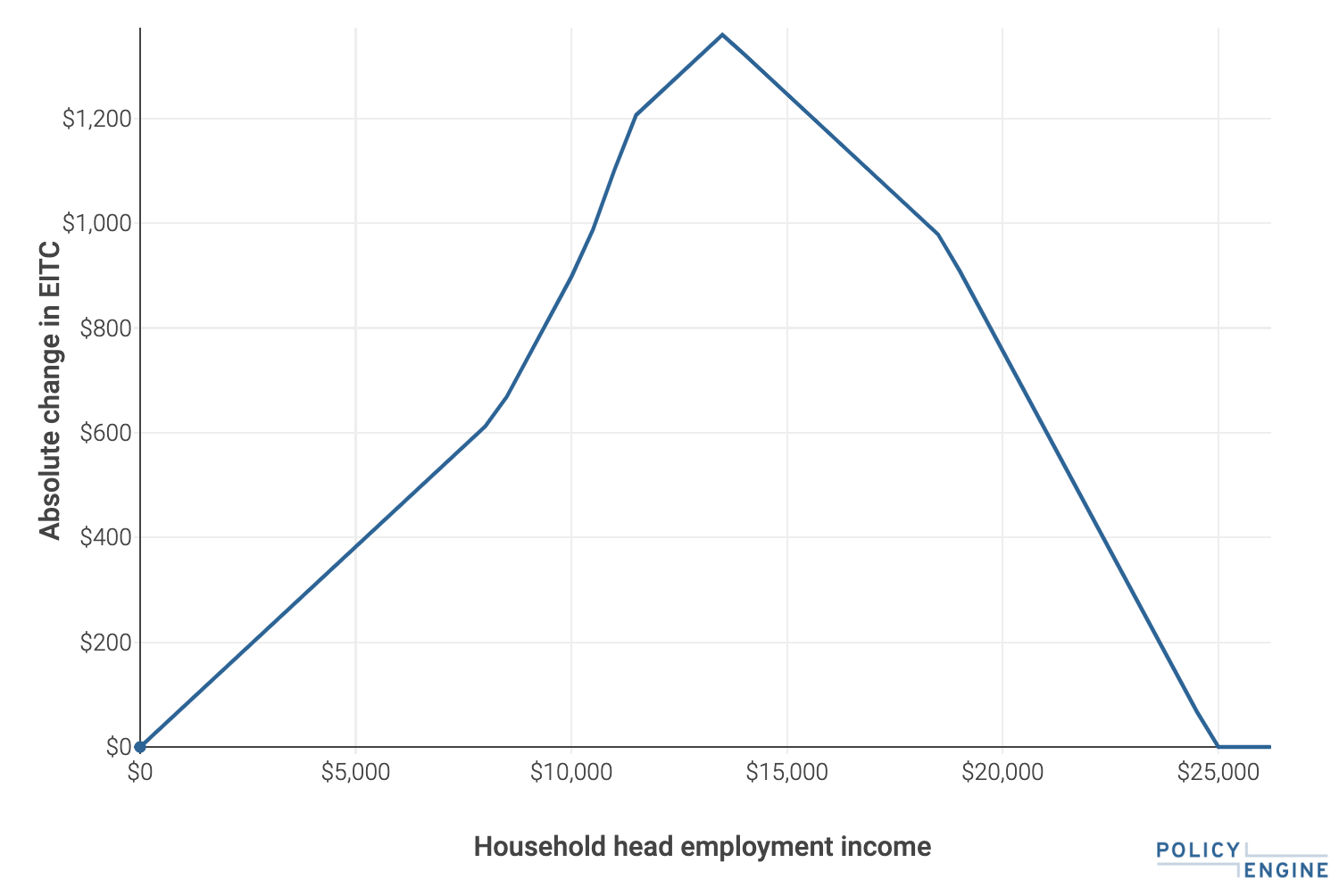

-This would change the EITC [as follows](https://policyengine.org/us/household?reform=50974&focus=householdOutput.earnings®ion=enhanced_us&timePeriod=2024&baseline=2&household=40437) for a single person between 25 and 65:

+This would change the EITC [as follows](https://legacy.policyengine.org/us/household?reform=50974&focus=householdOutput.earnings®ion=enhanced_us&timePeriod=2024&baseline=2&household=40437) for a single person between 25 and 65:

@@ -46,19 +46,19 @@ Producing a net benefit of up to $1,360 at $13,500 earnings, phasing out until e

-To learn more, read our [2023 report on restoring the ARPA EITC.](https://policyengine.org/us/research/restoring-arpa-eitc)

+To learn more, read our [2023 report on restoring the ARPA EITC.](https://legacy.policyengine.org/us/research/restoring-arpa-eitc)

### Increasing the top marginal rate to 39.6%

The President proposed raising the top marginal tax rate from 37% to 39.6%, its value prior to the Tax Cuts and Jobs Act of 2017. The new rate would apply to income above $400,000 for single filers, $425,000 for head of household filers, $450,000 for married filers, and $225,000 for married separate filers. The reform would take effect in 2024, and the thresholds would rise with inflation starting in 2025.

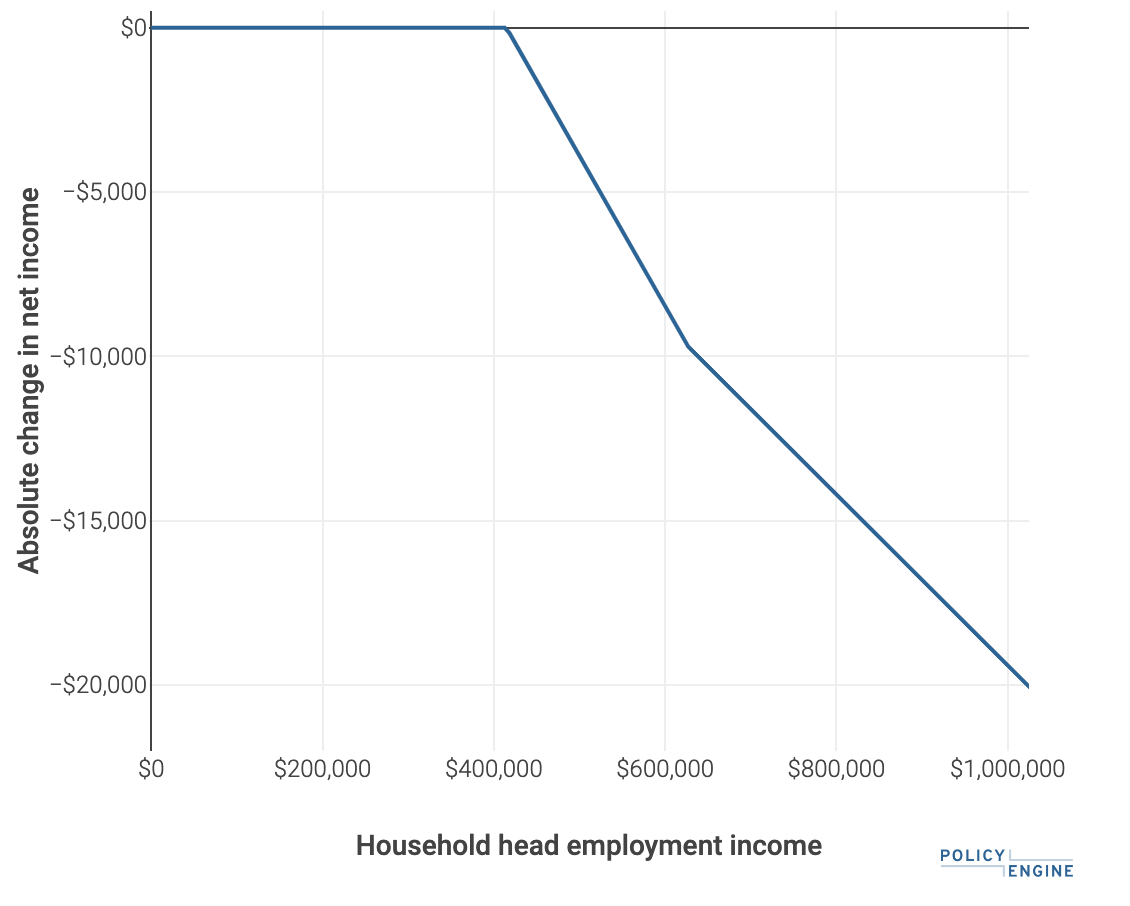

-For a [single person](https://policyengine.org/us/household?reform=50882&focus=householdOutput.earnings®ion=enhanced_us&timePeriod=2024&baseline=2&household=43050) without itemized deductions, taxes would begin rising at $414,600 ($400,000 plus the standard deduction), and reach $19,400 in additional taxes at $1 million earnings.

+For a [single person](https://legacy.policyengine.org/us/household?reform=50882&focus=householdOutput.earnings®ion=enhanced_us&timePeriod=2024&baseline=2&household=43050) without itemized deductions, taxes would begin rising at $414,600 ($400,000 plus the standard deduction), and reach $19,400 in additional taxes at $1 million earnings.

### Increasing the Medicare and Net Investment Income taxes

-Finally, the President proposed increasing both the top Medicare tax rate and top Net Investment Income Tax (NIIT) rate by 1.2 percentage points for individuals with income over $400,000. Since this is based on wages or net investment income, it kicks in at $400,000, not the higher amount resulting from the standard deduction. For an [individual](https://policyengine.org/us/household?reform=50660&focus=householdOutput.earnings®ion=enhanced_us&timePeriod=2024&baseline=2&household=43051) with $1 million in wages, it would increase their taxes by $7,200.

+Finally, the President proposed increasing both the top Medicare tax rate and top Net Investment Income Tax (NIIT) rate by 1.2 percentage points for individuals with income over $400,000. Since this is based on wages or net investment income, it kicks in at $400,000, not the higher amount resulting from the standard deduction. For an [individual](https://legacy.policyengine.org/us/household?reform=50660&focus=householdOutput.earnings®ion=enhanced_us&timePeriod=2024&baseline=2&household=43051) with $1 million in wages, it would increase their taxes by $7,200.

@@ -82,21 +82,21 @@ To see the combined impacts of all four reforms on net income and work incentive

### Single person

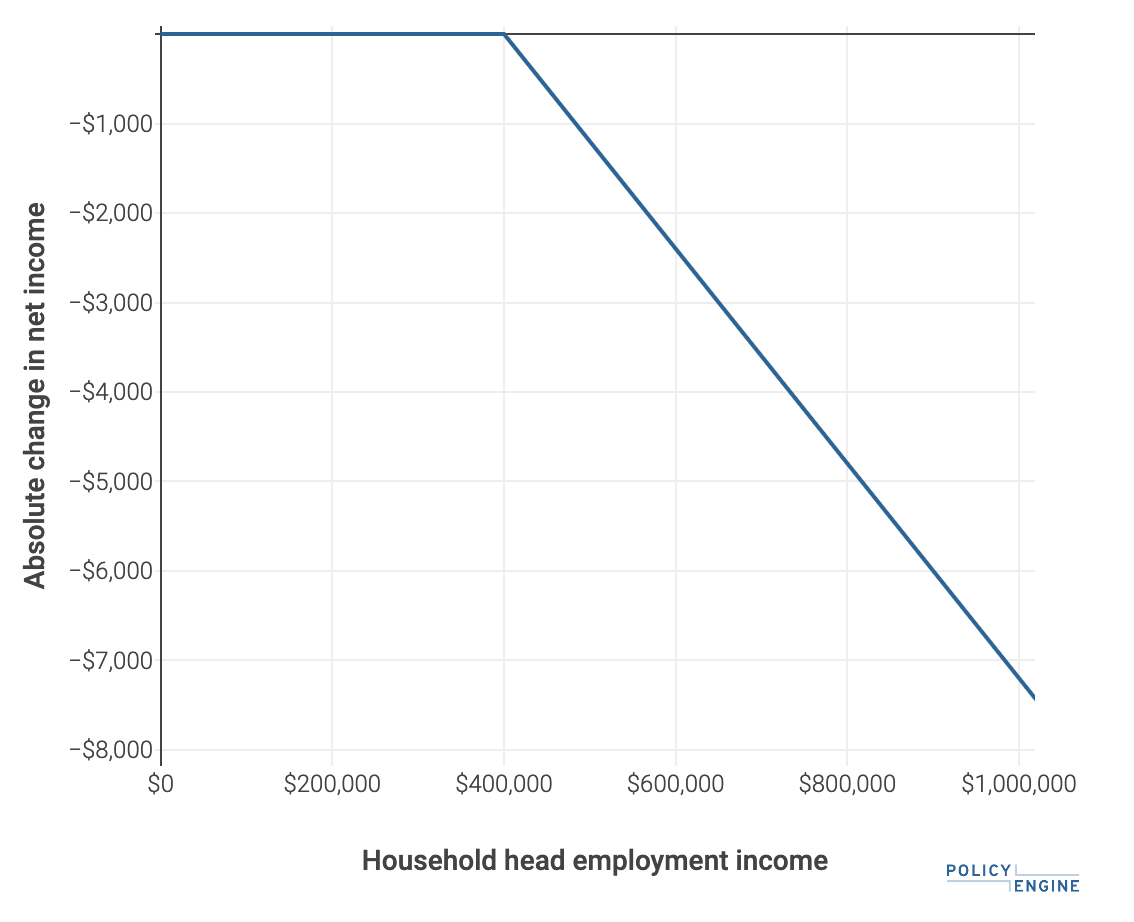

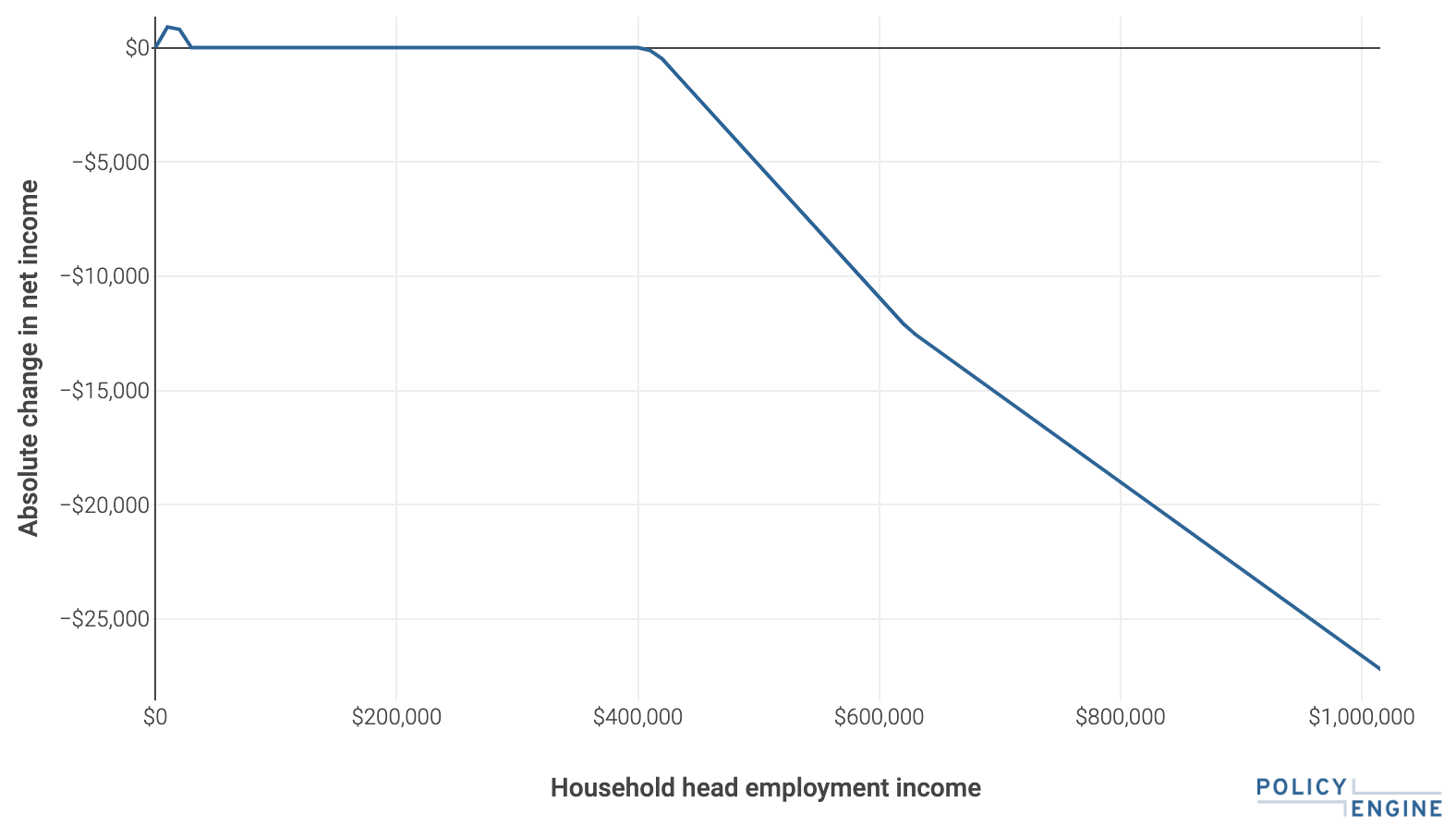

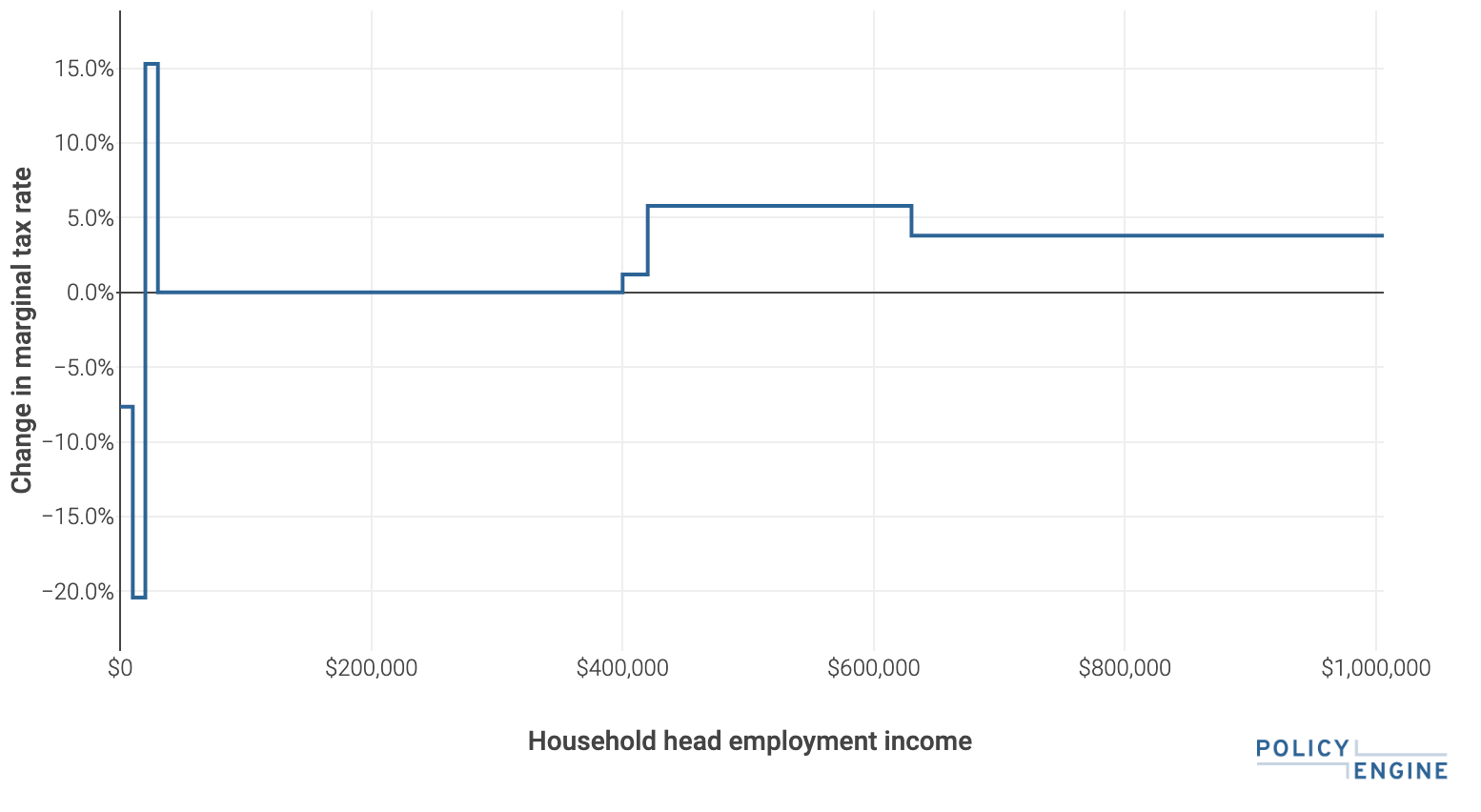

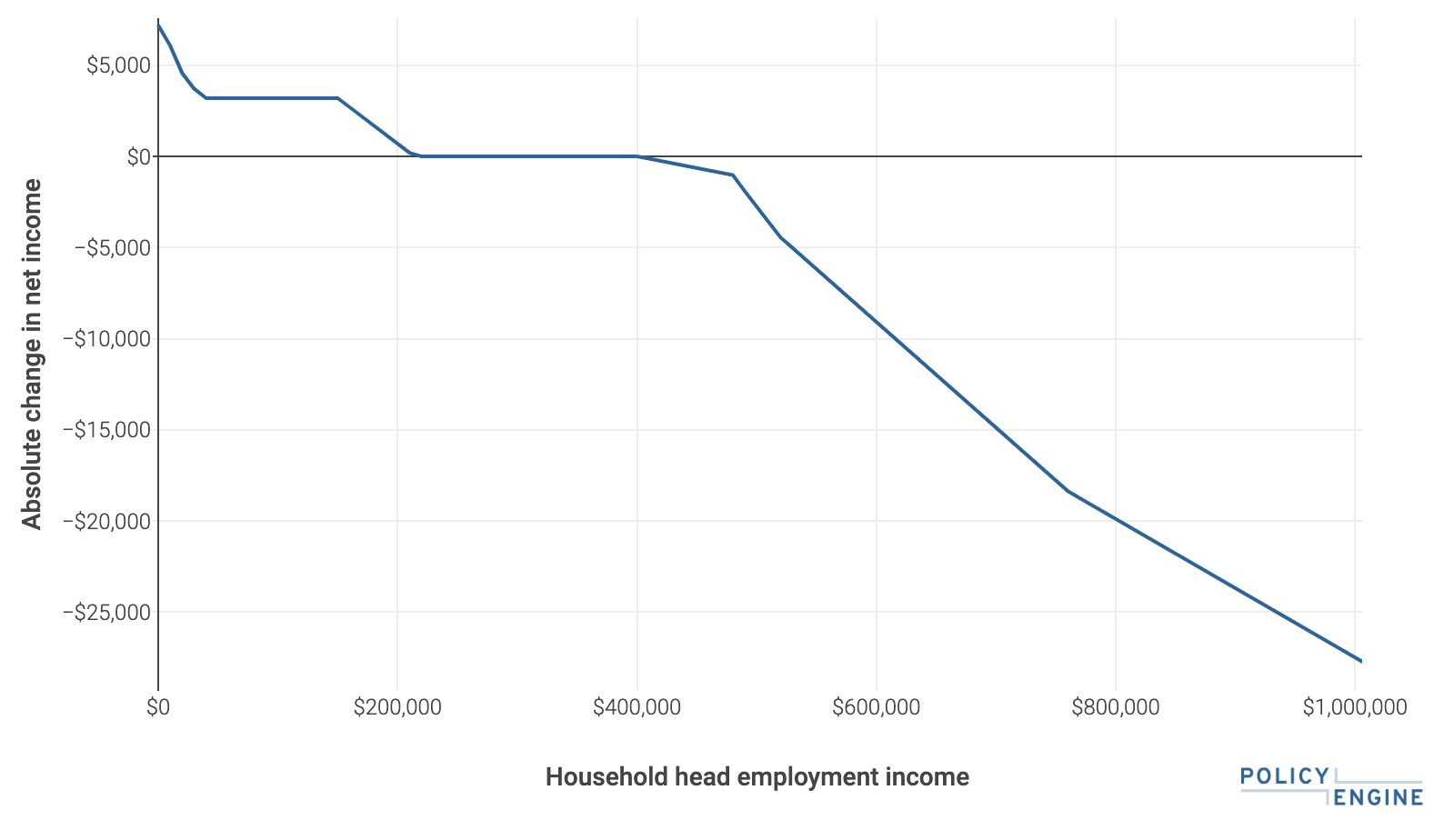

-The [single person](https://policyengine.org/us/household?reform=51189&focus=householdOutput.earnings®ion=enhanced_us&timePeriod=2024&baseline=2&household=43051) would see a larger EITC at low incomes, then a tax increase when their wages exceed $400,000, reaching a $26,600 total impact at $1 million earnings.

+The [single person](https://legacy.policyengine.org/us/household?reform=51189&focus=householdOutput.earnings®ion=enhanced_us&timePeriod=2024&baseline=2&household=43051) would see a larger EITC at low incomes, then a tax increase when their wages exceed $400,000, reaching a $26,600 total impact at $1 million earnings.