diff --git a/demo-FSI/lakehouse-fsi-credit-decisioning/03-Data-Science-ML/03.1-Exploratory-Analysis-credit-decisioning.py b/demo-FSI/lakehouse-fsi-credit-decisioning/03-Data-Science-ML/03.1-Exploratory-Analysis-credit-decisioning.py

new file mode 100644

index 00000000..e6b0c6c7

--- /dev/null

+++ b/demo-FSI/lakehouse-fsi-credit-decisioning/03-Data-Science-ML/03.1-Exploratory-Analysis-credit-decisioning.py

@@ -0,0 +1,107 @@

+# Databricks notebook source

+# MAGIC %md

+# MAGIC # Exploratory Analysis

+

+# COMMAND ----------

+

+# MAGIC %md

+# MAGIC

+# MAGIC Data exploration is a critical first step in building a Responsible AI solution, as it helps ensure transparency, fairness, and reliability from the outset. In this notebook, we will explore and analyze our dataset on the Databricks Data Intelligence Platform. This process lays the foundation for responsible feature engineering and model development. Human validation remains an essential part of this step, ensuring that data-driven insights align with domain knowledge and ethical considerations.

+# MAGIC

+# MAGIC By leveraging Databricks’ unified data and AI capabilities, we can conduct secure and scalable exploratory data analysis (EDA), assess data distributions, and validate class representation before moving forward with model development.

+# MAGIC

+# MAGIC

+

+# COMMAND ----------

+

+# MAGIC %run ../_resources/00-setup $reset_all_data=false

+

+# COMMAND ----------

+

+# MAGIC %md

+# MAGIC ## Security and Table Access Controls

+# MAGIC

+# MAGIC Before proceeding with data exploration, it is crucial to implement security and access controls to ensure data integrity and compliance. Proper security measures help:

+# MAGIC

+# MAGIC - Protect sensitive financial and customer data, preventing unauthorized access and ensuring regulatory adherence.

+# MAGIC - Ensure data consistency, so analysts work with validated and high-quality data without discrepancies.

+# MAGIC - Avoid data leakage risks, preventing the unintentional exposure of confidential information that could lead to compliance violations.

+# MAGIC - Facilitate accountability, ensuring that any modifications or transformations are logged and traceable.

+# MAGIC

+# MAGIC By establishing a secure data foundation, we ensure that subsequent analysis and modeling steps are performed responsibly, with complete confidence in data integrity and compliance.

+# MAGIC

+# MAGIC Table Access Control (TAC) in Databricks lets administrators manage access to specific tables and columns, controlling permissions like read, write, or modify. Integrated with Unity Catalog, it allows fine-grained security to protect sensitive data and ensure only authorized users have access. This feature enhances data governance, compliance, and secure collaboration across the platform.

+# MAGIC

+# MAGIC Now, let's grant only a ```SELECT``` access to ```customer_gold``` table to everyone in the group ```Data Scientist```.

+

+# COMMAND ----------

+

+# MAGIC %sql

+# MAGIC

+# MAGIC GRANT SELECT ON TABLE customer_gold TO `Data Scientist`

+

+# COMMAND ----------

+

+# MAGIC %md-sandbox

+# MAGIC

+# MAGIC ## Exploratory Data Analysis

+# MAGIC

+# MAGIC The first step as Data Scientist is to explore and understand the data. [Databricks Notebooks](https://docs.databricks.com/en/notebooks/index.html) offer native data quality profiling and dashboarding capabilities that allow users to easily assess and visualize the quality of their data. Built-in tools allows us to:

+# MAGIC - Identify missing values and potential data quality issues.

+# MAGIC - Detect outliers and anomalies that may skew model predictions.

+# MAGIC - Assess statistical distributions of key features to uncover potential biases.

+# MAGIC

+# MAGIC Databricks enables scalable EDA through interactive notebooks, where we can visualize distributions, perform statistical tests, and generate summary reports seamlessly.

+

+# COMMAND ----------

+

+# DBTITLE 1,Use SQL to explore your data

+# MAGIC %sql

+# MAGIC SELECT * FROM customer_gold

+

+# COMMAND ----------

+

+# MAGIC %md

+# MAGIC While Databricks provides built-in data profiling tools, additional Python libraries such as Plotly and Seaborn can be used to enhance analysis. These libraries allow for more interactive and customizable visualizations, helping uncover hidden patterns in the data.

+# MAGIC

+# MAGIC Using these additional libraries in combination with Databricks' built-in capabilities ensures a more comprehensive data exploration process, leading to better insights for responsible model development.

+

+# COMMAND ----------

+

+# DBTITLE 1,Use any of your usual python libraries for analysis

+data = spark.table("customer_gold") \

+ .where("tenure_months BETWEEN 10 AND 150") \

+ .groupBy("tenure_months", "education").sum("income_monthly") \

+ .orderBy('education').toPandas()

+

+px.bar(data, x="tenure_months", y="sum(income_monthly)", color="education", title="Total Monthly Income")

+

+# COMMAND ----------

+

+# MAGIC %md

+# MAGIC

+# MAGIC ## Class representation

+# MAGIC

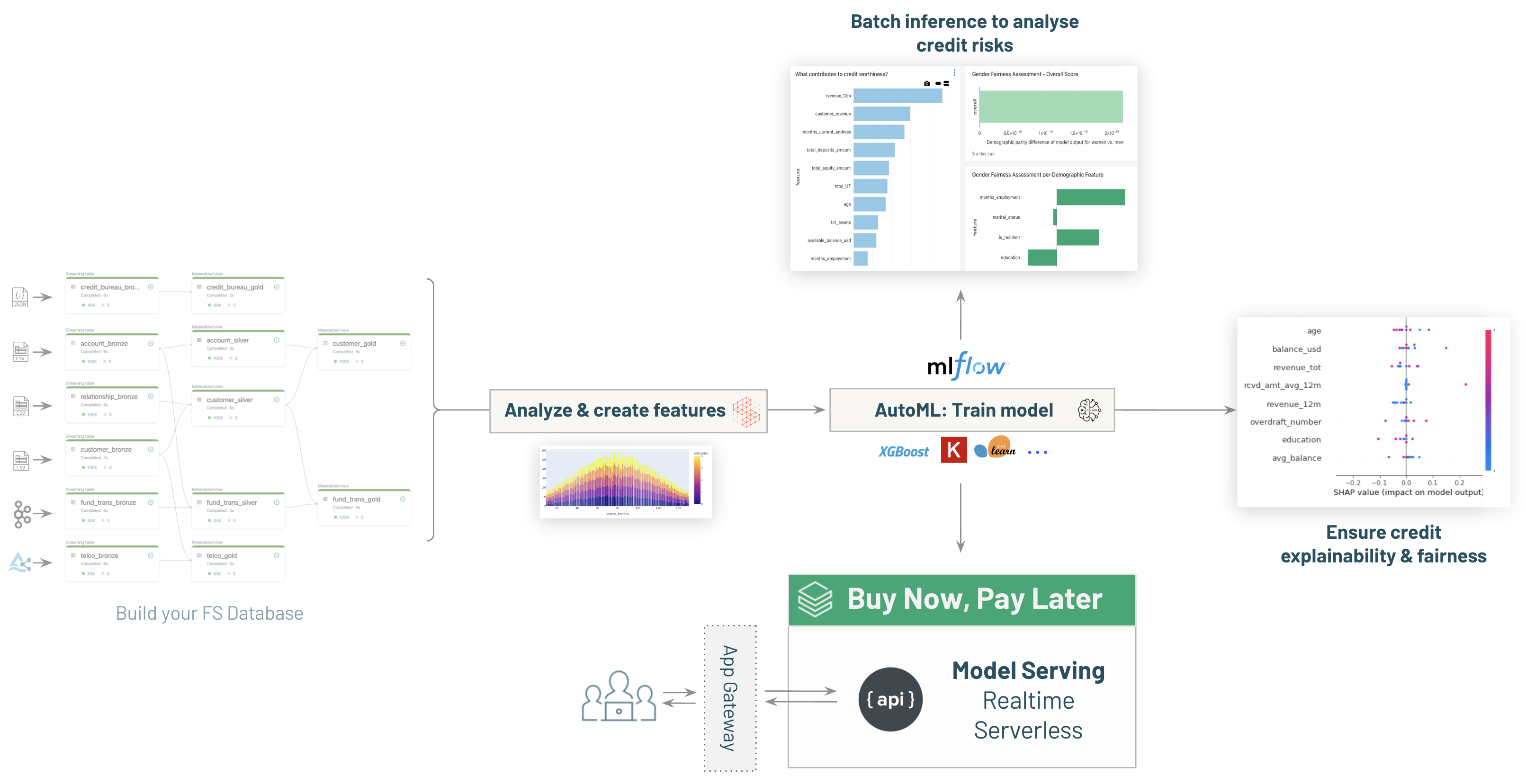

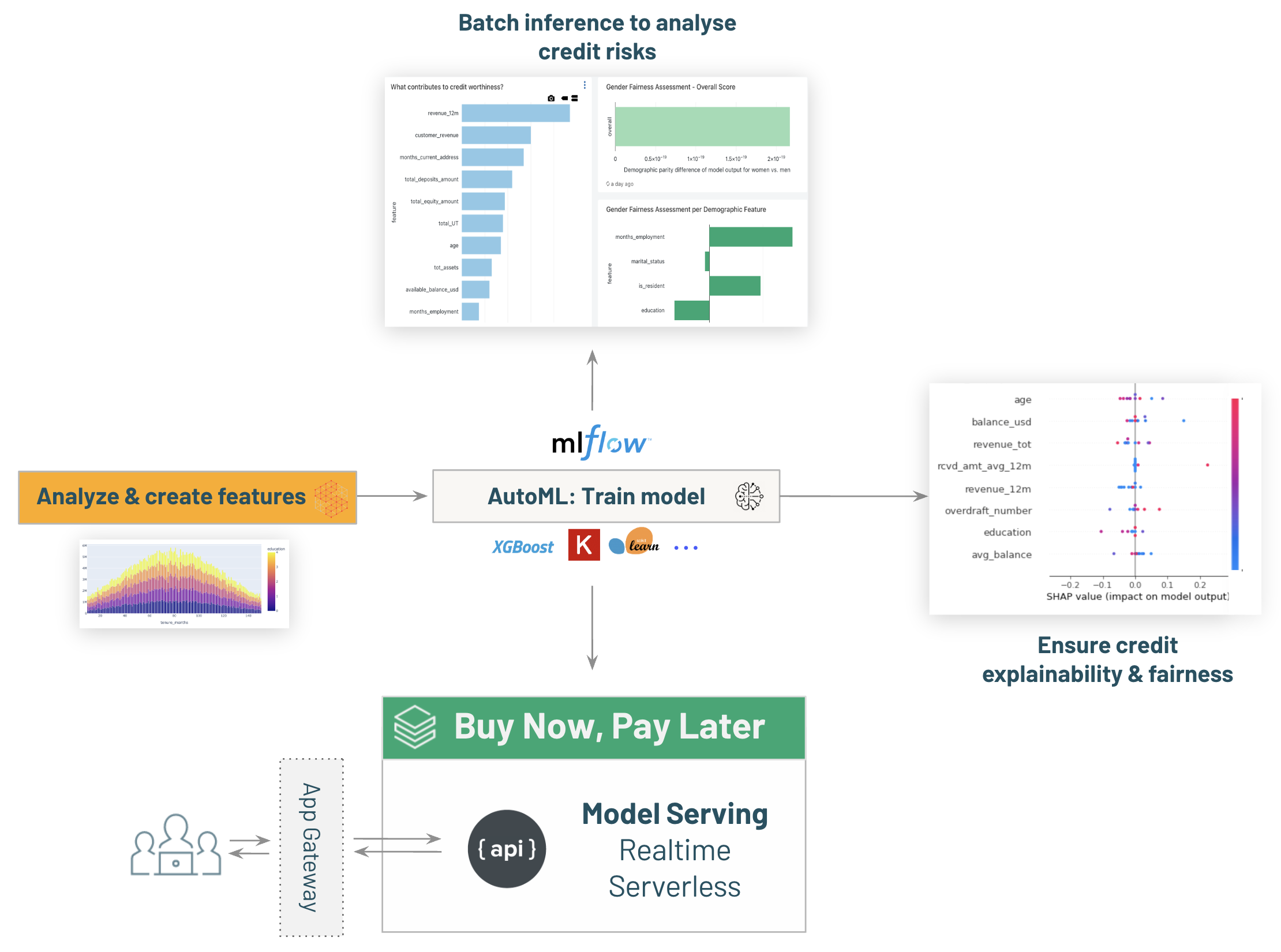

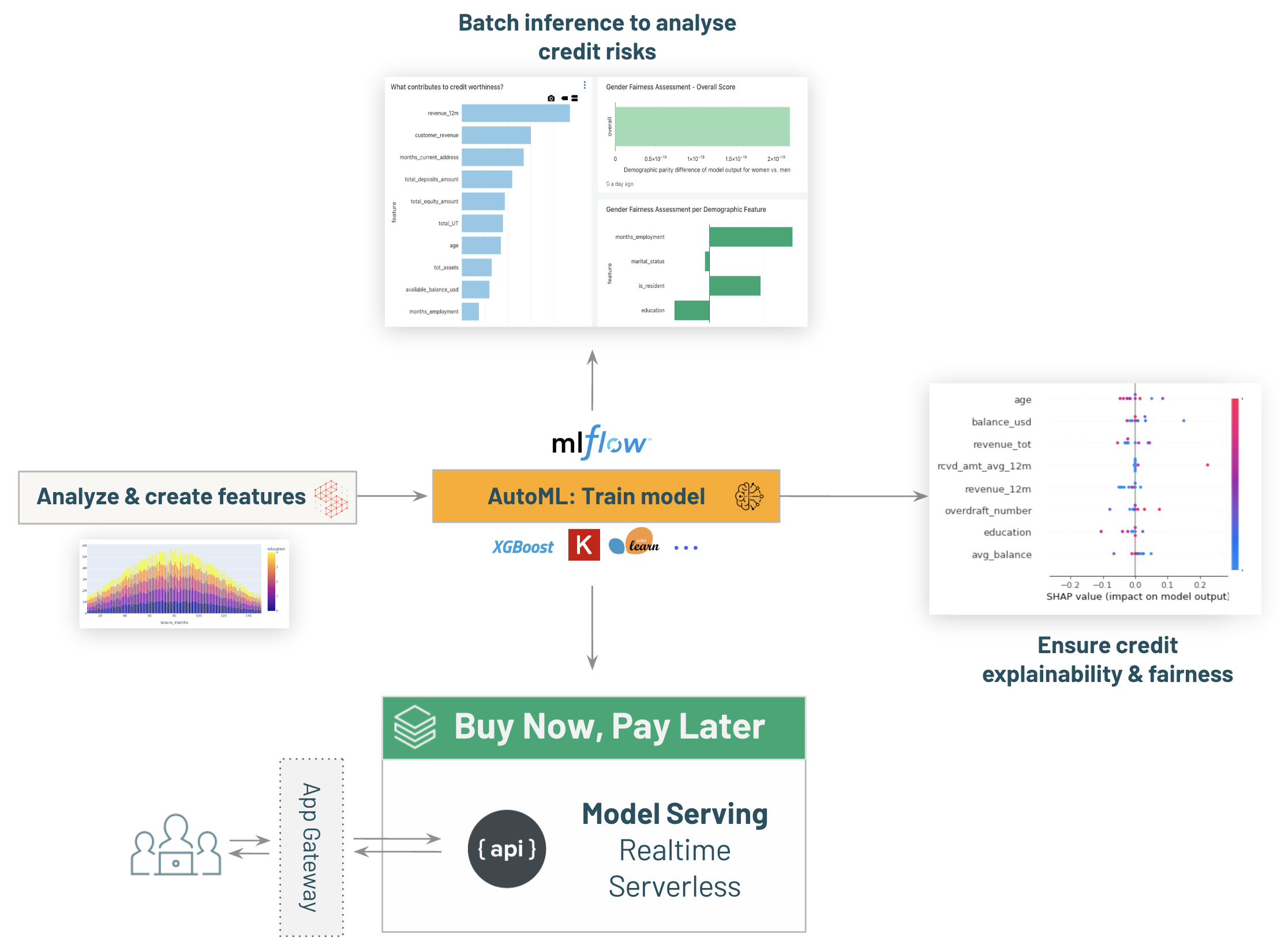

+# MAGIC Understanding class representation during exploratory data analysis is crucial for identifying potential bias in data. Imbalanced classes can lead to biased models, where underrepresented classes are poorly learned, resulting in inaccurate predictions. If certain groups are over- or underrepresented, the model may inherit societal biases, leading to unfair outcomes. Identifying skewed distributions helps in selecting appropriate resampling techniques or adjusting model evaluation metrics. Moreover, biased training data can reinforce discrimination in applications like credit decisioning. Detecting imbalance early allows for corrective actions, ensuring a more robust, fair, and generalizable model that performs well across all classes.

+

+# COMMAND ----------

+

+data = spark.table("customer_gold") \

+ .groupBy("gender").count() \

+ .orderBy('gender').toPandas()

+

+px.pie(data_frame=data, names="gender", values="count", color="gender", title="Percentage of Males vs. Females")

+

+# COMMAND ----------

+

+# MAGIC %md

+# MAGIC

+# MAGIC ## Next Steps

+# MAGIC

+# MAGIC After completing exploratory analysis, we proceed to [06.2-Feature-Updates]($./06-Responsible-AI/06.2-Feature-Updates), where we:

+# MAGIC - Continuously ingest new data to keep features relevant and up to date.

+# MAGIC - Apply responsible transformations while maintaining full lineage and compliance.

+# MAGIC - Log feature changes to ensure transparency in model evolution.

+# MAGIC

+# MAGIC By systematically updating features, we reinforce responsible AI practices and enhance our credit scoring model’s fairness, reliability, and effectiveness.

diff --git a/demo-FSI/lakehouse-fsi-credit-decisioning/03-Data-Science-ML/03.1-Feature-Engineering-credit-decisioning.py b/demo-FSI/lakehouse-fsi-credit-decisioning/03-Data-Science-ML/03.1-Feature-Engineering-credit-decisioning.py

deleted file mode 100644

index d267e52e..00000000

--- a/demo-FSI/lakehouse-fsi-credit-decisioning/03-Data-Science-ML/03.1-Feature-Engineering-credit-decisioning.py

+++ /dev/null

@@ -1,180 +0,0 @@

-# Databricks notebook source

-# MAGIC %md

-# MAGIC

-# MAGIC # ML: predict credit owners with high default probability

-# MAGIC

-# MAGIC Once all data is loaded and secured (the **data unification** part), we can proceed to exploring, understanding, and using the data to create actionable insights - **data decisioning**.

-# MAGIC

-# MAGIC

-# MAGIC As outlined in the [introductory notebook]($../00-Credit-Decisioning), we will build machine learning (ML) models for driving three business outcomes:

-# MAGIC 1. Identify currently underbanked customers with high credit worthiness so we can offer them credit instruments,

-# MAGIC 2. Predict current credit owners with high probability of defaulting along with the loss-given default, and

-# MAGIC 3. Offer instantaneous micro-loans (Buy Now, Pay Later) when a customer does not have the required credit limit or account balance to complete a transaction.

-# MAGIC

-# MAGIC Here is the flow we'll implement:

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC

-

-# COMMAND ----------

-

-# MAGIC %md

-# MAGIC

-# MAGIC ## The need for Enhanced Collaboration

-# MAGIC

-# MAGIC Feature Engineering is an iterative process - we need to quickly generate new features, test the model, and go back to feature selection and more feature engineering - many many times. The Databricks Lakehouse enables data teams to collaborate extremely effectively through the following Databricks Notebook features:

-# MAGIC 1. Sharing and collaborating in the same Notebook by any team member (with different access modes),

-# MAGIC 2. Ability to use python, SQL, and R simultaneously in the same Notebook on the same data,

-# MAGIC 3. Native integration with a Git repository (including AWS Code Commit, Azure DevOps, GitLabs, Github, and others), making the Notebooks tools for CI/CD,

-# MAGIC 4. Variables explorer,

-# MAGIC 5. Automatic Data Profiling (in the cell below), and

-# MAGIC 6. GUI-based dashboards (in the cell below) that can also be added to any Databricks SQL Dashboard.

-# MAGIC

-# MAGIC These features enable teams within FSI organizations to become extremely fast and efficient in building the best ML model at reduced time, thereby making the most out of market opportunities such as the raising interest rates.

-

-# COMMAND ----------

-

-# MAGIC %pip install databricks-sdk==0.36.0 mlflow==2.19.0 databricks-feature-store==0.17.0

-# MAGIC dbutils.library.restartPython()

-

-# COMMAND ----------

-

-# MAGIC %run ../_resources/00-setup $reset_all_data=false

-

-# COMMAND ----------

-

-# MAGIC %md-sandbox

-# MAGIC

-# MAGIC ## Data exploration & Features creation

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC The first step as Data Scientist is to explore our data and understand it to create Features.

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC This where we use our existing tables and transform the data to be ready for our ML models. These features will later be stored in Databricks Feature Store (see below) and used to train the aforementioned ML models.

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC Let's start with some data exploration. Databricks comes with built-in Data Profiling to help you bootstrap that.

-

-# COMMAND ----------

-

-# DBTITLE 1,Use SQL to explore your data

-# MAGIC %sql

-# MAGIC SELECT * FROM customer_gold WHERE tenure_months BETWEEN 10 AND 150

-

-# COMMAND ----------

-

-# DBTITLE 1,Our any of your usual python libraries for analysis

-data = spark.table("customer_gold") \

- .where("tenure_months BETWEEN 10 AND 150") \

- .groupBy("tenure_months", "education").sum("income_monthly") \

- .orderBy('education').toPandas()

-

-px.bar(data, x="tenure_months", y="sum(income_monthly)", color="education", title="Wide-Form Input")

-

-# COMMAND ----------

-

-# MAGIC %md

-# MAGIC

-# MAGIC # Building our Features for Credit Default risks

-# MAGIC

-# MAGIC To build our model predicting credit default risks, we'll need a buch of features. To improve our governance and centralize our data for multiple ML project, we can save our ML features using a Feature Store.

-

-# COMMAND ----------

-

-# DBTITLE 1,Read the customer table

-customer_gold_features = (spark.table("customer_gold")

- .withColumn('age', int(date.today().year) - col('birth_year'))

- .select('cust_id', 'education', 'marital_status', 'months_current_address', 'months_employment', 'is_resident',

- 'tenure_months', 'product_cnt', 'tot_rel_bal', 'revenue_tot', 'revenue_12m', 'income_annual', 'tot_assets',

- 'overdraft_balance_amount', 'overdraft_number', 'total_deposits_number', 'total_deposits_amount', 'total_equity_amount',

- 'total_UT', 'customer_revenue', 'age', 'avg_balance', 'num_accs', 'balance_usd', 'available_balance_usd')).dropDuplicates(['cust_id'])

-display(customer_gold_features)

-

-# COMMAND ----------

-

-# DBTITLE 1,Read the telco table

-telco_gold_features = (spark.table("telco_gold")

- .select('cust_id', 'is_pre_paid', 'number_payment_delays_last12mo', 'pct_increase_annual_number_of_delays_last_3_year', 'phone_bill_amt', \

- 'avg_phone_bill_amt_lst12mo')).dropDuplicates(['cust_id'])

-display(telco_gold_features)

-

-# COMMAND ----------

-

-# DBTITLE 1,Adding some additional features on transactional trends

-fund_trans_gold_features = spark.table("fund_trans_gold").dropDuplicates(['cust_id'])

-

-for c in ['12m', '6m', '3m']:

- fund_trans_gold_features = fund_trans_gold_features.withColumn('tot_txn_cnt_'+c, col('sent_txn_cnt_'+c)+col('rcvd_txn_cnt_'+c))\

- .withColumn('tot_txn_amt_'+c, col('sent_txn_amt_'+c)+col('rcvd_txn_amt_'+c))

-

-fund_trans_gold_features = fund_trans_gold_features.withColumn('ratio_txn_amt_3m_12m', F.when(col('tot_txn_amt_12m')==0, 0).otherwise(col('tot_txn_amt_3m')/col('tot_txn_amt_12m')))\

- .withColumn('ratio_txn_amt_6m_12m', F.when(col('tot_txn_amt_12m')==0, 0).otherwise(col('tot_txn_amt_6m')/col('tot_txn_amt_12m')))\

- .na.fill(0)

-display(fund_trans_gold_features)

-

-# COMMAND ----------

-

-# DBTITLE 1,Consolidating all the features

-feature_df = customer_gold_features.join(telco_gold_features.alias('telco'), "cust_id", how="left")

-feature_df = feature_df.join(fund_trans_gold_features, "cust_id", how="left")

-display(feature_df)

-

-# COMMAND ----------

-

-# MAGIC %md-sandbox

-# MAGIC

-# MAGIC # Databricks Feature Store

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC Once our features are ready, we'll save them in Databricks Feature Store.

-# MAGIC

-# MAGIC Under the hood, feature store are backed by a Delta Lake table. This will allow discoverability and reusability of our feature across our organization, increasing team efficiency.

-# MAGIC

-# MAGIC

-# MAGIC Databricks Feature Store brings advanced capabilities to accelerate and simplify your ML journey, such as point in time support and online-store, fetching your features within ms for real time Serving.

-# MAGIC

-# MAGIC ### Why use Databricks Feature Store?

-# MAGIC

-# MAGIC Databricks Feature Store is fully integrated with other components of Databricks.

-# MAGIC

-# MAGIC * **Discoverability**. The Feature Store UI, accessible from the Databricks workspace, lets you browse and search for existing features.

-# MAGIC

-# MAGIC * **Lineage**. When you create a feature table with Feature Store, the data sources used to create the feature table are saved and accessible. For each feature in a feature table, you can also access the models, notebooks, jobs, and endpoints that use the feature.

-# MAGIC

-# MAGIC * **Batch and Online feature lookup for real time serving**. When you use features from Feature Store to train a model, the model is packaged with feature metadata. When you use the model for batch scoring or online inference, it automatically retrieves features from Feature Store. The caller does not need to know about them or include logic to look up or join features to score new data. This makes model deployment and updates much easier.

-# MAGIC

-# MAGIC * **Point-in-time lookups**. Feature Store supports time series and event-based use cases that require point-in-time correctness.

-# MAGIC

-# MAGIC

-# MAGIC For more details about Databricks Feature Store, run `dbdemos.install('feature-store')`

-

-# COMMAND ----------

-

-from databricks import feature_store

-fs = feature_store.FeatureStoreClient()

-

-# Drop the fs table if it was already existing to cleanup the demo state

-drop_fs_table(f"{catalog}.{db}.credit_decisioning_features")

-

-fs.create_table(

- name=f"{catalog}.{db}.credit_decisioning_features",

- primary_keys=["cust_id"],

- df=feature_df,

- description="Features for Credit Decisioning.")

-

-# COMMAND ----------

-

-# MAGIC %md

-# MAGIC

-# MAGIC ## Next steps

-# MAGIC

-# MAGIC After creating our features and storing them in the Databricks Feature Store, we can now proceed to the [03.2-AutoML-credit-decisioning]($./03.2-AutoML-credit-decisioning) and build out credit decisioning model.

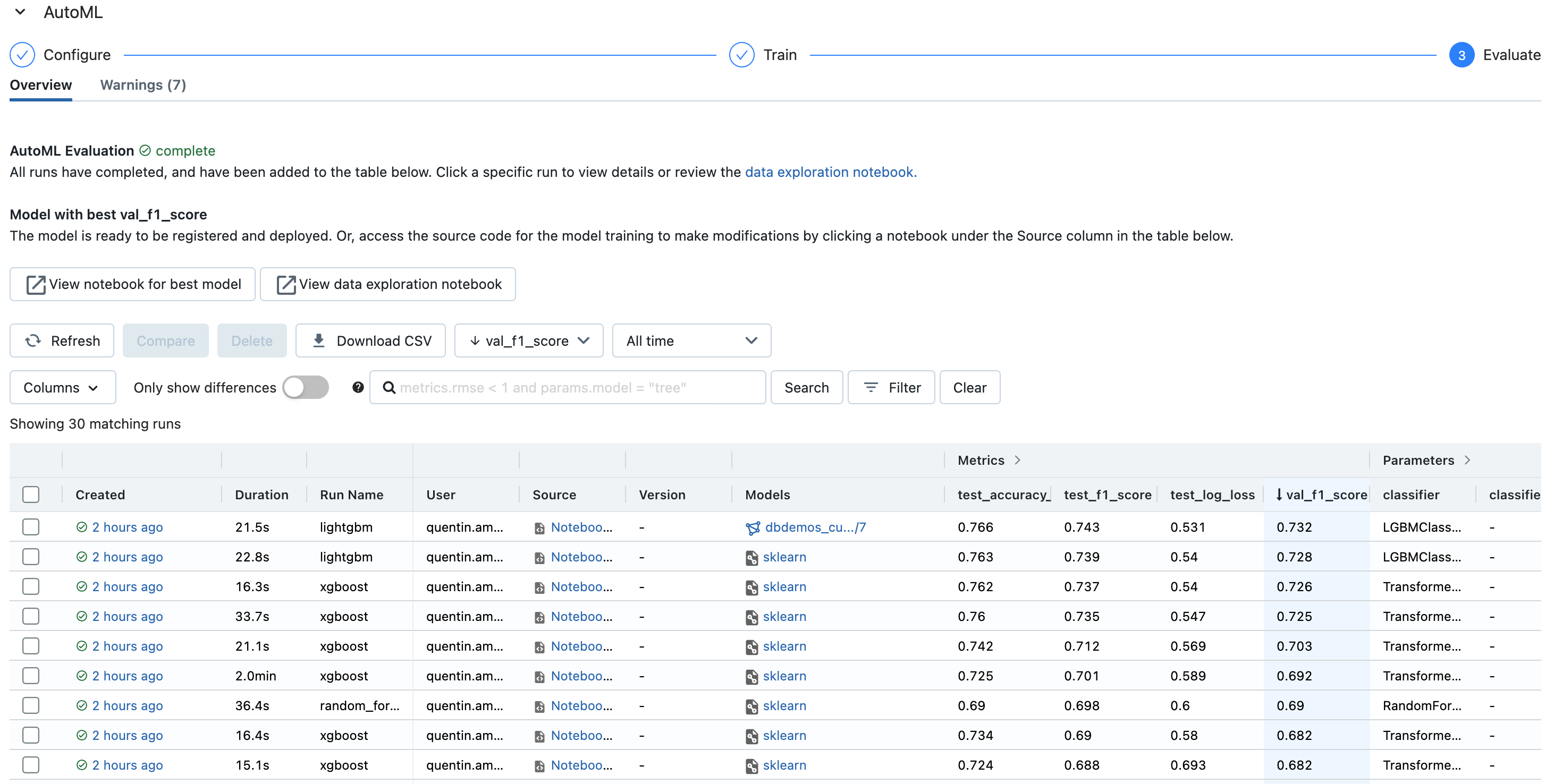

diff --git a/demo-FSI/lakehouse-fsi-credit-decisioning/03-Data-Science-ML/03.2-AutoML-credit-decisioning.py b/demo-FSI/lakehouse-fsi-credit-decisioning/03-Data-Science-ML/03.2-AutoML-credit-decisioning.py

deleted file mode 100644

index 5f8cf299..00000000

--- a/demo-FSI/lakehouse-fsi-credit-decisioning/03-Data-Science-ML/03.2-AutoML-credit-decisioning.py

+++ /dev/null

@@ -1,257 +0,0 @@

-# Databricks notebook source

-# MAGIC %md-sandbox

-# MAGIC

-# MAGIC # Data Science on the Databricks Lakehouse

-# MAGIC

-# MAGIC ## ML is key to disruption & personalization

-# MAGIC

-# MAGIC Being able to ingest and query our credit-related database is a first step, but this isn't enough to thrive in a very competitive market.

-# MAGIC

-# MAGIC Customers now expect real time personalization and new form of comunication. Modern data company achieve this with AI.

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC

90%

-# MAGIC

-# MAGIC Enterprise applications will be AI-augmented by 2025 — IDC

-# MAGIC

-# MAGIC

$10T+

-# MAGIC

-# MAGIC Projected business value creation by AI in 2030 — PwC

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC But a huge challenge is getting ML to work at scale!

-# MAGIC Most ML projects still fail before getting to production.

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC

-

-# COMMAND ----------

-

-# MAGIC %md

-# MAGIC

-# MAGIC ## So what makes machine learning and data science difficult?

-# MAGIC

-# MAGIC These are the top challenges we have observed companies struggle with:

-# MAGIC 1. Inability to ingest the required data in a timely manner,

-# MAGIC 2. Inability to properly control the access of the data,

-# MAGIC 3. Inability to trace problems in the feature store to the raw data,

-# MAGIC

-# MAGIC ... and many other data-related problems.

-

-# COMMAND ----------

-

-# MAGIC %md

-# MAGIC

-# MAGIC # Data-centric Machine Learning

-# MAGIC

-# MAGIC In Databricks, machine learning is not a separate product or service that needs to be "connected" to the data. The Lakehouse being a single, unified product, machine learning in Databricks "sits" on top of the data, so challenges like inability to discover and access data no longer exist.

-# MAGIC

-# MAGIC

-# MAGIC

-

-# COMMAND ----------

-

-# MAGIC %pip install databricks-sdk==0.36.0 mlflow==2.19.0 databricks-feature-store==0.17.0 scikit-learn==1.3.0

-# MAGIC dbutils.library.restartPython()

-

-# COMMAND ----------

-

-# MAGIC %run ../_resources/00-setup $reset_all_data=false

-

-# COMMAND ----------

-

-# MAGIC %md-sandbox

-# MAGIC

-# MAGIC # Credit Scoring default prediction

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC ## Single click deployment with AutoML

-# MAGIC

-# MAGIC

-# MAGIC Let's see how we can now leverage the credit decisioning data to build a model predicting and explaining customer creditworthiness.

-# MAGIC

-# MAGIC We'll start by retrieving our data from the feature store and creating our training dataset.

-# MAGIC

-# MAGIC We'll then use Databricks AutoML to automatically build our model.

-

-# COMMAND ----------

-

-# DBTITLE 1,Loading the training dataset from the Databricks Feature Store

-from databricks import feature_store

-fs = feature_store.FeatureStoreClient()

-features_set = fs.read_table(name=f"{catalog}.{db}.credit_decisioning_features")

-display(features_set)

-

-# COMMAND ----------

-

-# DBTITLE 1,Creating the label: "defaulted"

-credit_bureau_label = (spark.table("credit_bureau_gold")

- .withColumn("defaulted", F.when(col("CREDIT_DAY_OVERDUE") > 60, 1)

- .otherwise(0))

- .select("cust_id", "defaulted"))

-#As you can see, we have a fairly imbalanced dataset

-df = credit_bureau_label.groupBy('defaulted').count().toPandas()

-px.pie(df, values='count', names='defaulted', title='Credit default ratio')

-

-# COMMAND ----------

-

-# DBTITLE 1,Build our training dataset (join features and label)

-training_dataset = credit_bureau_label.join(features_set, "cust_id", "inner")

-

-# COMMAND ----------

-

-# MAGIC %md

-# MAGIC

-# MAGIC ## Balancing our dataset

-# MAGIC

-# MAGIC Let's downsample and upsample our dataset to improve our model performance

-

-# COMMAND ----------

-

-major_df = training_dataset.filter(col("defaulted") == 0)

-minor_df = training_dataset.filter(col("defaulted") == 1)

-

-# duplicate the minority rows

-oversampled_df = minor_df.union(minor_df)

-

-# downsample majority rows

-undersampled_df = major_df.sample(oversampled_df.count()/major_df.count()*3, 42)

-

-# combine both oversampled minority rows and undersampled majority rows, this will improve our balance while preseving enough information.

-train_df = undersampled_df.unionAll(oversampled_df).drop('cust_id').na.fill(0)

-# Save it as a table to be able to select it with the AutoML UI.

-train_df.write.mode('overwrite').saveAsTable('credit_risk_train_df')

-px.pie(train_df.groupBy('defaulted').count().toPandas(), values='count', names='defaulted', title='Credit default ratio')

-

-# COMMAND ----------

-

-# MAGIC %md-sandbox

-# MAGIC

-# MAGIC ## Accelerating credit scoring model creation using MLFlow and Databricks AutoML

-# MAGIC

-# MAGIC MLFlow is an open source project allowing model tracking, packaging and deployment. Every time your Data Science team works on a model, Databricks will track all parameters and data used and will auto-log them. This ensures ML traceability and reproductibility, making it easy to know what parameters/data were used to build each model and model version.

-# MAGIC

-# MAGIC ### A glass-box solution that empowers data teams without taking control away

-# MAGIC

-# MAGIC While Databricks simplifies model deployment and governance (MLOps) with MLFlow, bootstraping new ML projects can still be a long and inefficient process.

-# MAGIC

-# MAGIC Instead of creating the same boilerplate for each new project, Databricks AutoML can automatically generate state of the art models for Classifications, Regression, and Forecasting.

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC Models can be directly deployed, or instead leverage generated notebooks to boostrap projects with best-practices, saving you weeks worth of effort.

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC

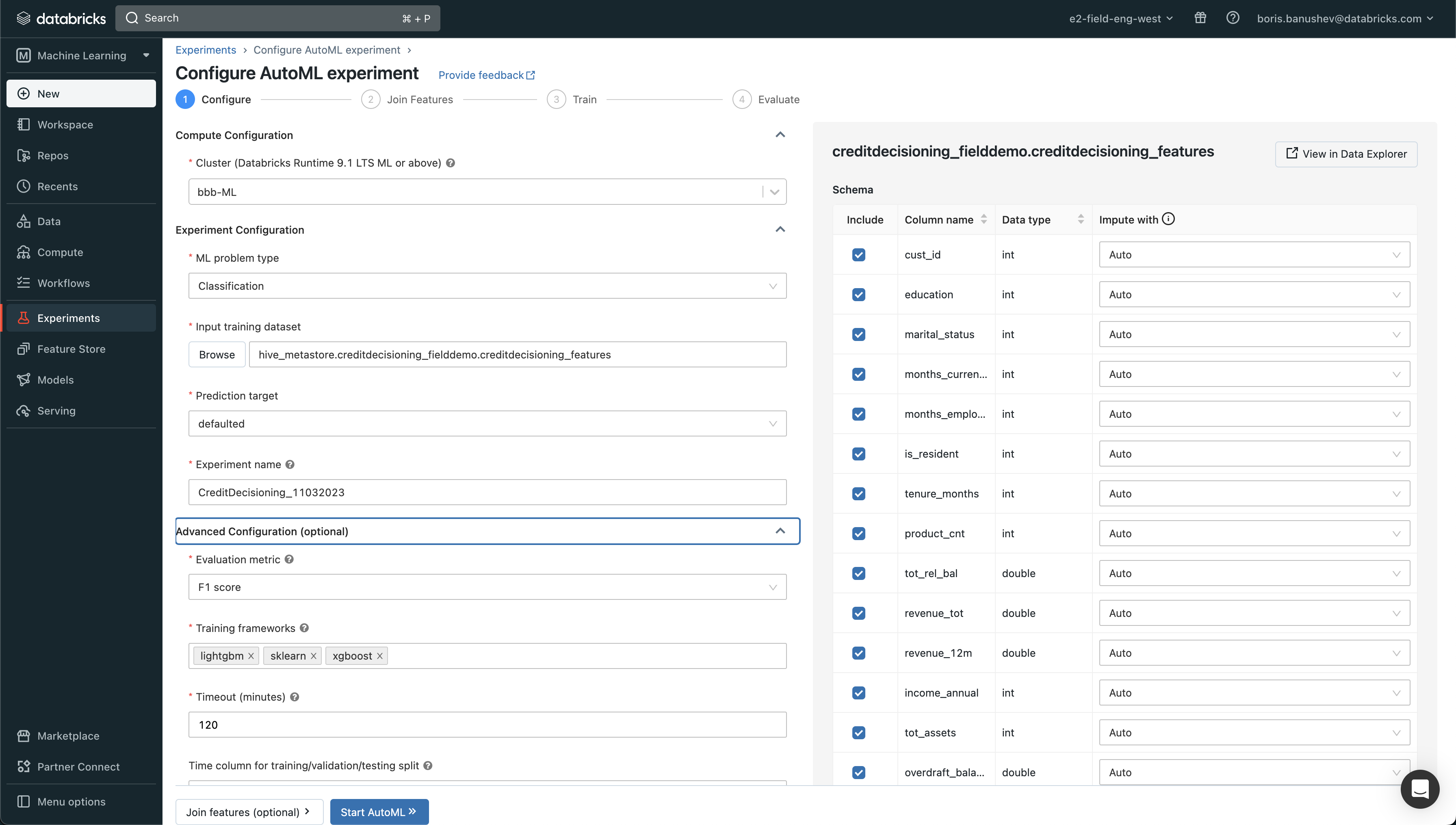

-# MAGIC ### Using Databricks Auto ML with our Credit Scoring dataset

-# MAGIC

-# MAGIC AutoML is available in the "Machine Learning" space. All we have to do is start a new AutoML Experiments and select the feature table we just created (`creditdecisioning_features`)

-# MAGIC

-# MAGIC Our prediction target is the `defaulted` column.

-# MAGIC

-# MAGIC Click on Start, and Databricks will do the rest.

-# MAGIC

-# MAGIC While this is done using the UI, you can also leverage the [python API](https://docs.databricks.com/applications/machine-learning/automl.html#automl-python-api-1)

-

-# COMMAND ----------

-

-model_name = "dbdemos_fsi_credit_decisioning"

-xp_path = "/Shared/dbdemos/experiments/lakehouse-fsi-credit-decisioning"

-xp_name = f"automl_credit_{datetime.now().strftime('%Y-%m-%d_%H:%M:%S')}"

-try:

- from databricks import automl

- automl_run = automl.classify(

- experiment_name = xp_name,

- experiment_dir = xp_path,

- dataset = train_df.sample(0.1),

- target_col = "defaulted",

- timeout_minutes = 10

- )

- #Make sure all users can access dbdemos shared experiment

- DBDemos.set_experiment_permission(f"{xp_path}/{xp_name}")

-except Exception as e:

- if "cannot import name 'automl'" in str(e):

- # Note: cannot import name 'automl' from 'databricks' likely means you're using serverless. Dbdemos doesn't support autoML serverless API - this will be improved soon.

- # Adding a temporary workaround to make sure it works well for now - ignore this for classic run

- automl_run = DBDemos.create_mockup_automl_run(f"{xp_path}/{xp_name}", train_df.sample(0.1).toPandas(), model_name=model_name, target_col="defaulted")

- else:

- raise e

-

-# COMMAND ----------

-

-# MAGIC %md

-# MAGIC ## Deploying our model in production

-# MAGIC

-# MAGIC Our model is now ready. We can review the notebook generated by the auto-ml run and customize if if required.

-# MAGIC

-# MAGIC For this demo, we'll consider that our model is ready and deploy it in production in our Model Registry:

-

-# COMMAND ----------

-

-model_name = "dbdemos_fsi_credit_decisioning"

-from mlflow import MlflowClient

-import mlflow

-

-#Use Databricks Unity Catalog to save our model

-mlflow.set_registry_uri('databricks-uc')

-client = MlflowClient()

-

-#Add model within our catalog

-latest_model = mlflow.register_model(f'runs:/{automl_run.best_trial.mlflow_run_id}/model', f"{catalog}.{db}.{model_name}")

-# Flag it as Production ready using UC Aliases

-client.set_registered_model_alias(name=f"{catalog}.{db}.{model_name}", alias="prod", version=latest_model.version)

-#DBDemos.set_model_permission(f"{catalog}.{db}.{model_name}", "ALL_PRIVILEGES", "account users")

-

-# COMMAND ----------

-

-# MAGIC %md

-# MAGIC We just moved our automl model as production ready!

-# MAGIC

-# MAGIC Open [the dbdemos_fsi_credit_decisioning model](#mlflow/models/dbdemos_fsi_credit_decisioning) to explore its artifact and analyze the parameters used, including traceability to the notebook used for its creation.

-

-# COMMAND ----------

-

-# MAGIC %md

-# MAGIC

-# MAGIC ## Our model predicting default risks is now deployed in production

-# MAGIC

-# MAGIC

-# MAGIC So far we have:

-# MAGIC * ingested all required data in a single source of truth,

-# MAGIC * properly secured all data (including granting granular access controls, masked PII data, applied column level filtering),

-# MAGIC * enhanced that data through feature engineering,

-# MAGIC * used MLFlow AutoML to track experiments and build a machine learning model,

-# MAGIC * registered the model.

-# MAGIC

-# MAGIC ### Next steps

-# MAGIC We're now ready to use our model use it for:

-# MAGIC

-# MAGIC - Batch inferences in notebook [03.3-Batch-Scoring-credit-decisioning]($./03.3-Batch-Scoring-credit-decisioning) to start using it for identifying currently underbanked customers with good credit-worthiness (**increase the revenue**) and predict current credit-owners who might default so we can prevent such defaults from happening (**manage risk**),

-# MAGIC - Real time inference with [03.4-model-serving-BNPL-credit-decisioning]($./03.4-model-serving-BNPL-credit-decisioning) to enable ```Buy Now, Pay Later``` capabilities within the bank.

-# MAGIC

-# MAGIC Extra: review model explainability & fairness with [03.5-Explainability-and-Fairness-credit-decisioning]($./03.5-Explainability-and-Fairness-credit-decisioning)

diff --git a/demo-FSI/lakehouse-fsi-credit-decisioning/03-Data-Science-ML/03.2-Feature-Updates-credit-decisioning.py b/demo-FSI/lakehouse-fsi-credit-decisioning/03-Data-Science-ML/03.2-Feature-Updates-credit-decisioning.py

new file mode 100644

index 00000000..0e8da74c

--- /dev/null

+++ b/demo-FSI/lakehouse-fsi-credit-decisioning/03-Data-Science-ML/03.2-Feature-Updates-credit-decisioning.py

@@ -0,0 +1,171 @@

+# Databricks notebook source

+# MAGIC %md

+# MAGIC

+# MAGIC # Feature Updates

+# MAGIC

+# MAGIC In responsible credit scoring, ensuring that machine learning models operate on high-quality and up-to-date data is essential. Continuous feature updates play a crucial role in maintaining model accuracy, fairness, and regulatory compliance. By centralizing feature management, we can improve governance, enforce lineage tracking, and ensure consistency across multiple ML projects.

+# MAGIC

+# MAGIC This notebook focuses on the ingestion, transformation, and tracking of features within the Databricks Feature Store. We ensure that every update is logged for traceability and that feature engineering practices align with Responsible AI principles. With transparent feature updates, we enhance the model’s effectiveness while meeting compliance standards.

+# MAGIC

+# MAGIC

+

+# COMMAND ----------

+

+# MAGIC %run ../_resources/00-setup $reset_all_data=false

+

+# COMMAND ----------

+

+# MAGIC %md

+# MAGIC

+# MAGIC # Building our Features for Credit Default risks

+# MAGIC

+# MAGIC To build our model predicting credit default risks, we need a comprehensive set of features that capture various aspects of customer behavior, financial activity, and risk indicators. Our primary data sources include:

+# MAGIC

+# MAGIC - `customer_gold`: Contains aggregated customer demographic, behavioral, and credit history attributes.

+# MAGIC - `telco_gold`: Includes telecommunications data, such as call patterns and payment behaviors.

+# MAGIC - `fund_trans_gold`: Provides insights into customer fund movements, transaction behaviors, and cash flow trends.

+# MAGIC

+# MAGIC To improve governance and centralize feature management for multiple machine learning projects, we leverage the Databricks Feature Store.

+

+# COMMAND ----------

+

+# DBTITLE 1,Read the customer table

+customer_gold_features = (spark.table("customer_gold")

+ .withColumn('age', int(date.today().year) - col('birth_year'))

+ .select('cust_id', 'education', 'marital_status', 'months_current_address', 'months_employment', 'is_resident',

+ 'tenure_months', 'product_cnt', 'tot_rel_bal', 'revenue_tot', 'revenue_12m', 'income_annual', 'tot_assets',

+ 'overdraft_balance_amount', 'overdraft_number', 'total_deposits_number', 'total_deposits_amount', 'total_equity_amount',

+ 'total_UT', 'customer_revenue', 'age', 'gender', 'avg_balance', 'num_accs', 'balance_usd', 'available_balance_usd')).dropDuplicates(['cust_id'])

+display(customer_gold_features)

+

+# COMMAND ----------

+

+# DBTITLE 1,Read the telco table

+telco_gold_features = (spark.table("telco_gold")

+ .select('cust_id', 'is_pre_paid', 'number_payment_delays_last12mo', 'pct_increase_annual_number_of_delays_last_3_year', 'phone_bill_amt', \

+ 'avg_phone_bill_amt_lst12mo')).dropDuplicates(['cust_id'])

+display(telco_gold_features)

+

+# COMMAND ----------

+

+# DBTITLE 1,Adding some additional features on transactional trends

+fund_trans_gold_features = spark.table("fund_trans_gold").dropDuplicates(['cust_id'])

+

+for c in ['12m', '6m', '3m']:

+ fund_trans_gold_features = fund_trans_gold_features.withColumn('tot_txn_cnt_'+c, col('sent_txn_cnt_'+c)+col('rcvd_txn_cnt_'+c))\

+ .withColumn('tot_txn_amt_'+c, col('sent_txn_amt_'+c)+col('rcvd_txn_amt_'+c))

+

+fund_trans_gold_features = fund_trans_gold_features.withColumn('ratio_txn_amt_3m_12m', F.when(col('tot_txn_amt_12m')==0, 0).otherwise(col('tot_txn_amt_3m')/col('tot_txn_amt_12m')))\

+ .withColumn('ratio_txn_amt_6m_12m', F.when(col('tot_txn_amt_12m')==0, 0).otherwise(col('tot_txn_amt_6m')/col('tot_txn_amt_12m')))\

+ .na.fill(0)

+display(fund_trans_gold_features)

+

+# COMMAND ----------

+

+# DBTITLE 1,Consolidating all the features

+feature_df = customer_gold_features.join(telco_gold_features.alias('telco'), "cust_id", how="left")

+feature_df = feature_df.join(fund_trans_gold_features, "cust_id", how="left")

+display(feature_df)

+

+# COMMAND ----------

+

+# MAGIC %md-sandbox

+# MAGIC

+# MAGIC # Databricks Feature Store

+# MAGIC

+# MAGIC Once our features are ready, we'll save them in Databricks Feature Store.

+# MAGIC

+# MAGIC Under the hood, feature store are backed by a Delta Lake table. This will allow discoverability and reusability of our feature across our organization, increasing team efficiency.

+# MAGIC

+# MAGIC

+# MAGIC Databricks Feature Store brings advanced capabilities to accelerate and simplify your ML journey, such as point in time support and online-store, fetching your features within ms for real time Serving.

+# MAGIC

+# MAGIC ### Why use Databricks Feature Store?

+# MAGIC

+# MAGIC Databricks Feature Store is fully integrated with other components of Databricks.

+# MAGIC

+# MAGIC * **Discoverability**. The Feature Store UI, accessible from the Databricks workspace, lets you browse and search for existing features.

+# MAGIC

+# MAGIC * **Lineage**. When you create a feature table with Feature Store, the data sources used to create the feature table are saved and accessible. For each feature in a feature table, you can also access the models, notebooks, jobs, and endpoints that use the feature.

+# MAGIC

+# MAGIC * **Batch and Online feature lookup for real time serving**. When you use features from Feature Store to train a model, the model is packaged with feature metadata. When you use the model for batch scoring or online inference, it automatically retrieves features from Feature Store. The caller does not need to know about them or include logic to look up or join features to score new data. This makes model deployment and updates much easier.

+# MAGIC

+# MAGIC * **Point-in-time lookups**. Feature Store supports time series and event-based use cases that require point-in-time correctness.

+# MAGIC

+# MAGIC

+# MAGIC For more details about Databricks Feature Store, run `dbdemos.install('feature-store')`

+

+# COMMAND ----------

+

+from databricks.feature_engineering import FeatureEngineeringClient

+

+fe = FeatureEngineeringClient()

+

+# Drop the fs table if it was already existing to cleanup the demo state

+try:

+ fe.drop_table(name=f"{catalog}.{db}.credit_decisioning_features")

+ print("Dropped existing feature table.")

+except:

+ print("Feature table does not exist. Creating a new feature table.")

+

+# Create feature table with `cust_id` as the primary key.

+fe.create_table(

+ name=f"{catalog}.{db}.credit_decisioning_features",

+ primary_keys="cust_id",

+ schema=feature_df.schema,

+ description="Features for Credit Decisioning.")

+

+fe.write_table(

+ name=f"{catalog}.{db}.credit_decisioning_features",

+ df = feature_df,

+ mode = 'merge'

+)

+

+# COMMAND ----------

+

+# MAGIC %md

+# MAGIC ## Transparency

+# MAGIC

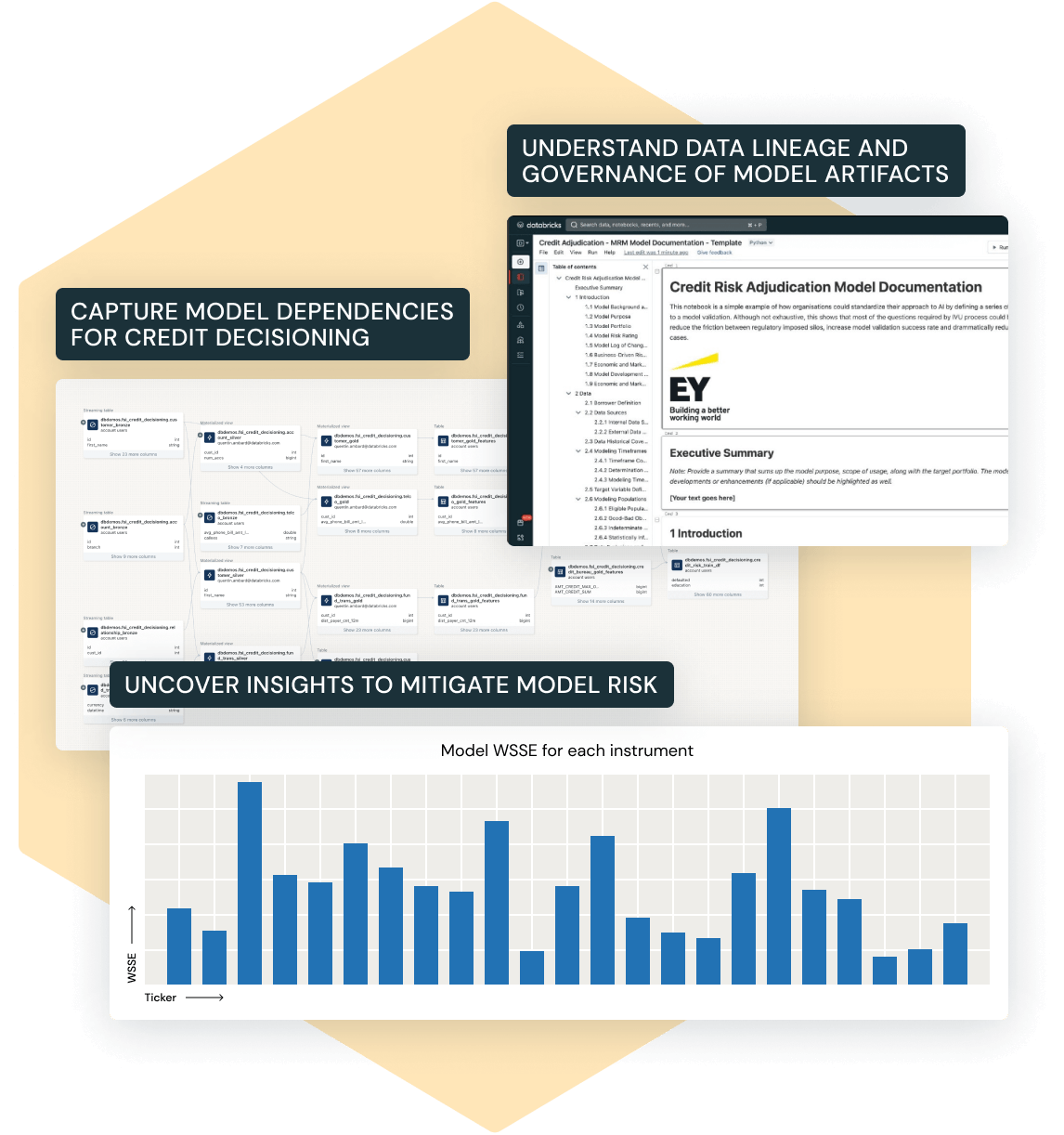

+# MAGIC Databricks Unity Catalog's **automated data lineage** feature tracks and visualizes data flow from ingestion to consumption. It ensures transparency in feature engineering for machine learning by capturing transformations, dependencies, and usage across notebooks, workflows, and dashboards. This enhances reproducibility, debugging, compliance, and model accuracy.

+# MAGIC

+# MAGIC Accessing lineage via [system tables](https://docs.databricks.com/en/admin/system-tables/lineage.html) allows users to query lineage metadata, track data dependencies, and analyze usage patterns. This structured approach aids auditing, debugging, and optimizing workflows, ensuring data quality across analytics and ML pipelines.

+# MAGIC

+# MAGIC Next, we'll import lineage data for the feature tables created in this Notebook.

+

+# COMMAND ----------

+

+# MAGIC %sql

+# MAGIC

+# MAGIC select * from system.access.table_lineage

+# MAGIC where target_table_catalog=current_catalog()

+# MAGIC and target_table_schema=current_schema()

+# MAGIC and target_table_name = 'credit_decisioning_features';

+

+# COMMAND ----------

+

+# MAGIC %md

+# MAGIC ## Documentation of the data

+# MAGIC

+# MAGIC In Databricks, the AI-generated column and table description feature leverages machine learning models to automatically analyze and generate meaningful metadata descriptions for tables and columns within a dataset. This functionality improves data discovery and understanding by providing natural language descriptions, helping users quickly interpret data without needing to manually write documentation. The AI can identify patterns, data types, and relationships between columns, offering suggestions that can enhance data governance, streamline collaboration, and make datasets more accessible, especially for those unfamiliar with the underlying schema. This feature is part of Databricks' broader effort to simplify data exploration and enhance productivity within its unified data analytics platform.

+

+# COMMAND ----------

+

+table_name = "credit_decisioning_features"

+

+table_description = spark.sql(f"DESCRIBE TABLE EXTENDED {table_name}").filter("col_name = 'Comment'").select("data_type").collect()[0][0]

+

+column_descriptions = spark.sql(f"DESCRIBE TABLE EXTENDED {table_name}").filter("col_name != ''").select("col_name", "comment").collect()

+

+# COMMAND ----------

+

+# MAGIC %md

+# MAGIC

+# MAGIC ## Next Steps

+# MAGIC

+# MAGIC With our feature set prepared and stored, the next step is model training. In the [06.3-Model-Training]($./06-Responsible-AI/06.3-Model-Training) notebook, we will:

+# MAGIC - Train multiple candidate models using the engineered features.

+# MAGIC - Evaluate models based on fairness, accuracy, and stability metrics.

+# MAGIC - Log model artifacts, ensuring full reproducibility.

+# MAGIC

+# MAGIC By maintaining transparency and governance throughout feature updates and model training, we lay the foundation for responsible credit decisioning and robust AI deployment.

diff --git a/demo-FSI/lakehouse-fsi-credit-decisioning/03-Data-Science-ML/03.3-Batch-Scoring-credit-decisioning.py b/demo-FSI/lakehouse-fsi-credit-decisioning/03-Data-Science-ML/03.3-Batch-Scoring-credit-decisioning.py

deleted file mode 100644

index af64954b..00000000

--- a/demo-FSI/lakehouse-fsi-credit-decisioning/03-Data-Science-ML/03.3-Batch-Scoring-credit-decisioning.py

+++ /dev/null

@@ -1,85 +0,0 @@

-# Databricks notebook source

-# MAGIC %md-sandbox

-# MAGIC # Use the best AutoML generated model to batch score credit worthiness

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC Databricks AutoML runs experiments across a grid and creates many models and metrics to determine the best models among all trials. This is a glass-box approach to create a baseline model, meaning we have all the code artifacts and experiments available afterwards.

-# MAGIC

-# MAGIC Here, we selected the Notebook from the best run from the AutoML experiment.

-# MAGIC

-# MAGIC All the code below has been automatically generated. As data scientists, we can tune it based on our business knowledge, or use the generated model as-is.

-# MAGIC

-# MAGIC This saves data scientists hours of developement and allows team to quickly bootstrap and validate new projects, especally when we may not know the predictors for alternative data such as the telco payment data.

-# MAGIC

-# MAGIC

-# MAGIC

-

-# COMMAND ----------

-

-# MAGIC %pip install mlflow==2.19.0

-# MAGIC dbutils.library.restartPython()

-

-# COMMAND ----------

-

-# MAGIC %run ../_resources/00-setup $reset_all_data=false

-

-# COMMAND ----------

-

-# MAGIC %md-sandbox

-# MAGIC

-# MAGIC ## Running batch inference to score our existing database

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC Now that our model was created and deployed in production within the MLFlow registry.

-# MAGIC

-# MAGIC

-# MAGIC We can now easily load it calling the `Production` stage, and use it in any Data Engineering pipeline (a job running every night, in streaming or even within a Delta Live Table pipeline).

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC We'll then save this information as a new table without our FS database, and start building dashboards and alerts on top of it to run live analysis.

-

-# COMMAND ----------

-

-model_name = "dbdemos_fsi_credit_decisioning"

-import mlflow

-mlflow.set_registry_uri('databricks-uc')

-

-# Load model as a Spark UDF.

-loaded_model = mlflow.pyfunc.spark_udf(spark, model_uri=f"models:/{catalog}.{db}.{model_name}@prod", result_type='double')

-

-# COMMAND ----------

-

-features = loaded_model.metadata.get_input_schema().input_names()

-

-underbanked_df = spark.table("credit_decisioning_features").fillna(0) \

- .withColumn("prediction", loaded_model(F.struct(*features))).cache()

-

-display(underbanked_df)

-

-# COMMAND ----------

-

-# MAGIC %md

-# MAGIC

-# MAGIC In the scored data frame above, we have essentially created an end-to-end process to predict credit worthiness for any customer, regardless of whether the customer has an existing bank account. We have a binary prediction which captures this and incorporates all the intellience from Databricks AutoML and curated features from our feature store.

-

-# COMMAND ----------

-

-underbanked_df.write.mode("overwrite").saveAsTable(f"underbanked_prediction")

-

-# COMMAND ----------

-

-# MAGIC %md

-# MAGIC

-# MAGIC ### Next steps

-# MAGIC

-# MAGIC * Deploy your model for real time inference with [03.4-model-serving-BNPL-credit-decisioning]($./03.4-model-serving-BNPL-credit-decisioning) to enable ```Buy Now, Pay Later``` capabilities within the bank.

-# MAGIC

-# MAGIC Or

-# MAGIC

-# MAGIC * Making sure your model is fair towards customers of any demographics are extremely important parts of building production-ready ML models for FSI use cases.

-# MAGIC Explore your model with [03.5-Explainability-and-Fairness-credit-decisioning]($./03.5-Explainability-and-Fairness-credit-decisioning) on the Lakehouse.

diff --git a/demo-FSI/lakehouse-fsi-credit-decisioning/03-Data-Science-ML/03.3-Model-Training-credit-decisioning.py b/demo-FSI/lakehouse-fsi-credit-decisioning/03-Data-Science-ML/03.3-Model-Training-credit-decisioning.py

new file mode 100644

index 00000000..eca100ee

--- /dev/null

+++ b/demo-FSI/lakehouse-fsi-credit-decisioning/03-Data-Science-ML/03.3-Model-Training-credit-decisioning.py

@@ -0,0 +1,191 @@

+# Databricks notebook source

+# MAGIC %md

+# MAGIC

+# MAGIC # Model Training

+# MAGIC

+# MAGIC In Databricks, machine learning is not a separate product or service that needs to be "connected" to the data. The Lakehouse being a single, unified product, machine learning in Databricks "sits" on top of the data, so challenges like inability to discover and access data no longer exist.

+# MAGIC

+# MAGIC

+# MAGIC

+

+# COMMAND ----------

+

+# MAGIC %run ../_resources/00-setup $reset_all_data=false

+

+# COMMAND ----------

+

+# MAGIC %md-sandbox

+# MAGIC

+# MAGIC ## Building a Responsible Credit Scoring Model

+# MAGIC

+# MAGIC With our credit decisioning data prepared, we can now leverage it to build a predictive model assessing customer creditworthiness. Our approach will emphasize transparency, fairness, and governance at every step.

+# MAGIC

+# MAGIC Steps in Model Training:

+# MAGIC - **Retrieve Data from the Feature Store:** We begin by accessing the curated and validated features stored in the Databricks Feature Store. This ensures consistency, traceability, and compliance with feature engineering best practices.

+# MAGIC - **Create the Training Dataset:** We assemble a well-balanced training dataset by selecting relevant features and handling missing or biased data points.

+# MAGIC - **Leverage Databricks AutoML:** To streamline model development, we use Databricks AutoML to automatically build and evaluate multiple models. This step ensures we select the most effective model while adhering to Responsible AI principles.

+

+# COMMAND ----------

+

+# DBTITLE 1,Loading the training dataset from the Databricks Feature Store

+from databricks.feature_engineering import FeatureEngineeringClient

+fe = FeatureEngineeringClient()

+

+features_set = fe.read_table(name=f"{catalog}.{db}.credit_decisioning_features")

+display(features_set)

+

+# COMMAND ----------

+

+# DBTITLE 1,Creating the label: "defaulted"

+credit_bureau_label = (spark.table("credit_bureau_gold")

+ .withColumn("defaulted", F.when(col("CREDIT_DAY_OVERDUE") > 60, 1)

+ .otherwise(0))

+ .select("cust_id", "defaulted"))

+#As you can see, we have a fairly imbalanced dataset

+df = credit_bureau_label.groupBy('defaulted').count().toPandas()

+px.pie(df, values='count', names='defaulted', title='Credit default ratio')

+

+# COMMAND ----------

+

+# DBTITLE 1,Build our training dataset (join features and label)

+training_dataset = credit_bureau_label.join(features_set, "cust_id", "inner")

+training_dataset.write.mode('overwrite').saveAsTable('credit_decisioning_features_labels')

+

+# COMMAND ----------

+

+# MAGIC %md

+# MAGIC

+# MAGIC ## Adressing the class imbalance of our dataset

+# MAGIC

+# MAGIC Let's downsample and upsample our dataset to improve our model performance

+

+# COMMAND ----------

+

+major_df = training_dataset.filter(col("defaulted") == 0)

+minor_df = training_dataset.filter(col("defaulted") == 1)

+

+# duplicate the minority rows

+oversampled_df = minor_df.union(minor_df)

+

+# downsample majority rows

+undersampled_df = major_df.sample(oversampled_df.count()/major_df.count()*3, 42)

+

+

+# COMMAND ----------

+

+# combine both oversampled minority rows and undersampled majority rows, this will improve our balance while preseving enough information.

+train_df = undersampled_df.unionAll(oversampled_df).drop('cust_id').na.fill(0)

+

+# COMMAND ----------

+

+# Save it as a table to be able to select it with the AutoML UI.

+train_df.write.mode('overwrite').saveAsTable('credit_risk_train_df')

+px.pie(train_df.groupBy('defaulted').count().toPandas(), values='count', names='defaulted', title='Credit default ratio')

+

+# COMMAND ----------

+

+# MAGIC %md

+# MAGIC ## Addressing Demographic or Ethical Bias

+# MAGIC

+# MAGIC When dealing with demographic or ethical bias—where disparities exist across sensitive attributes like gender, race, or age—standard class balancing techniques may be insufficient. Instead, more targeted strategies are used to promote fairness. Pre-processing methods like reweighing assign different instance weights to ensure equitable representation across groups. Techniques such as the disparate impact remover modify feature values to reduce bias while preserving predictive utility. In-processing approaches like adversarial debiasing involve training the main model alongside an adversary that attempts to predict the sensitive attribute, thereby encouraging the model to learn representations that are less biased. Additionally, fair sampling methods, such as Kamiran’s preferential sampling, selectively sample training data to correct for group imbalances. These approaches aim to improve fairness metrics like demographic parity or equal opportunity while maintaining model performance.

+

+# COMMAND ----------

+

+# MAGIC %md-sandbox

+# MAGIC

+# MAGIC ## Accelerating credit scoring model creation using MLFlow and Databricks AutoML

+# MAGIC

+# MAGIC MLFlow is an open source project allowing model tracking, packaging and deployment. Every time your Data Science team works on a model, Databricks will track all parameters and data used and will auto-log them. This ensures ML transparency, traceability, and reproducibility, making it easy to know what parameters/data were used to build each model and model version.

+# MAGIC

+# MAGIC ### A glass-box solution that empowers data teams without taking control away

+# MAGIC

+# MAGIC While Databricks simplifies model deployment and governance (MLOps) with MLFlow, bootstraping new ML projects can still be a long and inefficient process.

+# MAGIC

+# MAGIC Instead of creating the same boilerplate for each new project, Databricks AutoML can automatically generate state of the art models for Classifications, Regression, and Forecasting.

+# MAGIC

+# MAGIC

+# MAGIC

+# MAGIC

+# MAGIC

+# MAGIC Models can be directly deployed, or instead leverage generated notebooks to boostrap projects with best-practices, saving you weeks worth of effort.

+# MAGIC

+# MAGIC

+# MAGIC

+# MAGIC ### Using Databricks Auto ML with our Credit Scoring dataset

+# MAGIC

+# MAGIC AutoML is available in the "Machine Learning" space. All we have to do is start a new AutoML Experiments and select the feature table we just created (`creditdecisioning_features`)

+# MAGIC

+# MAGIC Our prediction target is the `defaulted` column.

+# MAGIC

+# MAGIC Click on Start, and Databricks will do the rest.

+# MAGIC

+# MAGIC While this is done using the UI, you can also leverage the [python API](https://docs.databricks.com/applications/machine-learning/automl.html#automl-python-api-1)

+

+# COMMAND ----------

+

+from databricks import automl

+xp_path = "/Shared/rai/experiments/credit-decisioning"

+xp_name = f"automl_rai_credit_{datetime.now().strftime('%Y-%m-%d_%H:%M:%S')}"

+automl_run = automl.classify(

+ experiment_name = xp_name,

+ experiment_dir = xp_path,

+ dataset = train_df.sample(0.1),

+ target_col = "defaulted",

+ timeout_minutes = 5

+)

+

+# COMMAND ----------

+

+# MAGIC %md

+# MAGIC ## Register our model in Unity Catalog

+# MAGIC

+# MAGIC Our model is now ready. We can review the notebook generated by the auto-ml run and customize if if required.

+# MAGIC

+# MAGIC For this demo, we'll consider that our model is ready to be registered in Unity Catalog:

+

+# COMMAND ----------

+

+import mlflow

+

+#Use Databricks Unity Catalog to save our model

+mlflow.set_registry_uri('databricks-uc')

+client = mlflow.MlflowClient()

+

+# Register the model to Unity Catalog

+try:

+ result = mlflow.register_model(model_uri=f"runs:/{automl_run.best_trial.mlflow_run_id}/model", name=f"{catalog}.{db}.{model_name}")

+ print(f"Model registered with version: {result.version}")

+except mlflow.exceptions.MlflowException as e:

+ print(f"Error registering model: {e}")

+

+# Flag it as Production ready using UC Aliases

+client.set_registered_model_alias(name=f"{catalog}.{db}.{model_name}", alias="None", version=result.version)

+

+# COMMAND ----------

+

+# MAGIC %md-sandbox

+# MAGIC

+# MAGIC ## Generate Model Documentation

+# MAGIC

+# MAGIC

+# MAGIC

+# MAGIC Once we have trained the model, we generate comprehensive model documentation using [Databricks' solutions accelerator](https://www.databricks.com/solutions/accelerators/model-risk-management-with-ey). This step is critical for maintaining compliance, governance, and transparency in financial services.

+# MAGIC

+# MAGIC #### Benefits of Automated Model Documentation:

+# MAGIC

+# MAGIC - Streamlined Model Governance: Automatically generate structured documentation for both machine learning and non-machine learning models, ensuring regulatory alignment.

+# MAGIC - Integrated Data Visualization & Reporting: Provide insights into model performance with built-in dashboards and visual analytics.

+# MAGIC - Risk Identification for Banking Models: Help model validation teams detect and mitigate risks associated with incorrect or misused models in financial decisioning.

+# MAGIC - Foundations for Explainable AI: Enhance trust by making every stage of the model lifecycle transparent, accelerating model validation and deployment processes.

+

+# COMMAND ----------

+

+# MAGIC %md

+# MAGIC ## Next Steps

+# MAGIC

+# MAGIC With our model trained and documented, the next step is validation. In the [06.4-Model-Validation]($./06-Responsible-AI/06.4-Model-Validation) notebook, we will conduct compliance checks, pre-deployment tests, and fairness evaluations. This ensures that our model meets regulatory requirements and maintains transparency before it is deployed into production.

+

+# COMMAND ----------

+

+

diff --git a/demo-FSI/lakehouse-fsi-credit-decisioning/03-Data-Science-ML/03.4-Model-Validation-credit-decisioning.py b/demo-FSI/lakehouse-fsi-credit-decisioning/03-Data-Science-ML/03.4-Model-Validation-credit-decisioning.py

new file mode 100644

index 00000000..033b784a

--- /dev/null

+++ b/demo-FSI/lakehouse-fsi-credit-decisioning/03-Data-Science-ML/03.4-Model-Validation-credit-decisioning.py

@@ -0,0 +1,367 @@

+# Databricks notebook source

+# MAGIC %md-sandbox

+# MAGIC

+# MAGIC # Model Validation

+# MAGIC

+# MAGIC Model validation is a critical step in ensuring the compliance, fairness, and reliability of our credit scoring model before deployment. This notebook performs key compliance checks to align with Responsible AI principles. Specifically, we:

+# MAGIC

+# MAGIC - Validate model fairness for existing credit customers.

+# MAGIC - Analyze feature importance and model behavior using Shapley values.

+# MAGIC - Log custom metrics for auditing and transparency.

+# MAGIC - Ensure compliance with regulatory fairness constraints.

+# MAGIC

+# MAGIC In addition, we also implement the champion-challenger framework to ensure that only the most effective and responsible model is promoted to a higher enviroment. This approach allows us to:

+# MAGIC - Compare the current production model (champion model) with a newly trained model (challenger model).

+# MAGIC - Incorporate human oversight to validate the challenger model before deployment.

+# MAGIC - Maintain full traceability and accountability at each stage of model deployment.

+# MAGIC

+# MAGIC Model validation includes both the model compliance checks and champion-challenger testing. It is only after a model passes these two checks that it is allowed to progress to a high environment. To do so, we:

+# MAGIC - Register the validated model in Unity Catalog and transition it to the next stage.

+# MAGIC

+# MAGIC By following this structured validation approach, we ensure that model transitions are transparent, fair, and aligned with Responsible AI principles.

+# MAGIC

+# MAGIC

+

+# COMMAND ----------

+

+# MAGIC %pip install --quiet shap==0.46.0

+# MAGIC dbutils.library.restartPython()

+

+# COMMAND ----------

+

+# MAGIC %run ../_resources/00-setup $reset_all_data=false

+

+# COMMAND ----------

+

+# MAGIC %md

+# MAGIC

+# MAGIC ## Load Data

+# MAGIC

+# MAGIC To validate our model, we first load the necessary data from `credit_decisioning_features` and `credit_bureau_gold` tables. These datasets provide customer financial and credit bureau insights necessary for validation.

+

+# COMMAND ----------

+

+feature_df = spark.table("credit_decisioning_features")

+credit_bureau_label = spark.table("credit_bureau_gold")

+

+df = (feature_df.join(credit_bureau_label, "cust_id", how="left")

+ .withColumn("defaulted", F.when(col("CREDIT_DAY_OVERDUE").isNull(), 2)

+ .when(col("CREDIT_DAY_OVERDUE") > 60, 1)

+ .otherwise(0))

+ .drop('CREDIT_DAY_OVERDUE')

+ .fillna(0))

+display(df)

+

+# COMMAND ----------

+

+# MAGIC %md

+# MAGIC ## Load model

+# MAGIC

+# MAGIC We retrieve our trained model from the Unity Catalog model registry

+

+# COMMAND ----------

+

+import mlflow

+

+mlflow.set_registry_uri('databricks-uc')

+

+model = mlflow.pyfunc.load_model(model_uri=f"models:/{catalog}.{db}.{model_name}@none")

+features = model.metadata.get_input_schema().input_names()

+

+# COMMAND ----------

+

+# MAGIC %md

+# MAGIC

+# MAGIC ## Ensuring model fairness for existing credit customers

+# MAGIC

+# MAGIC In this example, we'll make sure that our model behaves as expected and is fair for our existing customers.

+# MAGIC

+# MAGIC We'll select our existing customers not having credit and make sure that our model is fair and behave the same among different group of the population.

+

+# COMMAND ----------

+

+underbanked_df = df[df.defaulted==2].toPandas() # Features for underbanked customers

+banked_df = df[df.defaulted!=2].toPandas() # Features for our existing credit customers

+

+# COMMAND ----------

+

+# MAGIC %md

+# MAGIC ## Feature importance using Shapley values

+# MAGIC

+# MAGIC SHAP is a game-theoretic approach to explain machine learning models, providing a summary plot

+# MAGIC of the relationship between features and model output. Features are ranked in descending order of

+# MAGIC importance, and impact/color describe the correlation between the feature and the target variable.

+# MAGIC - Generating SHAP feature importance is a very memory intensive operation.

+# MAGIC - To reduce the computational overhead of each trial, a single example is sampled from the underbanked set to explain.

+# MAGIC For more thorough results, increase the sample size of explanations, or provide your own examples to explain.

+# MAGIC - SHAP cannot explain models using data with nulls; if your dataset has any, both the background data and

+# MAGIC examples to explain will be imputed using the mode (most frequent values). This affects the computed

+# MAGIC SHAP values, as the imputed samples may not match the actual data distribution.

+# MAGIC

+# MAGIC For more information on how to read Shapley values, see the [SHAP documentation](https://shap.readthedocs.io/en/latest/example_notebooks/overviews/An%20introduction%20to%20explainable%20AI%20with%20Shapley%20values.html).

+

+# COMMAND ----------

+

+import shap

+

+mlflow.autolog(disable=True)

+mlflow.sklearn.autolog(disable=True)

+

+train_sample = banked_df[features].sample(n=np.minimum(100, banked_df.shape[0]), random_state=42)

+underbanked_sample = underbanked_df.sample(n=np.minimum(100, underbanked_df.shape[0]), random_state=42)

+

+# Use Kernel SHAP to explain feature importance on the sampled rows from the validation set.

+predict = lambda x: model.predict(pd.DataFrame(x, columns=features).astype(train_sample.dtypes.to_dict()))

+

+explainer = shap.KernelExplainer(predict, train_sample, link="identity")

+shap_values = explainer.shap_values(underbanked_sample[features], l1_reg=False, nsamples=100)

+

+# COMMAND ----------

+

+# DBTITLE 1,Save feature importance

+import matplotlib.pyplot as plt

+import os

+

+shap.summary_plot(shap_values, underbanked_sample[features], show=False)

+plt.savefig(f"{os.getcwd()}/images/shap_feature_importance.png")

+

+# COMMAND ----------

+

+# MAGIC %md

+# MAGIC Shapley values can also help for the analysis of local, instance-wise effects.

+# MAGIC

+# MAGIC We can also easily explain which feature impacted the decision for a given user. This can helps agent to understand the model an apply additional checks or control if required.

+

+# COMMAND ----------

+

+# DBTITLE 1,Explain feature importance for a single customer

+#shap.initjs()

+#We'll need to add shap bundle js to display nice graph

+with open(shap.__file__[:shap.__file__.rfind('/')]+"/plots/resources/bundle.js", 'r') as file:

+ shap_bundle_js = ''

+

+html = shap.force_plot(explainer.expected_value, shap_values[0,:], banked_df[features].iloc[0,:])

+displayHTML(shap_bundle_js + html.html())

+

+# COMMAND ----------

+

+# MAGIC %md

+# MAGIC ## Model fairness using Shapley values

+# MAGIC

+# MAGIC In order to detect discriminatory outcomes in Machine Learning predictions, it is important to evaluate how the model treats various customer groups. This can be achieved by devising a metric, such as such as demographic parity, equal opportunity or equal odds, that defines fairness within the model. For example, when considering credit decisioning, we can compare the credit approval rates of male and female customers. In the notebook, we utilize Demographic Parity as a statistical measure of fairness, which asserts that there should be no difference between groups obtaining positive outcomes (e.g., credit approvals) in an ideal scenario. However, such perfect equality is rare, underscoring the need to monitor and address any gaps or discrepancies.

+

+# COMMAND ----------

+

+gender_array = banked_df['gender'].replace({'Female':0, 'Male':1}).to_numpy()[:100]

+shap.group_difference_plot(shap_values.sum(1), \

+ gender_array, \

+ xmin=-1.0, xmax=1.0, \

+ xlabel="Demographic parity difference\nof model output for women vs. men")

+

+# COMMAND ----------

+

+

+shap_df = pd.DataFrame(shap_values, columns=features).add_suffix('_shap')

+shap.group_difference_plot(shap_df[['age_shap', 'tenure_months_shap']].to_numpy(), \

+ gender_array, \

+ feature_names=['age', 'tenure_months'],

+ xmin=-0.5, xmax=0.5, \

+ xlabel="Demographic parity difference\nof SHAP values for women vs. men")

+

+# COMMAND ----------

+

+# MAGIC %md

+# MAGIC ## Logging custom metrics/artifacts with **MLflow**

+

+# COMMAND ----------

+

+# Retrieve model version by alias

+client = mlflow.tracking.MlflowClient()

+model_version_info = client.get_model_version_by_alias(name=f"{catalog}.{db}.{model_name}", alias="none")

+

+# Log new artifacts in the same experiment

+with mlflow.start_run(run_id=model_version_info.run_id):

+ # Log SHAP feature importance

+ mlflow.log_artifact(f"{os.getcwd()}/images/shap_feature_importance.png")

+

+ #Log Demographic parity difference\nof model output for women vs. men

+ mean_shap_male = np.mean(shap_values[gender_array == 1])

+ mean_shap_female = np.mean(shap_values[gender_array == 0])

+ mean_difference = mean_shap_male - mean_shap_female

+ mlflow.log_metric("shap_demo_parity_diff_wm", mean_shap_male - mean_shap_female)

+

+# COMMAND ----------

+

+# MAGIC %md

+# MAGIC ## Compliance checks

+# MAGIC

+# MAGIC Our model is demographic parity difference metric is logged with the model. The model is registered in Unity Catalog with the 'None' alias.

+# MAGIC

+# MAGIC Let's assume that the absolute demographic parity difference of model output for women vs. men should be less than 0.1 to model to pass the compliance checks.

+# MAGIC

+

+# COMMAND ----------

+

+import mlflow

+

+# Retrieve experiment run by alias

+client = mlflow.tracking.MlflowClient()

+model_info = client.get_model_version_by_alias(name=f"{catalog}.{db}.{model_name}", alias="none")

+run = client.get_run(model_info.run_id)

+

+# Retrieve a specific metric, such as 'shap_demo_parity_diff_wm'

+shap_demo_parity_diff_wm = run.data.metrics.get("shap_demo_parity_diff_wm")

+

+# COMMAND ----------

+

+# Check whether the metric passes the requirements

+

+compliance_checks_passed = False

+

+if abs(shap_demo_parity_diff_wm) < 0.1:

+ compliance_checks_passed = True

+ print("compliance checks passed")

+else:

+ print("compliance checks failed")

+

+# COMMAND ----------

+

+# MAGIC %md

+# MAGIC ## Champion-Challenger testing

+# MAGIC

+# MAGIC ### Identify the current champion and challenger models

+# MAGIC

+# MAGIC If there is a model already in production, we define it as the current `champion model`. The model with the 'None' alias is defined as the `challenger model`.

+

+# COMMAND ----------

+

+# Set the Challenger model to the model with the None alias

+challenger_model_info = model_info

+challenger_run = run

+

+# Set the Champion model to the model with the Production alias

+try:

+ champion_model_info = client.get_model_version_by_alias(name=f"{catalog}.{db}.{model_name}", alias="production")

+except Exception as e:

+ print(e)

+ champion_model_info = None

+if champion_model_info is not None:

+ champion_run = client.get_run(champion_model_info.run_id)

+

+# COMMAND ----------

+

+# MAGIC %md

+# MAGIC Next, we compare the perfomance of the two models. In this case, we use the `val_f1_score` metric. The model with the highest `val_f1_score` is the new candidate for the `champion model`.

+

+# COMMAND ----------

+

+champion_challenger_test_passed = False

+

+if champion_model_info is None:

+ # No champion model. Challenger model becomes the champion. Mark test as passed.

+ champion_challenger_test_passed = True

+ print("No champion model. Challenger model becomes the champion.")

+elif challenger_run.data.metrics['val_f1_score'] > champion_run.data.metrics['val_f1_score']:

+ # Challenger model is better than champion model. Mark test as passed.

+ champion_challenger_test_passed = True

+ print("Challenger model performs better than champion.")

+else:

+ print("Challenger model does not perform better than champion.")

+

+# COMMAND ----------

+

+# MAGIC %md

+# MAGIC ## Update validation status

+# MAGIC

+# MAGIC Having done both compliance check and champion-challenger testing, we will now update the model's validation status. Only models that have passed both checks are approved to progress further into higher environments.

+# MAGIC

+# MAGIC For auditability, we also apply tags on the version of the model in Unity Catalog that we are now reviewing to record the status of the tests and validation check.

+

+# COMMAND ----------

+

+# Indicate if compliance checks has passed

+pass_fail = "failed"

+if compliance_checks_passed:

+ pass_fail = "passed"

+client.set_model_version_tag(f"{catalog}.{db}.{model_name}", model_info.version, "compliance_checks", pass_fail)

+

+# Indicate if champion-challenger test has passed

+pass_fail = "failed"

+if champion_challenger_test_passed:

+ pass_fail = "passed"

+client.set_model_version_tag(f"{catalog}.{db}.{model_name}", model_info.version, "champion_challenger_test", pass_fail)

+

+# Model Validation Status is 'approved' only if both compliance checks and champion-challenger test have passed

+# Otherwise Model Validation Status is 'rejected'

+validation_status = "Not validated"

+if compliance_checks_passed & champion_challenger_test_passed:

+ validation_status = "approved"

+else:

+ validation_status = "rejected"

+client.set_model_version_tag(f"{catalog}.{db}.{model_name}", model_info.version, "validation_status", validation_status)

+

+# COMMAND ----------

+

+# MAGIC %md

+# MAGIC ## Promote model to Staging

+# MAGIC

+# MAGIC Our model is now ready to be moved to the next stage. For this demo, we'll consider that our model is approved after going through the validation checks. It's now ready to be promoted to `Staging`. In `Staging`, the model will go through integration testing, before being deployed to `Prodution`.

+# MAGIC

+# MAGIC Otheriwse, if the model is rejected after going through the validation checks, we archive the model by setting its alias to `Archived`.

+# MAGIC

+# MAGIC Before promoting the model into `Staging`, there can be a human validation of the model involved.

+

+# COMMAND ----------

+

+# The production model is the champion model used in champion-challenger testing above

+# We will use the prod_model_info variable here for the code to be easier to understand

+prod_model_info = champion_model_info

+

+if prod_model_info is None:

+ # No model in production. Set this model as the candidate production model by promoting it to Staging

+ client.delete_registered_model_alias(name=f"{catalog}.{db}.{model_name}", alias="none")

+ client.set_registered_model_alias(name=f"{catalog}.{db}.{model_name}", alias="staging", version=model_info.version)

+ print(f'{model_info.version} of {catalog}.{db}.{model_name} is now promoted to Staging.')

+elif validation_status == "approved":

+ # This model has passed validation checks. Promote it to Staging.

+ client.delete_registered_model_alias(name=f"{catalog}.{db}.{model_name}", alias="none")

+ client.set_registered_model_alias(name=f"{catalog}.{db}.{model_name}", alias="staging", version=model_info.version)

+ print(f'{model_info.version} of {catalog}.{db}.{model_name} is now promoted to Staging.')

+else:

+ # This model did not pass validation checks. Set it to Archived.

+ client.delete_registered_model_alias(name=f"{catalog}.{db}.{model_name}", alias="none")

+ client.set_registered_model_alias(name=f"{catalog}.{db}.{model_name}", alias="archived", version=model_info.version)

+ client.set_model_version_tag(f"{catalog}.{db}.{model_name}", model_info.version, f"archived", "true")

+ print(f'{model_info.version} of {catalog}.{db}.{model_name} is transitioned to Archived. No model promoted to Staging.')

+

+# COMMAND ----------

+

+# MAGIC %md

+# MAGIC

+# MAGIC ## Store Data (into Delta format) for Downstream Usage

+# MAGIC

+# MAGIC Finally, we store the validated dataset in Delta format for auditing and future reference

+

+# COMMAND ----------

+

+#Let's load the underlying model to get the proba

+try:

+ skmodel = mlflow.sklearn.load_model(model_uri=f"models:/{catalog}.{db}.{model_name}@Staging")

+ underbanked_sample['default_prob'] = skmodel.predict_proba(underbanked_sample[features])[:,1]

+ underbanked_sample['prediction'] = skmodel.predict(underbanked_sample[features])

+ final_df = pd.concat([underbanked_sample.reset_index(), shap_df], axis=1)

+

+ final_df = spark.createDataFrame(final_df).withColumn("default_prob", col("default_prob").cast('double'))

+ display(final_df)

+ final_df.drop('CREDIT_CURRENCY', '_rescued_data', 'index') \

+ .write.mode("overwrite").option('OverwriteSchema', True).saveAsTable(f"shap_explanation")

+except:

+ print("No model in staging.")

+

+# COMMAND ----------

+

+# MAGIC %md

+# MAGIC ## Next Steps

+# MAGIC

+# MAGIC In the next step [06.5-Model-Integration]($./06-Responsible-AI/06.5-Model-Integration), we will conduct integration testing on the model with other components that use it. An example of that is a batch inference pipeline. This is how the model is deployed responsibly, ensuring traceability and accountability at each decision point, while ensuring the integrity of systems and application where the model is used.

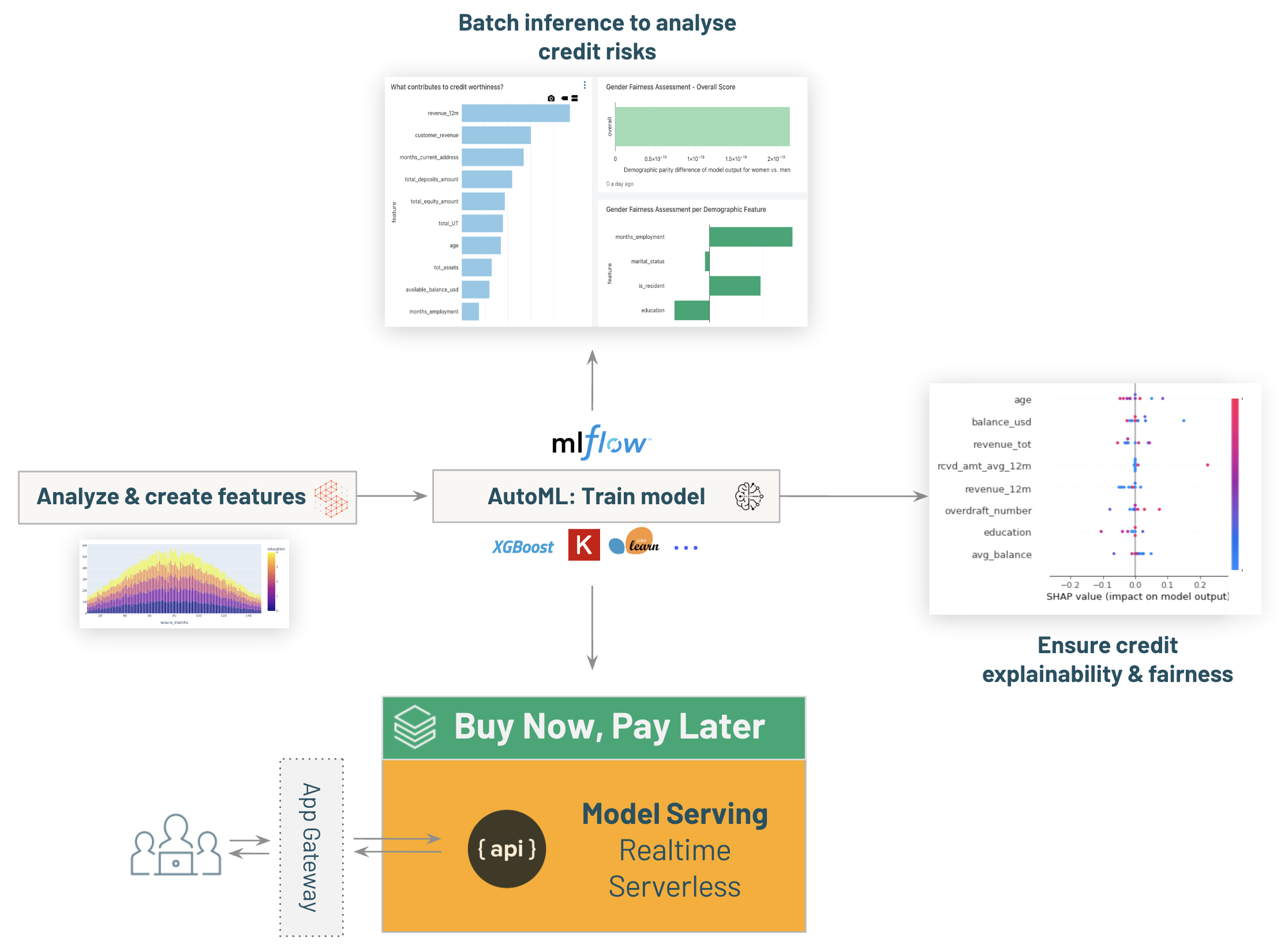

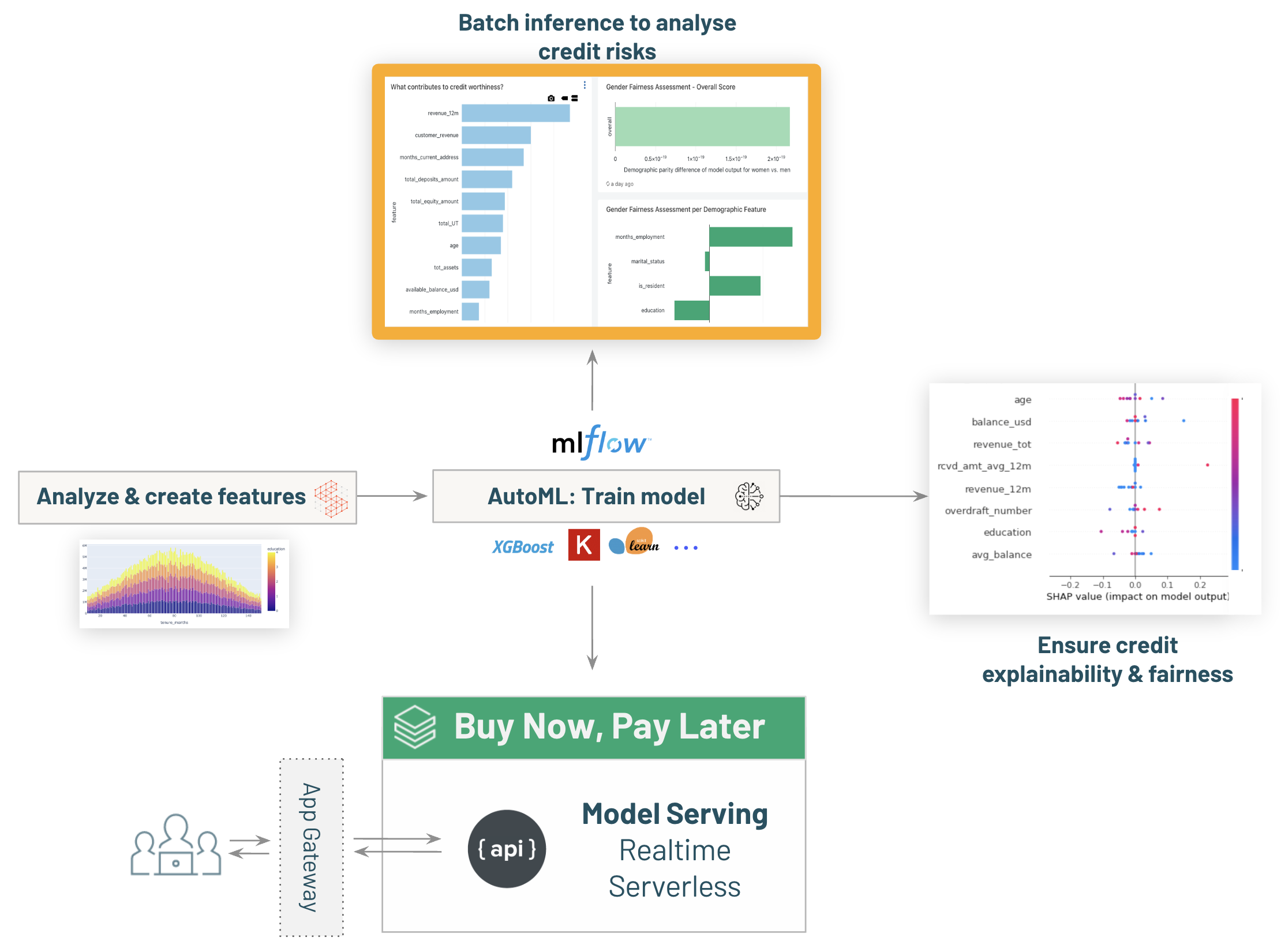

diff --git a/demo-FSI/lakehouse-fsi-credit-decisioning/03-Data-Science-ML/03.4-model-serving-BNPL-credit-decisioning.py b/demo-FSI/lakehouse-fsi-credit-decisioning/03-Data-Science-ML/03.4-model-serving-BNPL-credit-decisioning.py

deleted file mode 100644

index 61541b9f..00000000

--- a/demo-FSI/lakehouse-fsi-credit-decisioning/03-Data-Science-ML/03.4-model-serving-BNPL-credit-decisioning.py

+++ /dev/null

@@ -1,193 +0,0 @@

-# Databricks notebook source

-# MAGIC %md-sandbox

-# MAGIC

-# MAGIC # Buy Now, Pay Later (BNPL)

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC

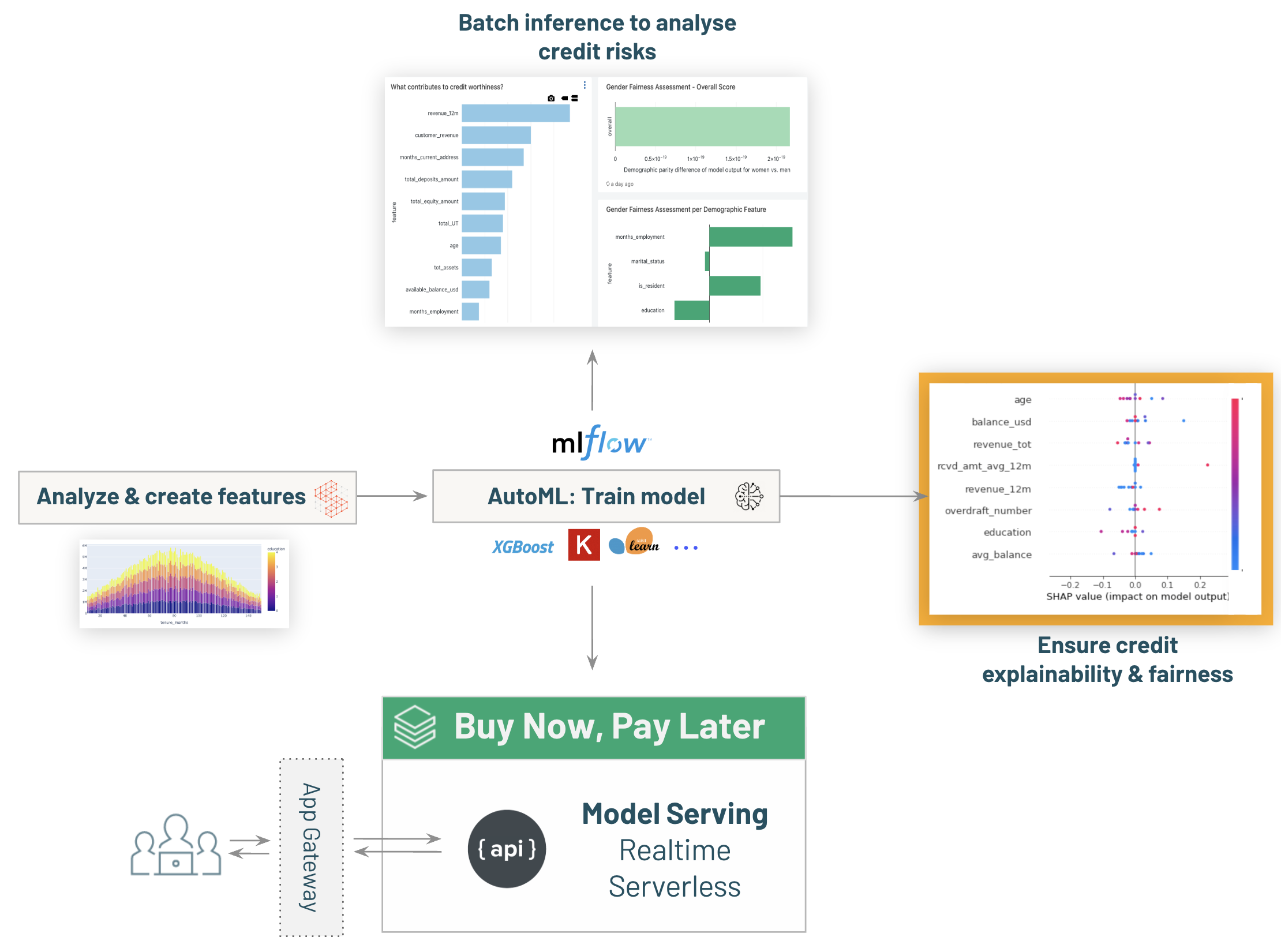

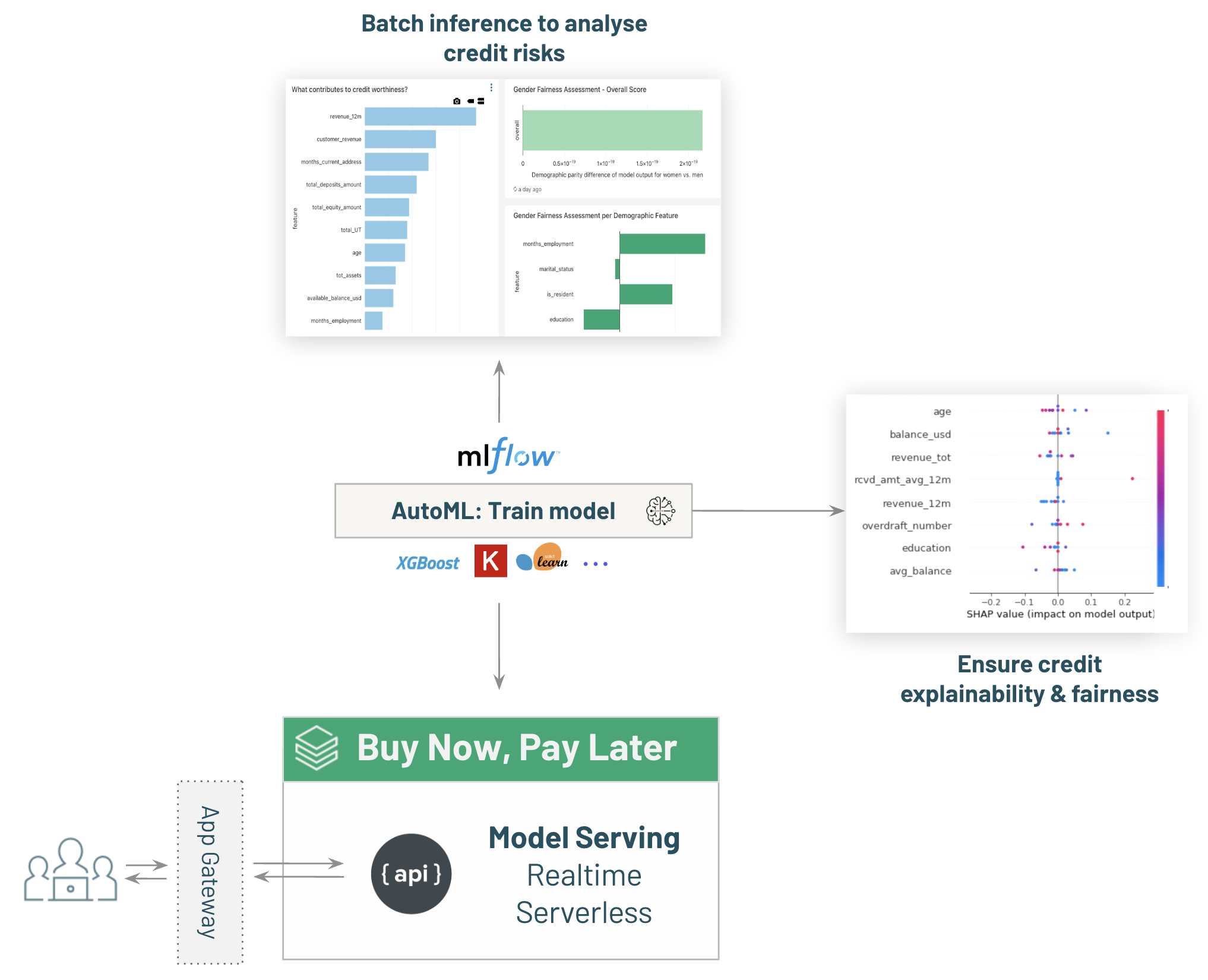

-# MAGIC ### *"Can we allow a user without sufficient balance in their account to complete the current (debit or credit) transaction?"*

-# MAGIC

-# MAGIC

-# MAGIC We will utilize our credit risk model (built in the previous steps) in real-time to answer this question.

-# MAGIC

-# MAGIC The payment system will be able to call our API in realtime and get a score within a few ms.

-# MAGIC

-# MAGIC With this information, we'll be able to offer our customer the choice to pay with a credit automatically, or refuse if the model believes the risk is too high and will likely result in a payment default.

-# MAGIC

-# MAGIC

-# MAGIC These types of decisions are typically embedded in live Point Of Sales (stores, online shop). That is why we need real-time serving capabilities.

-# MAGIC

-# MAGIC

-# MAGIC

-# MAGIC

-

-# COMMAND ----------

-

-# MAGIC %md

-# MAGIC # Deploying the Credit Scoring model for real-time serving

-# MAGIC

-# MAGIC

-# MAGIC Let's deploy our model behind a scalable API to evaluate credit-worthiness in real-time.

-# MAGIC

-# MAGIC ## Databricks Model Serving

-# MAGIC

-# MAGIC Now that our model has been created with Databricks AutoML, we can easily flag it as Production Ready and turn on Databricks Model Serving.

-# MAGIC

-# MAGIC We'll be able to send HTTP Requests and get inference in real-time.

-# MAGIC

-# MAGIC Databricks Model Serving is fully serverless:

-# MAGIC

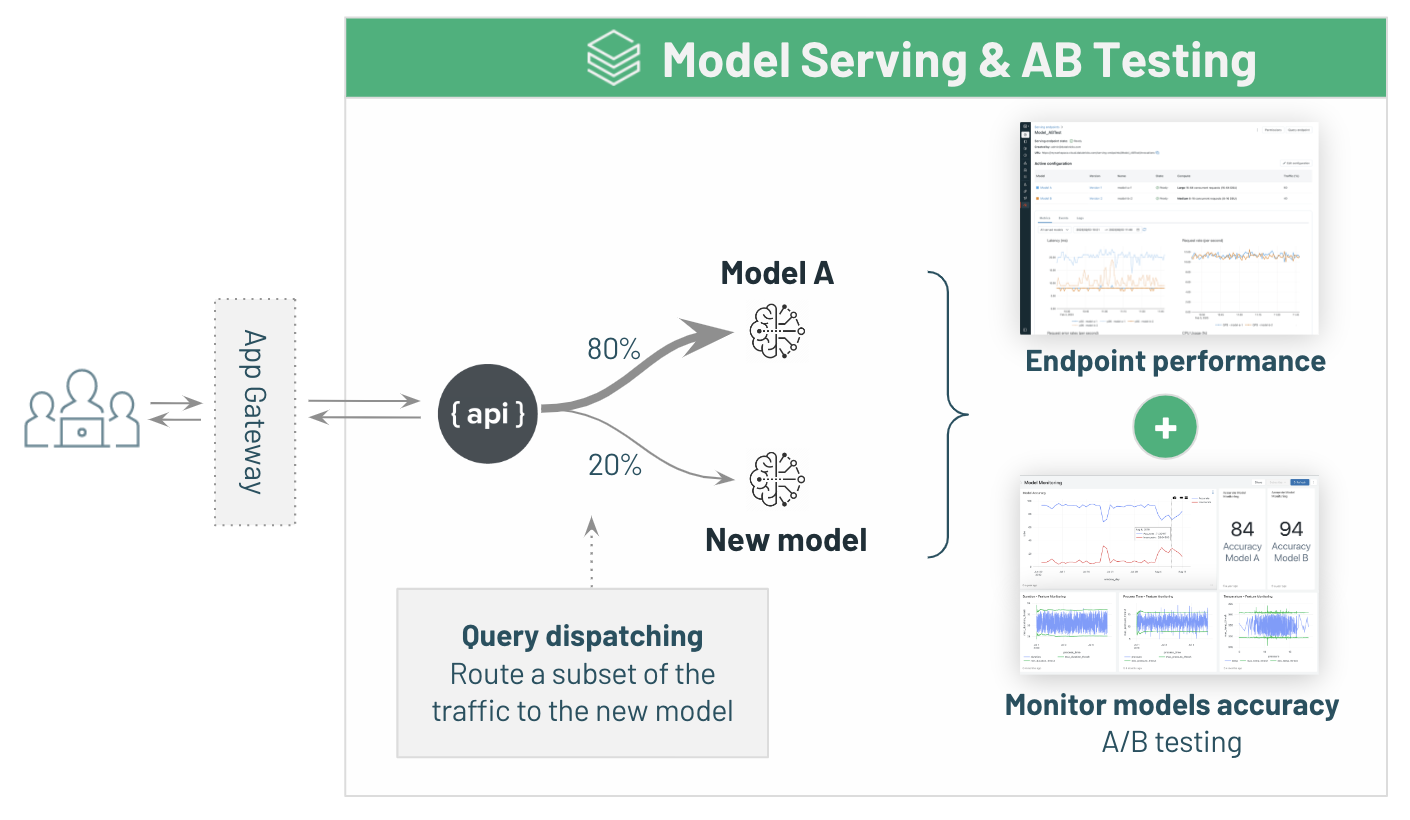

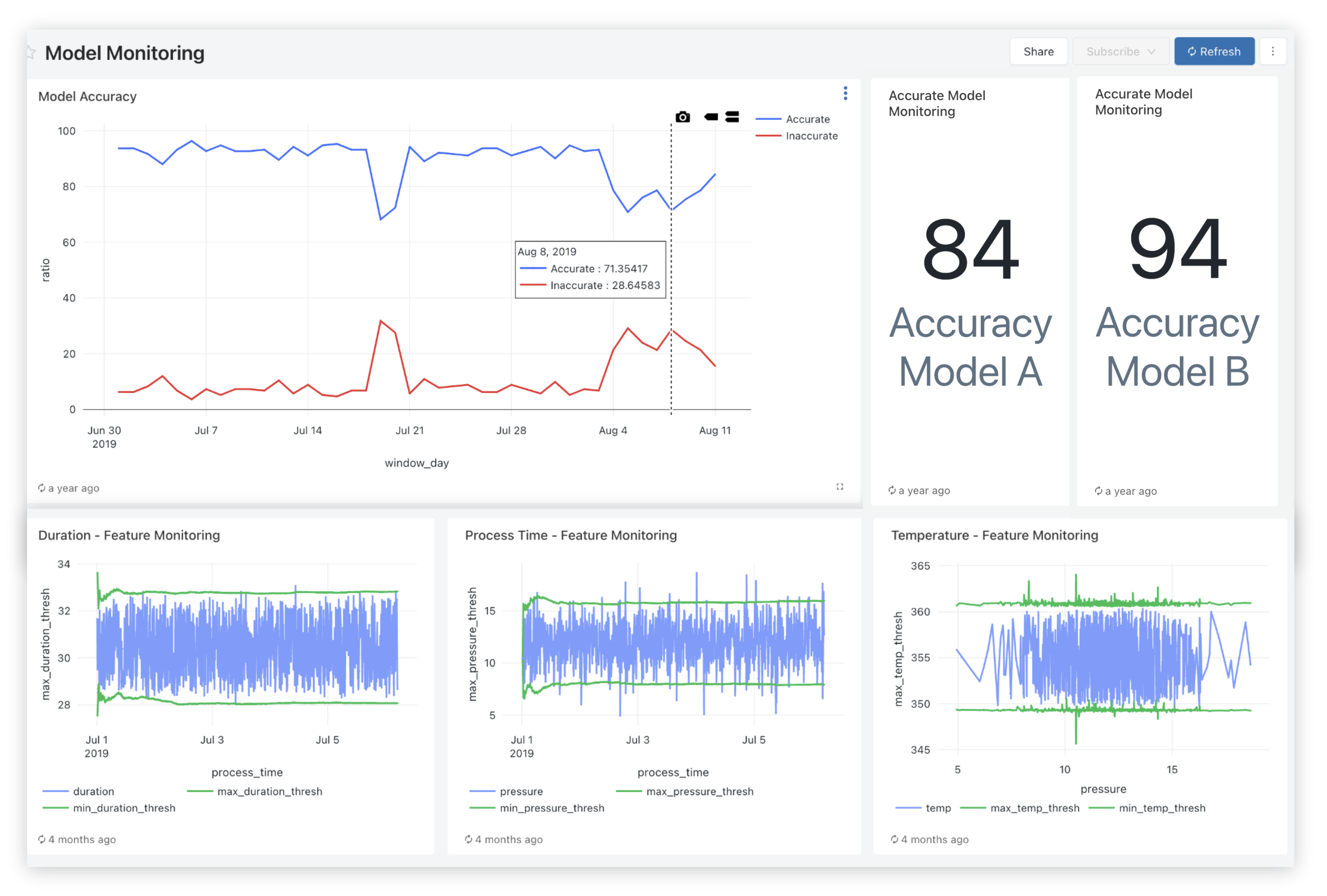

-# MAGIC * One-click deployment. Databricks will handle scalability, providing blazing fast inferences and startup time.

-# MAGIC * Scale down to zero as an option for best TCO (will shut down if the endpoint isn't used).

-# MAGIC * Built-in support for multiple models & version deployed.

-# MAGIC * A/B Testing and easy upgrade, routing traffic between each versions while measuring impact.

-# MAGIC * Built-in metrics & monitoring.

-

-# COMMAND ----------

-

-# MAGIC %pip install mlflow==2.19.0

-# MAGIC dbutils.library.restartPython()

-

-# COMMAND ----------

-

-# MAGIC %run ../_resources/00-setup $reset_all_data=false

-

-# COMMAND ----------

-

-# DBTITLE 1,Make sure our last model version is deployed in production in our registry

-import mlflow

-model_name = "dbdemos_fsi_credit_decisioning"

-mlflow.set_registry_uri('databricks-uc')

-

-# COMMAND ----------

-

-

-from databricks.sdk import WorkspaceClient

-from databricks.sdk.service.serving import ServedEntityInput, EndpointCoreConfigInput, AutoCaptureConfigInput

-

-model_name = f"{catalog}.{db}.dbdemos_fsi_credit_decisioning"

-serving_endpoint_name = "dbdemos_fsi_credit_decisioning_endpoint"

-w = WorkspaceClient()