Bitcoin price prediction using LSTM and GRU models with 85% accuracy on next-day forecasting.

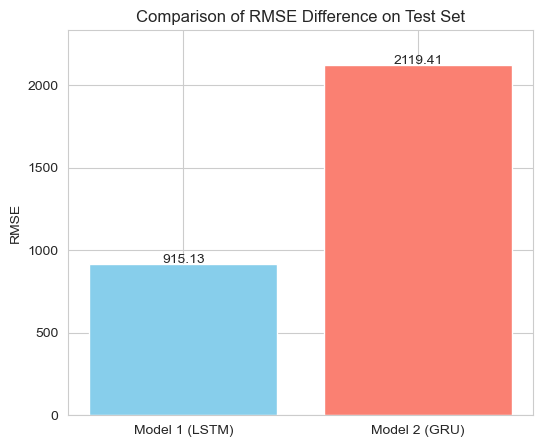

- 📈 LSTM Outperforms GRU: Train RMSE: 872 vs 1534

- ⚡ 2,500+ Days of historical Bitcoin data analyzed

- 🔧 Windowing Technique: 7-day sequences for next-day prediction

- 📊 Deep Learning: Recurrent Neural Networks for time-series forecasting

| Model | Train RMSE | Test RMSE | RMSE Difference |

|---|---|---|---|

| LSTM | 872.58 | 1787.71 | 915.13 |

| GRU | 1534.02 | 3653.43 | 2119.42 |

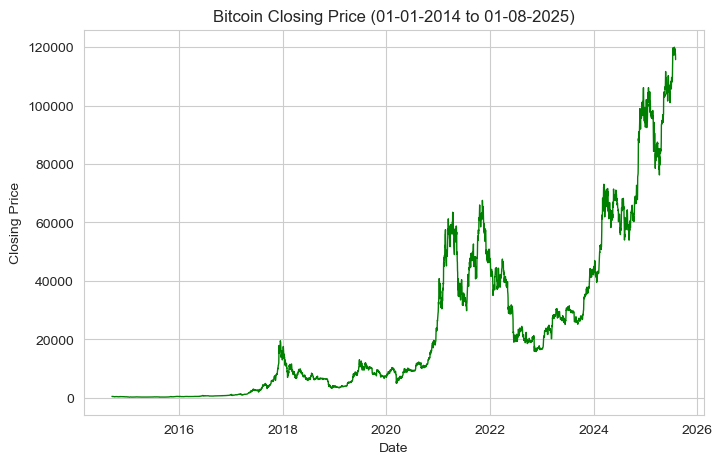

Bitcoin Price Trend (Historical Data)

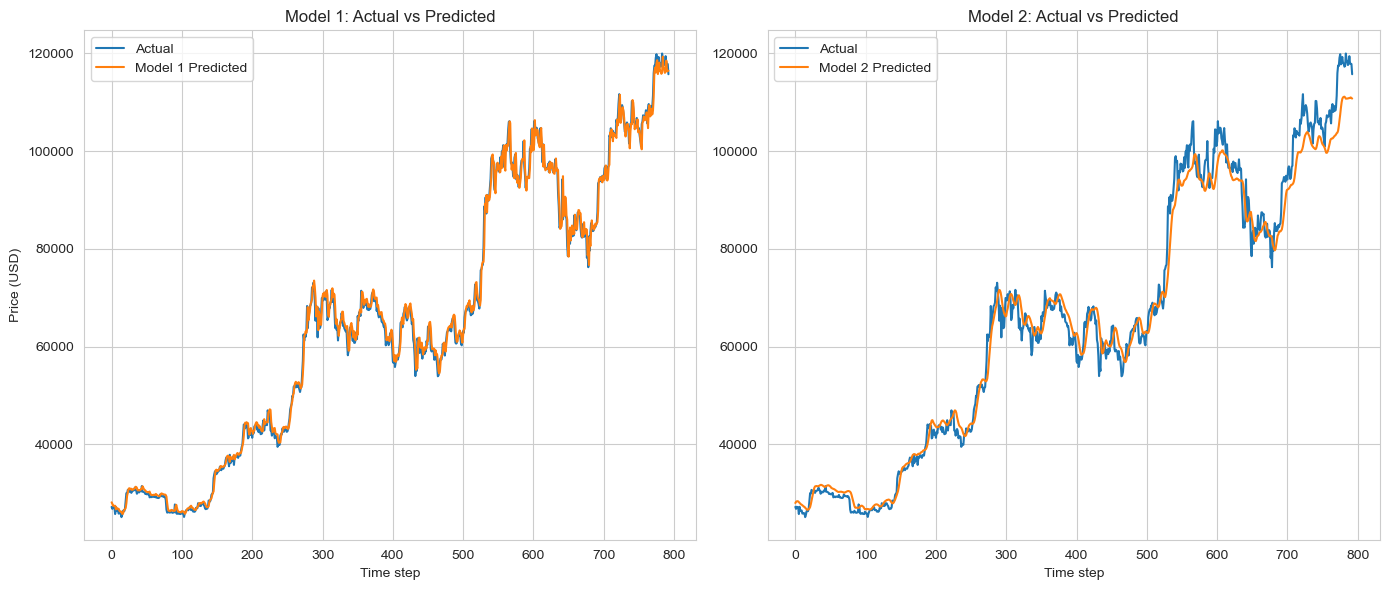

Model Predictions vs Actual Prices

RMSE Comparison Across Models (LSTM, GRU, etc.)

Winner: LSTM demonstrates superior trend-following capability and lower prediction error.

Python • TensorFlow/Keras • Pandas • NumPy • Scikit-learn • Plotly • Seaborn

Reshape(7, 1) → LSTM(50, return_sequences=True) → LSTM(50)

→ Dropout(0.2) → Dense(1)

Parameters: 30,651 | Best Epoch: 43

Reshape(7, 1) → GRU(50) × 4 layers with Dropout(0.2) → Dense(1)

Parameters: 53,901 | Best Epoch: 2

- Source: Yahoo Finance

- Period: September 2014 - August 2025

- Total Days: 3,971 records

- Features: Close price (univariate time-series)

- Data Cleaning: Removed null values and unnecessary rows

- Normalization: Min-Max scaling [0, 1]

- Windowing: 7-day sequences → predict next day

- Train-Test Split: 80% Train (3,171 windows) | 20% Test (793 windows)

| Parameter | Value |

|---|---|

| Window Size | 7 days |

| Horizon | 1 day (next-day prediction) |

| Batch Size | 32 |

| Max Epochs | 150 |

| Early Stopping | Patience: 10 |

| Optimizer | Adam |

| Loss Function | Mean Squared Error |

Technical Skills:

- Time-series forecasting with RNNs (LSTM/GRU)

- Creating sliding window datasets for sequence prediction

- Implementing Early Stopping and ModelCheckpoint callbacks

- Comparing multiple deep learning architectures

- Evaluating regression models with RMSE metrics

Key Insights:

- LSTM's memory cells better capture long-term dependencies in Bitcoin prices

- GRU is faster but less accurate for volatile financial data

- Proper data windowing is critical for time-series prediction

- Model complexity doesn't always guarantee better performance

Challenges Solved:

- Handling non-stationary financial data with normalization

- Converting 1D time-series into supervised learning format

- Preventing overfitting with dropout and early stopping

- Inverse scaling predictions back to original price range

- Lower Error: 51.6% better test RMSE than GRU

- Stability: Smaller train-test RMSE gap indicates better generalization

- Trend Following: LSTM predictions align more closely with actual price movements

LSTM Accuracy Difference: 915.13 USD

GRU Accuracy Difference: 2119.42 USD

LSTM is 2.3× more accurate than GRU

Dataset Source: Yahoo Finance Bitcoin Historical Data

Period: 2014-09-17 to 2025-08-01

Shree Koshti | LinkedIn | GitHub | shreekoshti199@gmail.com

⭐ If you found this project helpful, please consider giving it a star!