Interactive Modern Portfolio Theory optimizer with real-time data

|

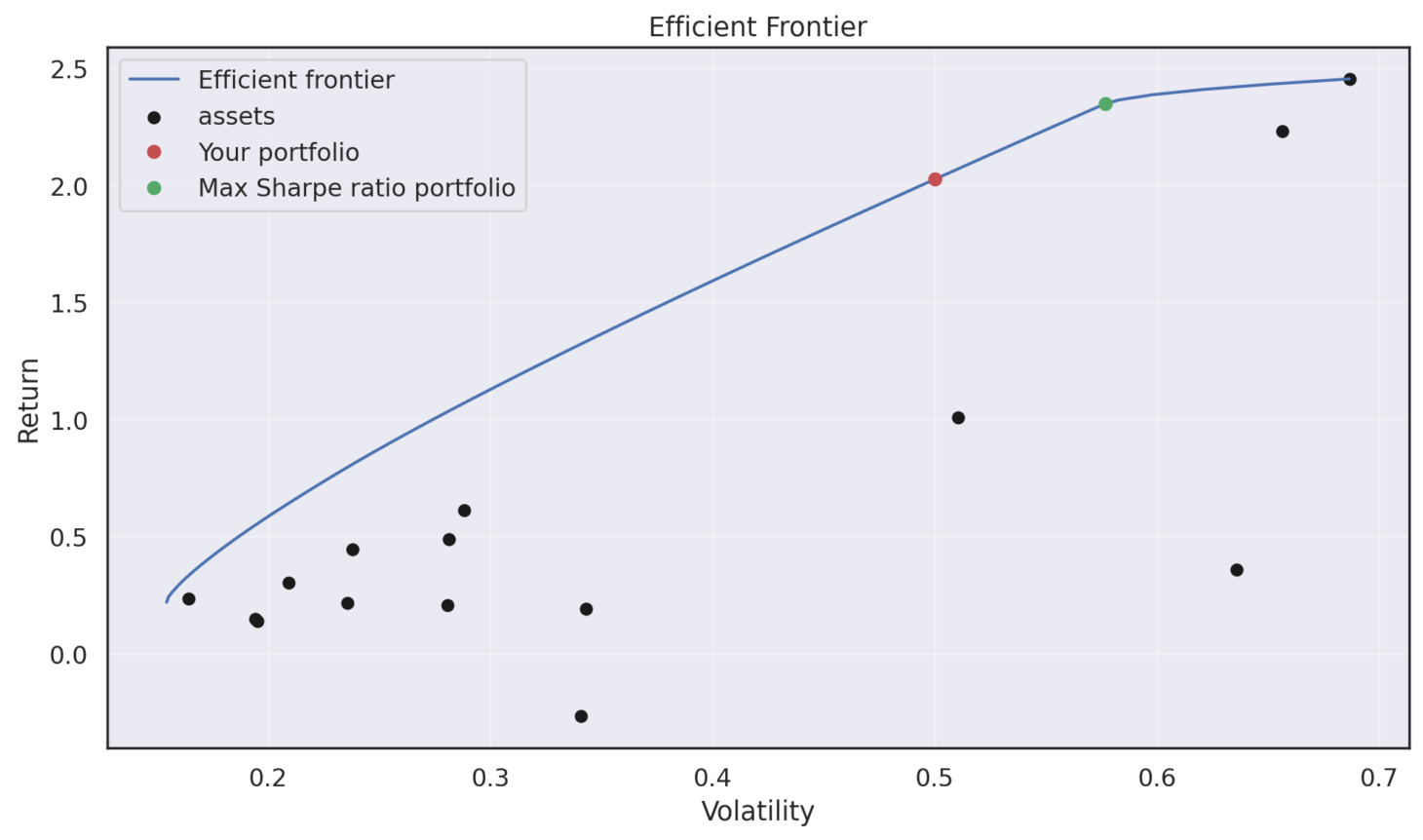

Efficient Frontier All possible portfolios from your tickers |

Max Sharpe Ratio Portfolio Optimal risk-adjusted allocation (green dot) |

- Real-time price & return data via yfinance

- Interactive Efficient Frontier with thousands of simulated portfolios

- Find Maximum Sharpe Ratio portfolio automatically

- Set your own risk tolerance (target volatility)

- See exact weights for each ticker in the optimal portfolio

- Works with any NASDAQ/NYSE tickers

- Lets you set your own acceptable risk level and shows the optimal allocation for it

- Displays exact weights for each stock, expected return, volatility, and Sharpe ratio

- Calculates optimal portfolio w/performance

Python • Streamlit • Plotly • Pandas • NumPy • SciPy

Live Demo (wakes in 30–60 sec)

https://markowitz-portfolio-optimization-model.streamlit.app